Please email me at:

![]()

Or use the form below.

[contact-form 1 “Contact form 1”]

The no-pants guide to spending, saving, and thriving in the real world.

Please email me at:

![]()

Or use the form below.

[contact-form 1 “Contact form 1”]

If you keep doing what you’ve always done, you’re going to keep getting what you you’ve always gotten. One of the hardest things about getting out of debt is changing your habits. You need to break your habits if you’re going to get yourself to a new place, financially.

How can you do that? Habits aren’t easy to break. Ask any smoker, junkie, or overeater what it takes. There are a lot of systems to break or establish habits, but they don’t all work for everyone.

Here are my suggestions:

Habits—especially bad habits—are hard to break. There is an entire self-help niche dedicated to breaking habits. Hypnotists, shrinks, and others base their careers on helping others get out of the grip of their bad habits, or conning them into thinking it is easy to do with some magic system. How do you avoid or break bad habits?

Today, I continuing the series, Money Problems: 30 Days to Perfect Finances. The series will consist of 30 things you can do in one setting to perfect your finances. It’s not a system to magically make your debt disappear. Instead, it is a path to understanding where you are, where you want to be, and–most importantly–how to bridge the gap.

I’m not running the series in 30 consecutive days. That’s not my schedule. Also, I think that talking about the same thing for 30 days straight will bore both of us. Instead, it will run roughly once a week. To make sure you don’t miss a post, please take a moment to subscribe, either by email or rss.

On this, day 2 of the series, you need to gather all of your bills: your electric bill, your mortgage, the rent for your storage unit, everything. Don’t miss any.

Go ahead, grab them now. I’ll wait.

Did you remember that thing that comes in the plain brown wrapper every month? You know, that thing you always hope your neighbors won’t notice?

Now, you’re going to sort all of the bills into 5 piles.

Pile #1: These are your monthly bills. This will probably be your biggest pile, since most bills are organized to get paid monthly. this will include your credit cards, mortgage(do you rent or buy?), most utilities and your cellphone.

Pile #2: Weekly expenses. When I look at my actual weekly bills, it’s a small stack. Just daycare. However, there are a lot of other expenses to consider. This stack should include your grocery bill, gas for your car, and anything else you spend money on each week.

Pile #3: Quarterly and semiannual bills. I’ve combined these because there generally aren’t enough bills to warrant two piles. My only semi-annual bill is my property tax payment. Quarterly bills could include water & sewer, maybe a life insurance policy and some memberships.

Pile #4: Annual bills. This probably won’t be a large pile. It will usually include just some memberships and subscriptions.

Pile #5: Irregular bills. The are some things that just don’t come due regularly. In our house, school lunches and car repairs fall into this category. We don’t have car problems often, but we set money aside each month so our budget doesn’t get flushed down the drain if something does come up.

Now that you have all of your expenses together, you know what your are on the hook for. Next time, we’ll address income.

In this installment of the Make Extra Money series, I’m going to show you how I do keyword research.

Properly done–unless you get lucky–this is the single most time-consuming part of making a niche site. If you aren’t targeting search terms that people use, you are wasting your time. If you are targeting terms that everybody else is targeting, it will take forever to get to the top of the search results.

Spend the extra time now to do proper keyword research. It will save you a ton of time and hassle later. This is time well-spent.

If you remember from the last installment, when we researched products to promote, we narrowed our choices down to a few products.

What I’ve done is create a spreadsheet to score the products. You can see the spreadsheet here. I’ll explain the columns as we populate them.

The first column contains the name of the product. Easy. We’ve got 10 products. I’m going to walk through scoring 1 product, then, through the magic of the internet, I’ll populate the rest, and you’ll get to see the results instantly. Wow.

The second column is the global search volume for the exact search term. I base my product niche sites primarily on the demand for a given product. Everything else is a secondary consideration.

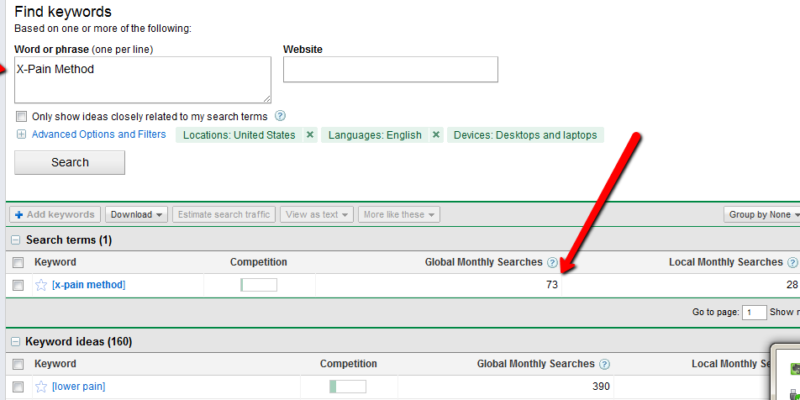

To find the demand for a product, go to the Google Adwords Keyword Tool. In the “word or phrase” box, enter your product name, exactly. In this case, it’s “X-Pain Method”. When the search results come up, change the match type to “Exact”. You should have something like this:

Enter the global search volume in column 2. In this case, it’s 73. Keep this window open, because we’ll be coming back to it.

Column 3 is the search competition. Go to google and enter your product name, in quotes. In this case, “X-Pain Method”. Put the total number of search results in column 3: 223000.

Column 4 is the search competition, but only what appears in a page’s title. Your search query is intitle:”X-Pain Method”, which yields 4400 results.

The next column is for the average PageRank of the first page of search results. For this, I use Traffic Travis. I use the 4th edition, which is paid software, but you can get the free version of version 3, instead. I’ll use version 3 for this example. Open the software and click on “SEO Analysis” on the bottom left of the screen. Put your search term (“X-Pain Method”) in the “phrase to analyze” and set the “Analyze Top” to 10, then hit “Analyze”. When it’s done running, just add up all of the PRs and divide by 10. Ignore Travis’s difficulty rating.

Now, for the rest of the columns, we’re going to look at the keyword tool again. We’re going to pick 3 alternate search terms. Here are the criteria:

Once we pick the keywords, we’ll throw them into google to get the competition, just like we did to populate column 2.

“Exercises for back pain” has medium competition and 1900 monthly searches. It also has an estimated cost-per-click of $3.02, which means people are paying for this.

“Lower back pain exercises” has 6600 searches and medium competition. It’s actually on the lower end of medium, so it looks really promising.

“Lower back” has 4400 searches and low competition, with a CPC of $6.24. This should be a good one. Scratch that. It has 40 million search results, but only 4400 searches. That’s a lot of competition for a small market.

Instead, I’m going to search for “cure back pain” in the keyword tool and see what I get. “Upper back pain” is better. Low competition, 18000 searches each month, and only 2000000 competing search results. Now, I’ll score it.

You really want at least 500 searches per month for the product name. More than 2500 is better. I’m going to assign 1 point per 500 monthly searches.

You also want a lower number of search results. Less than 10,000 is ideal. Less than 100,000 is still decent. More than 250,000, I’d walk. So, under 10,000 gets 5 points. Under 50,001 gets 4. Under 100,001 gets 3. Under 200,001 gets 2. Under 250,001 gets 1. Any higher gets 0.

The ideal intitle search will have less than 2000 results. More than 100,000 is too time-consuming to deal with. 0-2000: 5 points; 2001-10,000: 4 points; 10001-25000: 3 points; 25001-50000: 2 points; 50001 to 100000: 1 point.

The perfect product will have the first page of search result all with a PageRank of 0. That’s a 5 point product. I’ll knock off half a point for every point of average PR.

The related terms are more relaxed. They are what’s known as “Latent Semantic Indexing” (LSI) terms. We will be creating articles to match those search terms, mostly to make our niche site look as natural and real as possible. Any actual traffic those pages drive is just gravy. Points for the related searches start at 10 and get 1 point knocked off for each 3 million results. We’ll be treating the 3 terms as one for this score.

That gives us a perfect score of about 25. There’s no actual upper limit, since the score for the search volume has no upper limit. X-Pain Method scored 18.22.

Now, excuse me a moment while I score the rest.

I’m back. Did you miss me?

I’ve finished scoring each of the products and sorted the results by score. The clear winner is the back pain product, but the lack of searches bothers me. The wedding guide looks much nicer, especially if I target the phrase “wedding planning guide” during the SEO phase of the project. That change alone brings the score almost to first place.

Frankly, I’d take either 2nd or 3rd place over the back pain product. The bare numbers don’t support it, but my judgement tells me they are better products to promote.

There is one final step before deciding on the product. I have to buy it. I can’t review the product without seeing it and I can’t promote it without approving of it.

That’s the secret to ethical niche marketing, you know. Only promote good products that you’ve personally read, watched, or used.

When you realize that you’ve buried yourself in debt and decide to get out from under that terrible burden, the first thing you’ve got to do is build a budget because, without that, you’ve got no way to know how much money you have or need. After you’ve got a budget, you’ll start spending according to whatever it says. Hopefully, you’ll stay on budget, but what happens when an emergency does come up? What do you do when your car dies? When you suddenly find out your kids needs vision therapy? How do you manage when your job suddenly gets shipped off to East De Moines?

Your budget isn’t going to help you meet those expenses. Most people don’t have enough money in their bank account to make it all the way to the next payday, let alone enough to keep the lights on and food on the table. How can you possibly hope to deal with even the little things that come up?

You whip out your emergency fund.

The problem with a budget is that it does a poor job of accounting for the unexpected. That’s where an emergency fund comes in. An emergency fund is money that you have set aside in an available-but-not-too-accessible account. Its sole purpose is to give you a line of defense when life rears up and kicks you in the butt. Without an emergency fund, everything that comes unexpectedly is automatically an emergency. With an emergency fund, the things that come up are merely minor setbacks. Without an emergency fund, your budget is nothing but a good intention waiting to get shattered by the next thing that comes along. With an emergency fund, you are managing money. Without it, it’s managing you.

Every “expert” has their own opinion on this. Dave Ramsey recommends $1000 to start. Suze Orman says 8 months. The average time spent looking for work after losing your job is 24.5 weeks(roughly 6 months), so I recommend 7 months of expenses. That’s enough to carry you through an average bout of unemployment and a little more, but that’s not a goal for your first steps toward financial perfection. To start with, get $1000 in a savings account. That’s enough to manage most run-of-the-mill emergencies, without unduly delaying the rest of your debt repayment and savings goals.

Let’s not kid ourselves, $1000 is a lot of money when can barely make it from one check to the next. Unfortunately, this vital first step can’t get ignored. If you really work at it, you should be able to come up with $1000 in a month or so. Here are some ideas on how to manage that:

Dave Ramsey’s advice is to get your fund up to $1000 and then leave it alone until your debt is paid off. Screw that. I’ve got money going into my fund every month. It’s only $25 per month, but over the last two years, it has almost doubled my fund. Don’t dedicate so much money that you can’t meet your other goals, but don’t be afraid to keep some money flowing in .

When can you pull the money out? That is entirely up to you. I have ju st two points to make about withdrawing from your emergency fund:

An emergency fund makes your life easier and your budget possible when the unexpectable happens. Don’t forget to fund yours.

How much money do you keep in your emergency fund? What would it take to get you to spend it?

Today, I am continuing the series, Money Problems: 30 Days to Perfect Finances. The series will consist of 30 things you can do in one setting to perfect your finances. It’s not a system to magically make your debt disappear. Instead, it is a path to understanding where you are, where you want to be, and–most importantly–how to bridge the gap.

I’m not running the series in 30 consecutive days. That’s not my schedule. Also, I think that talking about the same thing for 30 days straight will bore both of us. Instead, it will run roughly once a week. To make sure you don’t miss a post, please take a moment to subscribe, either by email or rss.

On this, Day 10, we’re going to talk about debt insurance.

Debt insurance is insurance you pay for that will pay your lender in the event of your death, dismemberment, disfigurement, disembowelment, or unemployment. Exactly what is covered varies by insurer, type of debt, and what you are willing to pay for.

Private Mortgage Insurance(PMI) is a common form of debt insurance. Generally, if you take out a mortgage with a down payment under 20%, you’ll be expected to pay for PMI. According to the Homeowners Protection Act of 1998, you have the right to request your PMI be cancelled after reducing your loan amount to 78% of the appraised value of the property. That ensures that the lender will be able to recoup their money by seizing the mortgaged property if you should happen to fall under a bus or get hit by a meteorite.

Another common form of debt insurance is for your credit cards. Card companies love it when you buy their insurance. If you buy their life insurance, your card is paid off when you die. Disability insurance pays it if your get hurt. Unemployment insurance…you get the idea.

Here’s the deal: Get life insurance and disability insurance separately. It’s cheaper than getting it through your credit card company and let’s you get enough to actually live on if something tragic happens. Unless, of course, you die. Then it will leave enough for your heirs to live on.

As far as unemployment insurance, build up your emergency fund instead. That’s money that gives you options. Credit card insurance is money flushed down the toilet. Many of these policies cost 1% of your balance. If you’ve got a $5,000 balance, that will mean you are paying $50 per month. By comparison, if you’ve got a 9.9% interest rate, you’ll be paying about $40 per month in interest.

Debt insurance is a bad idea, if you can possibly avoid it. A combination of life insurance, disability insurance, and an emergency fund provide better protection with more flexibility.

Your task for today is to review your credit card statements and mortgage agreement and see if you are paying debt insurance on any of it. If you are, cancel and set up the proper insurance policies to protect yourself and your family.