LRN got hacked this morning. Thankfully, I backup weekly and subscribe to my own RSS feed. 20 minutes to total restoration.

Twitter Weekly Updates for 2010-06-26

- RT @ScottATaylor: The Guys on "Pickers" should just follow the "Hoarders" teams around- perfect mashup #

- PI/PNK test: http://su.pr/2umNRQ #

- RT @punchdebt: When I get married this will be my marital slogan "Unity through Nudity" #

- http://su.pr/79idLn #

- RT @jeffrosecfp: Wow! RT @DanielLiterary:Stats show 80% of Americns want to write a book yet only 57% have read at least 1 bk in the last yr #

- @jeffrosecfp That's because everyone thinks their lives are unique and interesting. in reply to jeffrosecfp #

- @CarrieCheap Congrats! #CPA in reply to CarrieCheap #

- @prosperousfool I subscribe to my own feed in google reader. Auto backup for in between routine backups. Saved me when I got hacked. in reply to prosperousfool #

- @SuzeOrmanShow No more benefits? I bet the real unemployment rate goes down shortly thereafter. in reply to SuzeOrmanShow #

- Losing power really make me appreciate living in the future. #

8 painless ways to save money

I saw this list on US News and thought I’d give my take on it.

- Get healthy. They are right. It is cheaper to be healthy…in the long run. Short-term, eating crap food is cheaper and obesity doesn’t get expensive until you are older. But remember, long-term planning is important. I intend to enjoy my old age, so I am working on losing weight and exercising. Fat and lazy is easy, but it won’t be in 50 years.

- Rethink your auto insurance. I don’t have an argument here. When I established my initial emergency fund, I set my deductibles to match it. We regularly review our policies to make sure they match what we need.

- Improve your credit scores. I don’t know what they were thinking with this one. If you’ve got lousy credit, it’s hardly painless to improve it. Digging out of a pit of debt hurts.

- Invest on the cheap. This is another one that’s hard to argue with. Low-fee funds are, by definition, cheaper. Will you get a better return on a fund with higher fees? It’s worth checking the historical return to see if the fee is justified.

- Think triple play. They recommend bundling your internet, TV, and phone. It is cheaper, but I don’t recommend it. I don’t like putting all of my eggs in one basket. If the cable goes down, or the the power goes out, I’d still like to be able to make a phone call, if I have to. My landline is independently powered, and I always make sure there is a corded phone plugged in somewhere. My basic landline only runs $35/month, so a bundle won’t save anything for me, anyway.

- Go prepaid with your cell phone. I have a coworker who pays, on average, $5/month for his cell phone. I use mine far more than he does. If you don’t talk much and don’t use data or texting, this can work out well for you.

- Shop online. I do shop online for a lot. I even buy my toilet paper online. For some things, I prefer to shop locally. When a store owner gets to know you, he can get you some fantastic deals, and give you advice that can save you a ton of money.

- Get cash back. I have a couple of decent cash-back credit cards, but I won’t use them. Until all of our credit card debt is paid, I won’t consider making regular use of any form of credit. Your mileage may vary, but that’s the condition I had to set on myself to make our debt plan work.

How many of these ideas do you use?

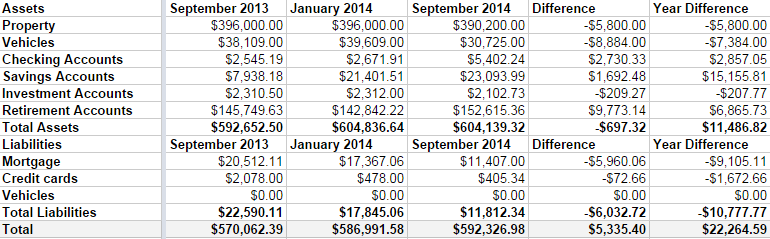

Net Worth Update – September 2014

It’s time for my irregular-but-usually-quarterly net worth update. It’s boring, but I like to keep track of how we’re doing. Frankly, I was a bit worried when I started this because we’ve been overspending this summer and Linda was off work for the season.

But, all in all, we didn’t do too bad.

Some highlights:

- Both of our properties lost around $3000 in value. I’m not worried, because we are keeping them both for the long haul. The rental is basically on auto-pilot, so that’s free money every month.

- We sold a boat that appraised for much less I had estimated in the last few updates. I had it listed for $5000, but it was worth $2000.

- I do have a credit card balance at the moment, but that goes away as soon as my expense check clears the bank, which will be in a day or two.

- We’re in the home stretch with the mortgage. There is $11,407 left to go, and we’ve paid down $9105 in the last year. By this time next year, I want that gone, gone, gone.

I can’t say I’m upset with our progress. We’ve paid down $6000 in debt in 2014, including 3 months with 1 income. We aren’t maxing our retirement accounts, yet, but I’d like to be completely debt free before I do that. It’s bad math, but having all of my debt gone will give me such a warm fuzzy feeling, I can’t not do it.

My immediate goal is to hit a $600,000 net worth by my next update in January. I’m only about $7000 off.

Time to hit the casino. Err, I mean, time to up my 401k contribution from 5% to 7%.

Naked Money

In our house, the bills don’t get hidden. I’ve never tried to hide our finances from our children. I believe doing that is part of the reason I reached adulthood with no brakes. Growing up, finances were almost entirely invisible. Now, I believe is financial transparency.

Now, as a father, I balance the checkbook and pay bills on the laptop in the living room where my children can see me. They see the stack of bills and they watch me balance the checkbook. We discuss how much things cost and how we can cut expenses while the bills are being paid. Even the toddlers know Daddy is doing something important.

My ten-year-old son knows what sales tax is and where to find it on a receipt. He knows what property taxes are and how much they are in our neighborhood. He knows roughly what percentage of a paycheck gets withheld. I work to make my son financially aware. My girls are too young to understand the concept of money, but they will be receiving a thorough financial education as soon as they are able to grasp the concepts.

The hard part is explaining to my son how we screwed up our finances. I’ve shown him my paycheck and discussed our debt. I have explained to him that we were making much less money when we accumulated our doom debt, while maintaining a higher standard of living. Now, when we go to the store, he doesn’t even ask if he can borrow money until we get to his bank account. He has learned to dislike debt in almost all forms. I’m fairly proud that my kid voluntarily practices delayed gratification.

What he doesn’t quite grasp is the idea of living within your means, even if your means are limited. “But, Dad, what if you don’t have much money? Then you have to borrow money for nice things, right?” I’m not sure how to break him of that. Delayed gratification is an understandable concept for him, but the difference between wants and needs seems to be missing. Any ideas?

Reason #45,682 Why It’s Good To Have An Emergency Fund

My mother-in-law died two weeks ago.

It’s sad, but I’m not going to get into the emotional devastation that comes with the death of a loved one here. At least, not today.

Today, I’m going to talk about the money, but not the funeral expenses.

I’m talking about the expense of taking over her stuff. When she died, she was living in her own home, paying her own bills.

Now, we have a small stack of expenses we weren’t planning for.

She had 2 cars. She actively drove one, and kept storage insurance on one that was parked in the driveway. Combined with the homeowner’s insurance, that’s $110/month.

One of the cars has a loan. The car is worth $4000 more than the loan, so it’s not worth letting the bank repossess it. That’s another $200/month.

The gas and electric add $50 to the monthly tab.

Setting aside money for the property tax adds nearly another $200 per month and the first half is due next week.

I rounded the numbers off here, but that’s $562.58 that’s outside of our regular budget and doesn’t address some bills that we paid off instead of arguing with bill collectors while we straighten out the estate.

This is the kind of scenario that makes me happy to have an emergency fund. We are able to pay the property taxes and keep the lights on because of it. A few years ago? The car would have been gone and the house dark within a month.

Now? The emergency fund covers the immediate expenses and we have some breathing room to adjust our budget. For example, the money we were setting aside for our next car is now being earmarked for paying off our surprise car loan.