- RT @ScottATaylor: Get a Daily Summary of Your Friends’ Twitter Activity [FREE INVITES] http://bit.ly/4v9o7b #

- Woo! Class is over and the girls are making me cookies. Life is good. #

- RT @susantiner: RT @LenPenzo Tip of the Day: Never, under any circumstances, take a sleeping pill and a laxative on the same night. #

- RT @ScottATaylor: Some of the United States’ most surprising statistics http://ff.im/-cPzMD #

- RT @glassyeyes: 39DollarGlasses extends/EXPANDS disc. to $20/pair for the REST OF THE YEAR! http://is.gd/5lvmLThis is big news! Please RT! #

- @LenPenzo @SusanTiner I couldn’t help it. That kicked over the giggle box. in reply to LenPenzo #

- RT @copyblogger: You’ll never get there, because “there” keeps moving. Appreciate where you’re at, right now. #

- Why am I expected to answer the phone, strictly because it’s ringing? #

- RT: @WellHeeledBlog: Carnival of Personal Finance #235: Cinderella Edition http://bit.ly/7p4GNe #

- 10 Things to do on a Cheap Vacation. https://liverealnow.net/aOEW #

- RT this for chance to win $250 @WiseBread http://bit.ly/4t0sDu #

- [Read more…] about Twitter Weekly Updates for 2009-12-19

Twitter Weekly Updates for 2009-12-05

- Guide to finding cheap airfare: http://su.pr/2pyOIq #

- As part of my effort to improve every part of my life, I have decided to get back in shape. Twelve years ago, I wor… http://su.pr/6HO81g #

- While jogging with my wife a few days ago, we had a conversation that we haven’t had in years. We discussed ou… http://su.pr/2n9hjj #

- In April, my wife and I decided that debt was done. We have hopefully closed that chapter in our lives. I borrowed… http://su.pr/19j98f #

- Arrrgh! Double-posts irritate me. Especially separated by 6 hours. #

- My problem lies in reconciling my gross habits with my net income. ~Errol Flynn #

- RT: @ScottATaylor: 11 Ways to Protect Yourself from Identity Theft | Business Pundit http://j.mp/5F7UNq #

- They who are of the opinion that Money will do everything, may very well be suspected to do everything for Money. ~George Savile #

- It is an unfortunate human failing that a full pocketbook often groans more loudly than an empty stomach. ~Franklin Delano Roosevelt #

- The real measure of your wealth is how much you'd be worth if you lost all your money. ~Author Unknown #

- The only reason [many] American families don't own an elephant is that they have never been offered an elephant for [a dollar down]~Mad Mag. #

- I'd like to live as a poor man with lots of money. ~Pablo Picasso #

- Waste your money and you're only out of money, but waste your time and you've lost a part of your life. ~Michael Leboeuf #

- We can tell our values by looking at our checkbook stubs. ~Gloria Steinem #

- There are people who have money and people who are rich. ~Coco Chanel #

- It's good to have [things that money can buy], but…[make] sure that you haven't lost the things that money can't buy. ~George Lorimer #

- The only thing that can console one for being poor is extravagance. ~Oscar Wilde #

- Money will buy you a pretty good dog, but it won't buy the wag of his tail. ~Henry Wheeler Shaw #

- I wish I'd said it first, and I don't even know who did: The only problems that money can solve are money problems. ~Mignon McLaughlin #

- Mnemonic tricks. #

- The Wilbur and Orville Wright Papers http://su.pr/4GAc52 #

- Champagne primer: http://su.pr/1elMS9 #

- Bank of Mom and Dad starts in 15 minutes. The only thing worth watching on SoapNet. http://su.pr/29OX7y #

- @prosperousfool That's normal this time of year, all around the country. Tis the season for violence. Sad. in reply to prosperousfool #

- In the old days a man who saved money was a miser; nowadays he's a wonder. ~Author Unknown #

- Empty pockets never held anyone back. Only empty heads and empty hearts can do that. ~Norman Vincent Peale #

- RT @MattJabs: RT @fcn: What do the FTC disclosure rules mean for bloggers? And what constitutes an endorsement? – http://bit.ly/70DLkE #

- Ordinary riches can be stolen; real riches cannot. In your soul are infinitely precious things that cannot be taken from you. ~Oscar Wilde #

- Today's quotes courtesy of the Quote Garden http://su.pr/7LK8aW #

- RT: @ChristianPF: 5 Ways to Show Love to Your Kids Without Spending a Dollar http://bit.ly/6sNaPF #

- FTC tips for buying, giving, and using gift cards. http://su.pr/1Yqu0S #

- .gov insulation primer. Insulation is one of the easiest ways to save money in a house. http://su.pr/9ow4yX #

- @krystalatwork It's primarily just chat and collaborative writing. I'm waiting for someone more innovative than I to make some stellar. in reply to krystalatwork #

- What a worthless tweet that was. How to tie the perfect tie: http://su.pr/1GcTcB #

- @WellHeeledBlog is giving away 5 copies of Get Financially Naked here http://bit.ly/5kRu44 #

- RT: @BSimple: RT @arohan The 3 Most Neglected Aspects of Preparing for Retirement http://su.pr/2qj4dK #

- RT: @bargainr: Unemployment FELL… 10.2% -> 10% http://bit.ly/5iGUdf #

- RT: @moolanomy: How to Break Bad Money Habits http://bit.ly/7sNYvo (via @InvestorGuide) #

- @ChristianPF is giving away a Lifetime Membership to Dave Ramsey’s Financial Peace University! RT to enter to win… http://su.pr/2lEXIT #

- @The_Weakonomist At $1173, it's only lost 2 weeks. I'd call it popped when it drops back under $1k. in reply to The_Weakonomist #

- @mymoneyshrugged It's worse than it looks. Less than 10% of Obama's Cabinet has ever been in the private sector. http://su.pr/93hspJ in reply to mymoneyshrugged #

- RT: @ScottATaylor: 43 Things Actually Said in Job Interviews http://ff.im/-crKxp #

- @ScottATaylor I'm following you and not being followed back. 🙁 in reply to ScottATaylor #

Side Hustle: The Garage Sale Preparation

We had a garage sale last week, as a wrap-up to the April 30 Day Project. We got rained out halfway through the first day of our 3-day sale, but we still managed to clear $1500. We held the sale in our neighbor’s garage because it had more space and better visibility.

Wednesday night, while carrying boxes over, I missed the step to their property from our driveway and crashed while carrying three boxes. That’s a twisted ankle and a bleeding knee. Naturally, while I’m hopping and swearing, everyone is concerned that I’m okay. The worry-warts. Anyway, it hurt, so we stopped setting up while we still had a few boxes left in the basement.

[ad name=”inlineleft”]Thursday morning, I decided to show them all. At 5:30AM, before anybody else is strongly considering the possibility of maybe thinking about getting ready to hit the snooze button, I decided to get the rest of the boxes ready. They’d all wake up, worried about how I’m feeling, asking if I’m to stiff to carry boxes. The best way to show them they don’t need to worry would be to have all of the boxes dealt with before they woke up. So I started. Up and down the stairs, with a stiff, twisted ankle, gloating to myself about how tough I was…BOOM, down the stairs. I was on my back, sliding down the stairs. I caught a stair-tread in the small of my back and another on the point of my tailbone. Mommy?

After I stopped twitching on the floor at the base of the stairs, I managed to get the last of the boxes ready. Instead of sympathy, I spent the rest of the weekend getting asked if I needed an inflatable doughnut to sit on. There are places I’d prefer not to have bruised.

Unpacking the boxes made me glad that everything was priced. We spent 6 weeks going through our entire house–every room, every dresser, every drawer–to eliminate the clutter. As something went into a box, it got priced, so we didn’t have to do it all at the last minute. That is the most important time-saving step for a garage sale. Price it as you pack it. You don’t want to waste hours pricing stuff while tripping over potential customers.

Another preparation tip to do early: Find tables! Ask around. You’d be surprised at who has a dozen folding tables collecting dust in his basement. It’s better to borrow that to rent. The best price I found was $17.50 to rent an 8′ X 30″ table for a week. We didn’t have to do that, but we thought we would have to. I borrowed a few, found a few, and built a few out of sawhorses.

The week before the sale, we placed an ad in the paper. When I placed the ad, the paper called to suggest we change it from running the weekend before to running just the days of the sale. I agreed, to a point, but their Sunday circulation is miles ahead of the weekday circulation, so why pay to run an ad nobody will see on Thursday? I ran it Sunday through Tuesday, because I wanted the Sunday ad and we got 3 consecutive days in the price. Did I actually know better than the paper’s sales-weasel? Who knows? I think I made the right decision.

The Sunday before the sale, I posted an ad on Craigslist. Interesting fact: little old ladies use Craiglist to plan their garage-sale adventures.

Two days before the sale, we made signs. Bright pink signs with brighter yellow starbursts. They were all simple. “Mega Sale! 8-5” followed by an arrow and our address. Simple, easy-to-read, and bright. The morning of the sale, after the ibuprofen kicked in, I put the signs up. When you make signs out of paper, always include a crossbar. It rained a lot the first day of the sale, so the signs wilted. The second morning, I went out with some duct tape and crossbars and fixed them all.

The day before the sale, we got cash and change. We had $50 in 1s and 5s and $25 in silver change. No pennies. Nothing was priced to make us need them.

The morning of the sale, we set up two canopy tents in the driveway and pulled the prepared-and-filled table out under them. We finished stacking as much as we could on the tables and called it “open”. There were a few boxes we couldn’t put out due to the rain. We simply ran our of room. At noon, $65 into the sale, we decided enough was enough and shut down–cold, wet, and miserable. Lunch and a nap made the day better.

Later, I’ll discuss the other parts of our successful sale.

Note: The entire series is contained in the Garage Sale Manual on the sidebar.

Update: This post has been included in the Money Hacks Carnival.

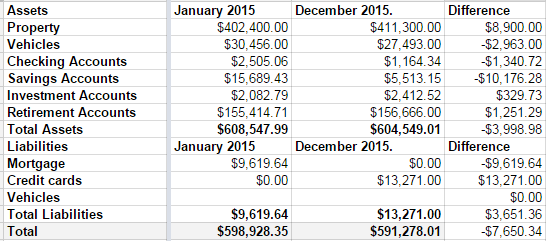

Net Worth and other stuff

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

- We’re going to save for college at a rate we should have started 10 years ago.

- We’re going to max out both of our retirement plans.

- We’re going to take some nicer family vacations.

- We’re going to buy a pony.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

Teaching My Child about Money in a Way I Was Not Taught

When I was in high school and working 15 to 20 hours a week, my mom gave me free rein to use the money I earned as I would like. Actually, she said nothing to me about saving for college or putting some money into savings.

When I had friends who complained that they had to put away some of their earnings, I commiserated with them. How unfair of their parents to make them save some of their money! They worked hard for their money, often at crappy part-time jobs. They deserved to spend the money any way they saw fit.

The way I saw it, why save for college? According to financial aid rules, if the student has any savings, she would have to use the majority of it to pay for college. How unfair. To add insult to injury, if prospective college students have some savings, they would qualify for less financial aid, which often meant fewer student loans.

The injustice.

Yes, it was better to spend my hard earned money than save it and be penalized.

No one told me differently. In fact, many people in my family agreed with me and encouraged me to buy a used car to get to and from my job. Of course, I paid the loan payments for the car, the gas I used and my insurance out of money from my job. That was a responsible use of money, but I also went out to eat with friends, a lot. At 16, I was going out to eat with my friends twice a week at least.

However, my plan worked perfectly. When I went to college, I didn’t have to use any of my hard earned cash. No, not me, because I hadn’t saved anything. Instead, I left college with nearly $20,000 in student loan debt. I took two years off and paid down as much student loan debt as I could, getting it down to about $8,000, but then I went to graduate school and took on more student loan debt. I graduated with nearly $25,000 in debt total. I am still paying on it today, 13 years later.

Now that I am the parent, I am one of those “awful” parents who makes her kids save. My son knows when he gets his allowance, some goes to save, some goes to donate, and some goes to spend. True, it makes me cringe when he uses his spend money on little trinkets like temporary tattoos, stickers, and gum, but I keep silent. He did the work to earn the money, and he can spend it as he likes. However, I am inflexible with saving; that money must be set aside. When he goes to college, I expect that he will have to use the majority of that money. Rather than seeing it as a waste, I see it as an important component of his financial education. Spending his money to pay a portion of his college education will hopefully make him take college more seriously.

Meanwhile, I have already begun having chats with him about money, spending, and budgeting. He watches his dad and I work hard to pay down our debt with gazelle intensity. He sees me use a calculator at the grocery store to see how much our groceries will be.

Ultimately, he will make his own financial decisions as he grows up, but I plan to teach him throughout these important years so that even if he turns into a spendthrift, he will have a firm financial understanding to revert to as he ages. While my mom taught me how to stretch money further, she never taught me how to save; I hope saving is a lesson my son takes with him throughout his adulthood.

How do you teach your kids about money management?

Melissa writes at Fiscal Phoenix where she encourages people to rise from the ashes of their financial mistakes as she and her husband are doing.

Apple Launches iPad Air in November

With a lighter and thinner chasis, the newly announced iPad Air has a more powerful processor with a great new design and performance features that’s sure to continue Apple’s trend setting reputation. Apple senior vice president Phil Schiller is calling it the biggest leap forward for a full-sized iPad. We expect people have already started packing overnight bags for their long wait on the sidewalks outside the stores.

Apple is promoting its newest innovation as having the power of lightness, hence the addition of the “Air” moniker. That’s because the iPad Air weighs a mere pound and even then doesn’t feel like it. It’s 7.5 millimeters thin and has a design that might remind you of the iPad mini. It’s been engineered with a smaller bezel that shrinks the tablet without losing any screen size. The new dimensions and weight actually makes it easier to hold the tablet in one hand.The device will certainly impress its fans with its incredible power. The new A7 chip has a 64 bit architecture, providing graphics and CPU processing that’s significantly faster than the previous version. Working alongside the A7, the M7 motion co-processor, according to Apple, provides a graphic performance that’s over 70 times faster than the processor in the original iPad model. In fact, in terms of graphics, the Retina Display is likely the most impressive aspect of the new iPad. Graphics promise to render at two times the speed of the last iPad. The pared down bezel makes the screen stand out prominently.The iPad Air is supposed to give a user the chance to do more in more places with an advanced wireless connection. It’s faster than ever in more locations than ever before. The iPad Air brings a WiFi performance twice the speed of the last iPad. It utilizes two antennas instead of one, and MIMO, the latest in communication and smart antenna technology. The WiFi and Cellular model will support more LTE brands, offering greater support and quicker connection anywhere in the world.

With almost a half million apps already available for the iPad, you have a great head start on things to do. Apps built into the iPad Air will include solutions for routine tasks, like web surfing and checking email. A number of previously apps that had to be purchased are now free, such as iMovie, Keynote, iPhoto, GarageBand and Pages. Popular apps for other Apple products, they have all been upgraded to work with iOS 7 and the iPad. Quickly put together an original song or detail a presentation anywhere. As a lot of apps are developed solely for Apple products, these can look stunning on their displays.

The iPad Air’s current launch date is November 1. It will come in black and gray or silver and white. It will start at $499 for a 16 gigabyte WiFi version. This is $100 more than previous generation launches, but supporters say the consumer is getting more screen real estate. The Cellular model will retail for $629. The iPad 2 will continue in the stores for $399.