Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

The no-pants guide to spending, saving, and thriving in the real world.

Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

The publicly documented downward spiral of Amanda Bynes may be reaching its breaking point. She has been on psychiatric lockdown for the past three days, and her parents are petitioning for conservatorship in California

on the grounds that they believe she is suffering from acute schizophrenia. They claim that the troubled starlet is unable to make safe decisions regarding her own well-being, not to mention the safety of others. The issue is complex, but the former childhood star has demonstrated that she meets the criteria to have external guardians instated to protect her from unpredictably irrational behaviors.

This was not the first criminal case against Bynes; she is also dealing with hit-and-run allegations in California. It was also not her last interaction with the police. Most recently, the actress doused an elderly woman’s driveway in gasoline and set it ablaze. She accidentally covered a puppy in the flammable liquid, so she ran down the block looking for something to save the animal from catching fire. After ransacking a convenience store, officers accosted her. The exchange resulted in the psychiatric hold that has been placed on Bynes.

Unfortunately, grounds for conservatorship can be exceedingly challenging to meet. Clear proof of mental illness needs to provided, and the standards are rigidly strict; however, if anyone has showcased the fanatical craziness that constitutes a lack of personal responsibility, it is Amanda Bynes.

Her schizophrenia is no longer dormant. The actress has become obsessed with plastic surgery, and she has deformed her face with cheek piercings. She uses online social networks to decry public figures for their ugliness. Victims of this attack include even Barack and Michelle Obama. Furthermore, she makes offensive sexual remarks towards rappers, and she wants to be a hip-hop artist herself. She has spent fortunes on a wig collection, and she employs a different style at every court appearance. The actress even used one as a disguise for an incognito trip to a trampoline emporium.

Anyone that has seen her Nickelodeon program would not be shocked to learn that she was schizophrenic. The role had her switching between dozens of identities for different skits, and she even played a character that was, in effect, obsessively stalking the star herself. “The Amanda Show” was neurotically fast-paced. Ultimately, the entire program can now be viewed as an eerie foreshadowing to the budding of a latent psychological disorder. If the legal standards of insanity are not met, then she will be free to wreak havoc on herself and others.

Would you be ready for the apocalypse? The Walking Dead asks that question every week. There is a great deal of human intrigue in the show, but the show is always asking you, the viewer, if you would be ready to deal with an apocalypse on that order. The idea goes much farther than dealing with zombies. Truly, zombies are the easy part of the apocalypse.

Lost People

We live in a world where we are very connected. You know people from all over the world, and it the entire world has been overrun by an apocalypse at once, all the people you are connected to around the world are effectively gone. There is no chance you will ever see them again. The people on the show deal with those ideas every day. There are so many people they miss that they never go to to say goodbye to.

Insecurity

The one thing that the apocalypse creates is insecurity. You will have no idea what is going to happen the next morning. You never know when someone in your crew is going to be bitten or killed. You have no idea when you will run into other humans you cannot trust. There is not a safe place on Earth. Even if you lock down a house, there is no way to know for sure that zombies would not get in.

Violence

The Walking Dead graphically depicts the violence that is necessary to kill zombies. You would have to “kill” thousands of people who have become zombies. You can see their wedding rings. You can see them in their uniforms, and you know that they used to be somebody. However, you have to end them in order to save yourself. Many of us believe we could do that, but we need to think twice before we assume we could be that violent.

Order

The lack of order in the world is the thing that would break most of us. We can reconcile loss, but that loss is hard to reconcile when there is no order in the world. There is not one authority on the planet that is still operating. How would you be able to resolve problems without such a structure?

On the show, all these problems are handled violently. Murdering violent people is all part of the job if you want to stay alive. It is one thing to kill a zombie that is no longer a person, but it is something else to kill a real person who is simply a thieving criminal.

You might think that you would do just fine when you are watching The Walking Dead, but you would not know unless it happened in real life. The zombie apocalypse is not all fun and games. At its heart is a tense human emotion called loss that we would all have to confront head on.

One of the best ways in the early years of your career to provide for your long term future is to have a 401K for your retirement where your employer will match your own contributions up to a certain figure. Your contribution is pre-tax incidentally. Albert Einstein once said that compound interest was the ‘eighth wonder of the world’ and it is compound interest that will help even small amounts to grow into a substantial figure on retirement if savings begin in your 20s.

It is worth illustrating this with real figures. A figure of $4,000 a year saved between the ages of 25 and 35 with no further contributions after that will produce a larger final figure at 65 than someone starting at 35 and contributing $4,000 per annum for 30 years. The latter has invested three times as much as well. The factors that decide this are time and compound interest. The whole total of former is working for him or her for 30 years. A fair amount of the second example is only ‘working’ positively for a limited time. Start early!

An Illustration

It is worth looking at examples to see what size of fund is realistic. 8% is not an unreasonable sum to put away on a salary of $40,000 a year, a salary that grows at 2% per annum for 20 years. If the employer pays 3% in addition and growth is a modest 7%, the fund at the end of 20 years would be around $210,000. If you can put 10% in instead, or if you extend the saving period to 30 years the fund rockets to over $500,000! It’s time and compound interest again because in the example over 20 years you will have only put in just under $80,000 yourself to have a fund two and a half times bigger.

A Couple of Observations

Can there be a bigger argument for saving from an early age than that? Surely not! The question is how to manage your money well enough so that you can start to save in the early years of your career. You may well have a student loan to begin to pay off. Probably two of the most important things to do with realisticloans.com, or not to do depending how you look at it are:

Expenditure

There is no doubt that you may well have monthly expenditure you did not face before, especially if you have relocated to start work. Such expenditure is unavoidable but you should spend some time on researching whether you are getting the best deals. That applies to a number of significant things such as utilities, insurance and telephone. There are comparison websites that do a good deal of research for you and at least will provide you with a short list to look at further.

The aim is to create a regular surplus that can be transferred out of your checking account when your monthly pay comes in to work positively for you and your future. You will need to apply self-discipline to your finances but you can see from the example of ‘time and compound interest’ what they benefits are for being in control. It really is not much to sacrifice.

There will be times in the years to come when you have big financial decisions to make. Real estate comes to mind immediately and a long term mortgage can reasonably be regarded as positive debt because it should produce good growth over the term you have committed yourself to. With real estate often comes marriage and a family; and all the expense that involves. Yet that responsibility is yet another reason to start young in saving for the future, and your possible dependents.

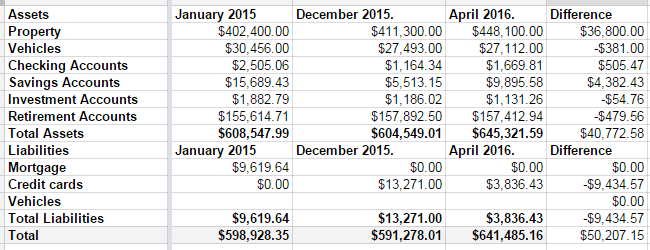

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.

I last did a net worth update in August. I don’t worry much about tracking my net worth, but I’d like to know where I sit at the beginning of the year. If I’m going to track it, I’m going to share it.

This is where I was sitting in August:

Overall: $239,317

Overall: $249,717 (+9400)

I had two goals in August: Get an IRA rolling and save an extra $2500.

The IRAs I have are just sitting. I haven’t done anything to boost them, in any way, so hurray for the free $1163!

My savings have only grown my $773, but the $1000 I put in the investment account 3 weeks ago came from my car fund, so it would have been a growth of $1773, which isn’t bad at all.

I would still like to kill that credit card debt by August, which I think is doable. My crazy goal is to get rid of it by the end of May.

On 4/15/2009, I had $90,395 in debt. Today, it’s $48,707, so I’ve paid down $41,688 in just under three years, for an average of $1263 per month. That average is down $92 over the last few months. I blame our insane Christmas.

Overall, we had a good year. Paying off my car loan while paying down $4800 in credit card debt feels good. Now, I need to make 2012 better.