Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

The no-pants guide to spending, saving, and thriving in the real world.

Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

I’m overbanked.

The National Bank, Oamaru, built 1871: a prostyle Palladian portico on a neoclassical facade (Photo credit: Wikipedia)I’ve mentioned that before.

I won’t give up my herd of CapitalOne 360 accounts. I use those to track my savings goals, all 17 of them. I can’t drop my business accounts, my kids’ savings accounts, or the personal accounts that I actually use to spend money.

I do, however, need to simplify a bit.

Last month, I went through the hassle of transferring my 401k from two jobs ago and my IRA from my last job. Now, I’m down to just two retirement accounts. One is for my current job, and the other is a self-managed IRA with Sharebuilder.

Two down.

A few months ago, I went to yet another bank to close an account. My last job offered crappy health insurance, but balanced it out with an HSA. It complicated things, but the actual costs came to almost the same as the previous plan that didn’t have a high deductible. When I left, my HSA just sat there.

Last year, my oldest got braces, so I cleaned out the HSA ahead of time so we could pay up front and save 5% without paying interest.

Another one down.

That’s three accounts down out of 34.

Thirty-four?

Crap. That’s retirement accounts, business accounts, and personal accounts for two adults and three kids.

Bank 1 has the checking account we use, plus two savings accounts, one of which is where we store the rent money until we take a payday.

Bank 2 has a checking account, 16 savings accounts, and stock-trading account, a CD, and two IRAs for my wife and I.

Bank 3 has a checking account, and savings account for each of two businesses I own, a spare set of personal accounts, a savings account for each of the kids, and a checking account for my teenager.

Bank 4 holds nothing but my current 401k.

The only thing I can simplify without sacrificing my organizational jungle is to combine the personal accounts from bank 1 and 3. The problem is that Bank 1 has all of my bill pay information and there is still an account open for my mother-in-law’s estate. We keep that open just in case we find any other checks we need to cash. Bank 3 has my business accounts tied to my personal account and is the bank that my business partner uses, so that’s convenient to move money around.

I may be stuck.

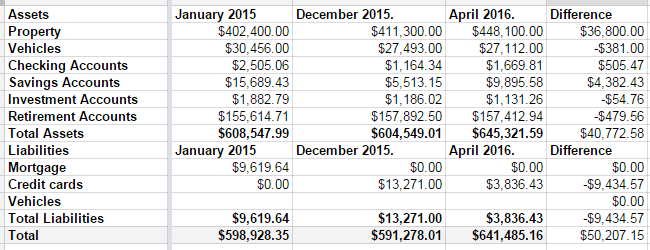

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.

In an effort to promote the crap out of the Yakezie Beta Chapter, I’ve created a search specific to us. This will make it easy to find Beta Challengers to promote.

The current list in the search is:

Live Real, Now

http://www.YourSmartMoneyMoves.com

http://meinmillions.blogspot.com/

http://www.rentingoutrooms.com

http://www.yesiamcheap.com

http://SimpleVesting.com

http://untildebtdouspart.blogspot.com/

http://www.blondeandbalanced.com

http://jamesfowlkes.com/

http://www.mightybargainhunter.com

http://www.beatingtheindex.com

http://www.thepassiveincomeearner.com

http://www.prairieecothrifter.com

http://sustainablepersonalfinance.com/

http://www.toddswanderings.com

More will be added as I have time to dig through the forums. If you’re a Beta Challenger and don’t see your name, leave a comment below and I’ll get you added ASAP.

Today, I discovered our AOL billing information. Turns out we’ve been paying for dial-up via automatic bill paying that we thought we cancelled in 2000. $1,800 later, we called to cancel. Customer service congratulated us on being loyal members for over 13 years. FML -Jay

I am a huge fan of automating my finances. My paycheck is direct-deposited. My savings are automatically transferred from my checking account to my savings account. Almost every bill I receive regularly is set up as an automatic payment in my bank’s bill-pay system. I even have my debt snowball automated.

The only question left is whether it’s possible to automate too far. Can you automate past the point of benefit, straight into detriment? The primary benefit of automation is knowing that you can’t forget a payment. The other benefit is freeing up your attention. You don’t have to give any focus to paying your bills, freeing you to worry about other things.

The problem with the second benefit is the same as the benefit. If you don’t give your bills any attention, how do you know if there is a problem? If something changes–an extra fee or a mis-keyed payment–you won’t notice because you haven’t been giving the bills any focus.

Sometimes, this means you are paying an extra fee without noticing it. Sometimes, if your due date changes, it can mean late fees. Even if nothing goes wrong, you are missing the opportunity to review what you are paying to ensure your needs are being met as efficiently as possible.

What can you do about it? I put a reminder on my Life Calendar to check my bills each month. I pick one bill each month and try to find a way to save money on it. I review the services to make sure they are what I need and if that doesn’t help, I call and ask for a lower price. If it’s a credit card, I ask for a lower interest rate. For the cable company, I ask if they will match whatever deal they have for new customers.

Every company can do something to keep a loyal customer happy. All you have to do is ask.

Do you automate anything? How do you keep track of it all?