There comes a time when it’s too late to tell people how you feel.

There will come a day when the person you mean to talk to won’t be there. Don’t wait for that day.

“There’s always tomorrow” isn’t always true.

The no-pants guide to spending, saving, and thriving in the real world.

There comes a time when it’s too late to tell people how you feel.

There will come a day when the person you mean to talk to won’t be there. Don’t wait for that day.

“There’s always tomorrow” isn’t always true.

Last weekend, we held a garage sale at my mother-in-law’s house. It was technically an estate sale, but we treated it exactly as a garage sale.

A week before we started, a friend’s mother came to buy all of the blankets and most of the dishes, pots, and non-sharp utensils so she could donate them all to a shelter she works with. She took at least 3 dozen comforters and blankets away.

Even after that truckload, we started with two double rows of tables through the living room and dining room. The tops of the tables were as absolutely full as we could get them, and the floor under the tables was also used for displaying merchandise.

Have you ever had to display 75 brand-new pairs of shoes in a minimal about of space? They claimed about 16 feet of under-table space all by themselves. Thankfully, the blankets weren’t there anymore.

We also had half of the driveway full of furniture, toys, and tools.

We had a lot of stuff.

Now, most people hold a sale to make some money. Not us. We held a sale to let other people pay us for the privilege of hauling away our crap. As such, it was all priced to move. The most expensive thing we sold was about $20, but I can’t remember what that was. Most things went for somewhere between 25 cents and $1.

At those prices, we sold at least 2000 items. That isn’t a typo. We ended the day with $1325. After taking out the initial seed cash, lunches we bought for the people helping us, and dinner we bought one night, we had a profit of $975.

At 25 cents per item.

We optimized to sell instead of optimizing for profit. At the end of a long summer of cleaning out a hoarding house, it all needed to go.

In the next part, I’ll explain exactly how we made it work.

When my mother-in-law died, we went through all of her accounts and paid off anything she owed.

The Discover card she’d carried since the 80s–a card that had my wife listed as an authorized user–had a balance of about $700. We paid that off with the money in her savings account. They cashed out the accumulated points as gift cards and closed the account.

A few months ago, we decided it was time to buy an SUV, to fit our family’s needs. We financed it, to give us a chance to take advantage of a killer deal while waiting for the state to process the title transfer on an inherited car we have since sold.

Getting good terms was never a worry. Both of us had scores bordering on 800. Since our plan was to pay off the entire loan within a few months, we asked for whatever term came with the lowest interest rate.

Then the credit department came back and said that my wife’s credit was poor. I chalked it up to a temporary blip caused by closing the oldest account on her credit report and financed without her. No big deal.

Since we decided to rent our my mother-in-law’s house, we’ve discussed picking up more rental properties. That’s a post for another time, but last week, we went to get pre-approved for a mortgage. During the process, the mortgage officer asked me if my wife had any outstanding debt that could be ignored if we financed without her.

Weird.

A few days ago, we got the credit check letter from the bank. Her credit score? 668.

What the heck?

I immediately pulled her free annual credit report from annualcreditreport.com, which is something I usually do 2-3 times per year, but had neglected for 2012.

There are currently two negatives on her report.

One is a 30 day late payment on a store card in 2007. That’s not a 120 point hit.

The other is an $8 charge-off to Discover. As an authorized user. On an account that was paid.

Crap.

We called Discover to get them to correct the reporting and got told they don’t have it listed as a charge-off. They did agree to send a letter to us saying that, but said they couldn’t fix anything with the credit bureaus.

Once we get that letter, it’s dispute time.

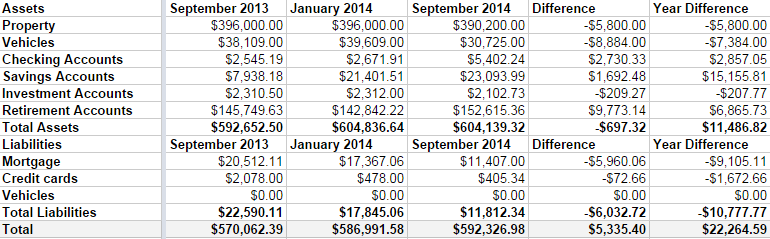

It’s time for my irregular-but-usually-quarterly net worth update. It’s boring, but I like to keep track of how we’re doing. Frankly, I was a bit worried when I started this because we’ve been overspending this summer and Linda was off work for the season.

But, all in all, we didn’t do too bad.

Some highlights:

I can’t say I’m upset with our progress. We’ve paid down $6000 in debt in 2014, including 3 months with 1 income. We aren’t maxing our retirement accounts, yet, but I’d like to be completely debt free before I do that. It’s bad math, but having all of my debt gone will give me such a warm fuzzy feeling, I can’t not do it.

My immediate goal is to hit a $600,000 net worth by my next update in January. I’m only about $7000 off.

Time to hit the casino. Err, I mean, time to up my 401k contribution from 5% to 7%.

Mariano Rivera is the most dominant closer in the history of baseball. His cut fastball, or cutter, is considered by many to be the best pitch in the history of the game. He is the all-time saves leader, and he has five World Series rings that he can wear. Of course, he has made millions of dollars over his professional career, which has brought him a long way from his humble roots as the son of a Panamanian fisherman.

Instead, Rivera and his friends would play games with tree branches for bats. They used milk cartons instead of gloves, and they taped together pieces of old fishing nets to use as balls. Rivera didn’t have his first real leather baseball glove until his dad bought him one at the age of 12.

Rivera liked baseball, but he never thought he would one day make a living at it. Instead, he dreamed of playing soccer professionally like most Latinos. However, he suffered a series of ankle injuries during high school that shattered this dream. He finished school at age 16 and began working on his father’s fishing boat. He had to abandon ship when the boat capsized, and that scared him away from fishing forever.

Soon after that, Rivera started playing on a local amateur baseball team, Panama Oeste. He was the team’s shortstop, and he only started pitching because the team’s normal pitcher was in a slump. His teammates were so impressed with his pitching skills that they convinced the Panama scout for the New York Yankees to give him a tryout. Rivera went to Panama City for a Yankees tryout camp, and the Yankees signed the man who would become one of the greatest players of all-time to a contract worth just $3,000.

When Rivera came to the United States, he did not speak English and was incredibly homesick. Puerto Caimito did not have telephone service at that time, which meant Rivera could only communicate to his family back home by writing long letters.

Rivera made steady progress through the minor leagues, but it was still five years before he was called up to the big leagues. His first few years in the major leagues, Rivera made the minimum salary of $750,000. This is a small figure by American standards, but it is more money than most people in Panama can dream of.

Rivera still goes back to Panama every year. He feels it is a home and that he is a part of it. His riches have never transformed him into a diva. He is one of the most down-to-earth and genuinely friendly players in the game.