- RT @Dave_Champion Obama asks DOJ to look at whether AZ immigration law is constitutional. Odd that he never did that with #Healthcare #tcot #

- RT @wilw: You know, kids, when I was your age, the internet was 80 columns wide and built entirely out of text. #

- RT @BudgetsAreSexy: RT @FinanciallyPoor "The real measure of your wealth is how much you'd be worth if you lost all your money." ~ Unknown #

- Official review of the double-down: Unimpressive. Not enough bacon and soggy breading on the chicken. #

- @FARNOOSH Try Ubertwitter. I haven't found a reason to complain. in reply to FARNOOSH #

- Personal inbox zero! #

- Work email inbox zero! #

- StepUp3D: Lame dancing flick using VomitCam instead or choreography. #

- I approve of the Nightmare remake. #Krueger #

Effen Carpets, Effen Pets

We’ve got pets. Lots of pets.

- 4 cats

- 3 kids

- 2 pythons

- 1 dog

- 1 hamster

And yours truly.

I count, I make a good mess.

Pets have hair. Well, except for the python and the horrible abominations of mis-evolved Chinese food known as bald cats.

Pet hair gets every-damn-where.

A few weeks ago, we watched our friend’s dogs for a few days.

Those things pee. Not in the backyard like good dogs, but on the girls’ bedroom carpet.

I hate pee.

Not my own, of course.

I really, really hate animal pee in my house.

So we got the carpets cleaned. Linda told me it would be a bit more than normal, since we were going to get the air ducts cleaned at the same time. I was fine with that. Animal hair gets everywhere, and in the ducts, it makes the furnace and air conditioner work poorly.

Then, I got an email alert from Capital One.

Seven hundred freaking dollars!

That’s about $400 more than I was expecting.

Not flipping thrilled! <—-Understatement.

Thankfully, we have money tucked aside for crap like this, but if stuff keeps coming up, we’re going to be hosed.

Net Worth Update

Now that my taxes are done and paid for, I thought it would be nice to update my net worth.

In January, I had:

Assets

- House: $252,900

- Cars: $20,789

- Checking accounts: $3,220

- Savings accounts: $6,254

- CDs: $1,105

- IRAs: $12,001

- Investment Accounts: $1,155

- Total: $297,424

Liabilities

- Mortgage: $29,982

- Credit card: $18,725

- Total: $48,707

Overall: $249,717.00

Here is my current status:

Assets

- House: $240,100 (-12,800) Estimated market value according to the county tax assessor. This will be going down in a few months when the estimates are finalized for the year. I don’t care much about this number. We’re not moving any time soon, so the lower the value, the lower the tax assessment.

- Cars: $15,857 (-4,932) Kelly Blue Book suggested retail value for both of our vehicles and my motorcycle.

- Checking accounts: $4,817 (+1,597) I have accounts spread across three banks. I don’t keep much operating cash here, so this fluctuates based on how far away my next paycheck is.

- Savings accounts: $6,418 (+164) I have savings accounts spread across a few banks. This does not include my kids’ accounts, even though they are in my name. This includes every savings goal I have at the moment. I swept a chunk of this into an IRA to lower my tax bill, which is also why my IRA balance is up as much as it is.

- CDs: $1,107 (+2) I consider this a part of my emergency fund.

- IRAs: $16,398 (+4,397) I have finally started to contribute automatically. It’s only $200 at the moment, but it’s something.

- Investment Accounts: $308 (-847) I pulled most of this out and threw it at a credit card.

- Total: $285,005 (-12,419)

Liabilities

- Mortgage: $28,162 (-1,820)

- Credit card: $16,038 (-2,687) This is the current target of my debt snowball. This has actually grown a bit over the last week. I did a balance transfer that cost $400, but it gives me 0% for a year, versus the 9% I was paying. That will pay for itself in 3 months, while simplifying my payments a bit and saving me almost a thousand dollars in payments this year.

- Total: $44,200 (-4,507)

Overall: $240,805 (-8,912)

Well, I lost some net worth over the last quarter, but it’s still a good report. If I disregard the change in value of my house and cars–two thing I have no control over–my overall total would have gone up almost $9,000.

All in all, it’s been a good year for me, so far, though paying off that credit card by fall is going to be a challenge.

Transparency

A friend–let’s call him me–recently had a bit of a hangup with a business relationship.

On a long-term project, there were some unavoidable setbacks. My friend decided to work through them, hoping to get everything back up to speed…before the customer noticed.

It’s a funny thing, but customers like to look at status reports on long-term projects. A couple of months after the biggest problem, the customer called my friend wanting an in-person status update. They told him to be prepared for an uncomfortable conversation.

Crap.

Now, the setbacks were truly unavoidable. Things came up that were entirely outside the realm of my friend’s control, but he had to deal with them anyway. When the problems were laid out in front of the customer, it went from uncomfortable to a discussion on how to expand the business relationship.

Transparency for the win.

Bad things happen. Anybody who doubts this is clearly not equipped to deal in the adult (that’s adult in the “grown-up” sense, not adult in the “porn” sense) world. Companies know that bad things can happen to derail a project. They are going to be more interested in how you get the project back on track than anything else.

When things go wrong, be open about it. Your customers/family/friends/one-night-stands will appreciate not having to wonder what’s going on.

Let me check….

A few days ago, I asked a coworker if she wanted to go out for lunch. She said she’d have to check her bank account before she decided.

What?

If you have to check your bank balance to know if you can afford something, you can’t afford it. It really is that simple.

Now, strict budgets aren’t for everyone, but everyone should know how much money they have available to spend. If you don’t know what you have to spare, you need to set up a budget.

Period.

After you’ve done that, you can ignore it, with the exception of knowing how much you have available to blow on groceries, entertainment, and other discretionary purchases.

If you don’t know where your money needs to go, how can you determine how much you can spend on the things you want?

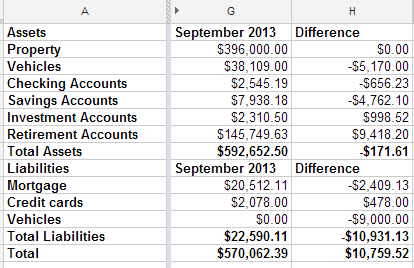

Net Worth Update

Time to update my net worth. Here are the highlights:

We paid off the Tahoe we bought last fall, but the value of my Pacifica fell $5,000 since April. That made me sad.

In August, we had $1000 worth of car repairs and $5500 for braces. We had most of the money saved for braces, but had to juggle some savings accounts around to cover it. We didn’t have enough money in our car repair fund to cover the repairs. Between the two, we beat up our credit card a bit more than usual last month. I’m not happy about it, but I’m confident we’ll catch up this month. My current goal is to get that paid off by the end of September. If I do, I should be able to avoid paying any interest on the balance.

All in all, it’s not bad progress. Our assets dropped $171.61, but our liabilities dropped $10,931.13, so our net worth is up $10,000. You won’t catch me complaining about that.

What’s going to happen in the future? We’re going to remodel both of our bathrooms this winter. We’re hoping to buy a pony before spring.

I’m excited to see our budget evolve over the next few months.

My wife is working and my kids are all in school. With the way our schedules work, we’ve pulled the youngest two out of daycare, so that expense is gone. And there are a couple of other things in the works that I’ll be sharing when they are finalized. If things progress the way they are looking, we’re going to spend the winter living off of my income, and saving her’s. That makes me feel like putting on an ant costume and kicking grasshopper’s butt all over town.