- Getting ready to go build a rain gauge at home depot with the kids. #

- RT @hughdeburgh: "Having children makes you no more a parent than having a piano makes you a pianist." ~ Michael Levine #

- RT @wisebread: Wow! Major food recall that touches so many pantry items. Check your cupboards NOW! http://bit.ly/c5wJh6 #

- Baby just said "coffin" for the first time. #feelingaddams #

- @TheLeanTimes I have an awesome recipe for pizza dough…at home. We make it once per week. I'll share later. in reply to TheLeanTimes #

- RT @bargainr: 9 minute, well-reasoned video on why we should repeal marijuana prohibition by Judge Jim Gray http://bit.ly/cKNYkQ plz watch #

- RT @jdroth: Brilliant post from Trent at The Simple Dollar: http://bit.ly/c6BWMs — All about dreams and why we don't pursue them. #

- Pizza dough: add garlic powder and Ital. Seasoning http://tweetphoto.com/13861829 #

- @TheLeanTimes: Pizza dough: add lots of garlic powder and Ital. Seasoning to this: http://tweetphoto.com/13861829 #

- RT @flexo: "Genesis. Exorcist. Leviathan. Deu… The Right Thing…" #

- @TheLeanTimes Once, for at least 3 hours. Knead it hard and use more garlic powder tha you think you need. 🙂 in reply to TheLeanTimes #

- Google is now hosting Popular Science archives. http://su.pr/1bMs77 #

- RT @wisebread 6 Slick Tools to Save Money on Car Repairs http://bit.ly/cUbjZG #

- @BudgetsAreSexy I filed federal last week, haven't bothered filing state, yet. Guess which one is paying me and which one wants more money. in reply to BudgetsAreSexy #

- RT @ChristianPF is giving away a Lifetime Membership to Dave Ramsey’s Financial Peace University! RT to enter to win… http://su.pr/2lEXIT #

- RT @MoneyCrashers: 4 Reasons To Choose Community College Out Of High School. http://ow.ly/16MoNX #

- RT @hughdeburgh:"When it comes to a happy marriage,sex is cornerstone content.Its what separates spouses from friends." SimpleMarriage.net #

- RT @tferriss: So true. "Nearly all men can stand adversity, but if you want to test a man's character, give him power." – Abraham Lincoln #

- RT @hughdeburgh: "The most important thing that parents can teach their children is how to get along without them." ~ Frank A. Clark #

Black Friday

- Image by Getty Images via @daylife

Today being the biggest shopping day of the year, I thought I’d get in the game.

First, instead of helping you spend money, I’m going to help you save it. As I’ve mentioned before, I am a big fan of INGDirect. They make it easy to create savings accounts for specific savings goals and they have a decent interest rate. I’ve never had a problem with any of my accounts.

For Black Friday(through Sunday!), they are offering the following:

- Earn $103. Open Electric Orange November 26th – 28th, and make a total of 7 purchases using your Electric Orange Card or Person2Person Payments (or any combination of the two) within 45 days.

- Open a Kids Savings Account November 26th – 28th and we’ll(ING) put a $25 bonus into your new account.

- Use your Electric Orange Debit MasterCard® at least one time from 8:00 AM ET, November 26th – 7:59 PM ET, November 26th, and you’ll be automatically entered into the 100% Cash Back Giveaway.

- Open a 36-month IRA CD with ING DIRECT November 26th – November 28th and get 2.00% Annual Percentage Yield (APY). Ask them about work at home moms and dads spousal IRA.

- Apply online November 26th – 28th for Easy Orange or the Orange Mortgage or call a Mortgage Specialist at 1-866-327-4599 and get up to $2,000 off closing costs. If your costs are less than $2,000, you pay nothing.

- 25% rebate on Sharebuilder trades that execute today or Monday.

Click here to open an account with the best bank to ever hold my money.

Now, to help you spend some money.

All of my websites are hosted by HostGator. I’ve never had noticeable downtime or any technical problems. The one issue I had that couldn’t be controlled by their interface was fixed by technical support in minutes. Not hours, minutes. They are having an amazing deal today. From 5AM to 9AM CST, all of their products are 80% off. The rest of the day, it’s all 50% off. Unfortunately, this doesn’t apply to existing customers, but if you are looking for a website host, paying $35 for 3 years of hosting can’t be beat.

3 Things You Need to Know About Homeowner’s Insurance

- Image by ecstaticist via Flickr

If you are a homeowner, you need homeowner’s insurance. Period. Protecting what is mostly likely the biggest investment of your life with a relatively small monthly payment is so important, that, if you disagree, I’m afraid we are so fundamentally opposed on the most basic elements of personal finance that nothing I say will register with you.

If, however, you have homeowner’s insurance, or–through some innocent lapse–need homeowner’s insurance and you just want some more information, welcome!

The basic principle of insurance is simple. You bet against the insurance company that you or your property are going to get hurt. If you’re right, you win whatever your policy limit is. If you’re wrong, the insurance company cleans up with your monthly premium. Insurance is gambling that something bad will happen to you. If you lose, you win!

Now, there are some things about homeowner’s insurance that you may not realize.

1. Homeowner’s insurance will not protect you against a flood. For that you need flood insurance. The easiest way to tell which policy covers water damage is to see if the water touched the ground before your house. An overflowing river, or heavy rain that seeps through the ground and your foundation are both considered flooding. On the other hand, hail breaking your windows and allowing the rain in or a broken pipe are both generally covered by your homeowner’s policy.

Do you need flood insurance? I would say that, if you live on the coast below sea level, you should have flood insurance. If you’re on a flood plain, you need flood insurance. If you’re not sure, use the handy tool at http://www.floodsmart.gov to rate your risk and get an estimate on premium costs. My home is in moderate-to-low risk of flooding, so full coverage starts at $120.

2. You can negotiate an insurance claim. When you have an insurance adjuster inspecting your home after you file a claim, most of the time they will lowball you. Generous adjusters don’t get brought in for the next round of claims. If you know the replacement costs are higher than they are offering, or even if you aren’t sure, don’t sign! Once you sign, you are locked into a contract with the insurance company. Take your time and do your research. Get a contractor out to give you a damage estimate, if you can.

3. Your deductible is too low. If you’ve built up an emergency fund, you can safely boost your deductible to a sizable percentage of that fund and save yourself a bunch of money. When we got our emergency fund up to about $2000, we raised our deductible from $500 to $1000 and saved a couple of hundred dollars per year. That change pays for itself every 2 years we don’t have a claim. I absolutely wouldn’t recommend this if you don’t have the money to cover your deductible, but, if you do, it can be a great money-saver.

Bonus tip: If you get angry that your homeowner’s insurance doesn’t cover flooding, even if you haven’t had to deal with a flood, and you cancel your insurance out of spite, and you subsequently have a ton of hail damage, your insurance company won’t cover the crap that happened during the window where you weren’t their customer.

Are you one of the misguided masses who prefer to trust their home to fate?

Do you have an insurance horror story?

Credit Cards: How to Pick a Winner

We live in a decidedly credit-centric culture. Whip out cash to pay for $200 in groceries and watch the funny looks from the other customers and the disgust from the clerk. It’s almost like they are upset they have to know how to count to run a cash register.

If someone doesn’t have a credit card, everyone wonders what’s wrong, and assumes they have terrible credit. That’s a lousy assumption to make, but it happens. For most of the last two years, I shunned credit cards as much as possible, preferring cash for my daily spending. Spending two years changing my spending habits has made me comfortable enough to use my cards again, both for the convenience and the rewards.

Having a decent card brings some advantages.

Credit cards legally provide fraud protection to consumers. Under U.S. federal law, you are not responsible for more than $50 of fraudulent charges. many card issuers have extended this to $0 liability, meaning you don’t pay a cent if your card is stolen. Trying getting that protection with a wallet full of cash.

The fraud protection makes it easier to shop online, which more people are doing every day. At this point, there is no product you can buy in person that you can’t get online, often cheaper. How would you order something without a credit card? Even the prepaid cards you can buy and fill at a store will often fail during an online transaction because there is no actual person or account associated with the card. The “name as it appears on the card” is a protective feature for the credit card processors and they dislike accepting cards without it.

If you’re going to use a credit card, you need to make a good choice on which credit card to get. There are a few things to check before you apply for a card.

Annual fee. Generally, I am opposed to getting any card with an annual fee, but sometimes, it’s worth it. If, for example, a card provides travel discounts and roadside assistance with its $65 annual fee, you can cancel AAA and save $75 per year. A good rewards plan can balance out the fee, too. I’m using a travel rewards card that has a 2% rewards plan. That’s 2% on every dollar spent, plus discounts on some travel purchases. In a few months, I’ve accumulated $500 of travel rewards for the $65 fee that was waived for the first year. The math works. A card that charges an annual fee without providing services worth several times that fee isn’t worth getting.

Interest rate. This should be a non-issue. You should be paying off you card completely every month. In a perfect world. In the real world, sometimes things come up. In my case, I was surprised with a medical bill for my son that was 4 times larger than my emergency fund. It went on the card. So far, I’ve only had to pay one month’s interest, and I don’t see the balance surviving another month, but it’s nice that I’m not paying a 20% interest rate. Unfortunately, as a response the CARD Act, the days of fixed rate 9.9% cards seems to be over.

Grace period. This is the amount of time you have when the credit card company isn’t charging you interest. Most cards offer a 20-25 day grace period, but still bill monthly. That means that you’ll be paying interest, even if you pay your bill on time. To be safe, you’ll need to either find a card that has a 30 day grace period, or pay your balance off every 15-20 days. Some of the horrible cards don’t offer a grace period of any length. Avoid those.

Activation fees. Avoid these. Always. There’s no card that charges an activation fee that’s worth getting. An activation fee is an early warning sign that you’ll be paying a $200 annual fee and 30% interest in addition to the $150 activation fee.

Other fees. What else does the card charge for? International transactions? ATM fees? Know what you’ll be paying.

Service. Some cards provide some stellar services, include concierge service, roadside assistance, and free travel services. Some of that can more than balance out the fees they charge. My card adds a year to the warranty of any electronics I buy with it, which is great.

Credit cards aren’t always evil, if you use them responsibly. Just be sure you know what you’re paying and what you’re getting.

What’s in your wallet?

How to Cut Costs on Legal Fees

Occasionally, life goes truly pear-shaped and you’re forced to enter the legal system.

Even if you’re not embroiled in a tawdry, tabloid-fodder divorce, there are still legal issues that everyone needs to address, without exception.

The problem? Or rather, one of many, if you’re having legal problems?

Lawyers are expensive.

Before I go any further:

- If you are having criminal court issues, get a lawyer. Get the best possible lawyer. Really. The cost does not compare to a lifetime in jail, or even 10 years. If you’re facing jail, get the best dang attorney you can find.

- I am not only not an attorney, but I’ve never even played one on TV. I have driven past a law school a couple of times, but never stopped in. I do know several attorney, carry the business cards of a couple and have a couple on my speed dial, just in case. If any of them thought I was giving legal advice, I’d be in trouble. To reiterate: I am not an attorney. This is not legal advice.

- Don’t do a prenuptual agreement at home. A prenup will almost always be found unenforceable if both parties don’t have an attorney.

Where was I? Ah, yes. Lawyers are expensive, but there are ways to mitigate that.

There a couple of things you can handle yourself.

Small claims court, also known as conciliation court. Typical cases in conciliation court include cases involving sums under $7500(varies by state) that involve unpaid debts or wages, claims by tenants to get a security deposit, claims by landlords for property damage, or claims about possession or ownership of property. Fees and procedures vary by state, but generally cost less than $100 to file. The procedures for your state can be found by googling “small claims court” and the name of your state.

Small worker’s compensation cases can be handled yourself, if they don’t involve a demotion or termination related to the injury.

Apartment and car leases are usually simple and straightforward. Read them carefully, but you probably won’t need a lawyer.

You can probably handle your own estate planning and will writing with some decent software. I love Quicken Willmaker. It walked me through a detailed will that takes care of my kids, and gave me advice on financing their futures in the horrible event that I am tragically killed before my wonderousness can fully permeate the world. It also contains forms for promissory notes, bills of sale, health care directives and more. If you have extensive property, I’d still seek an attorney’s advice, but I’d bring the Willmaker will with me to save some time and money.

Purchase agreements. A few years ago, I sold a truck to a friend and accepted payments. I made a promissory note and payment schedule. When he quit paying or calling me, that paperwork was enough to get the state to accept the repossession when I took the truck back.

A simple no-fault divorce is actually pretty painless, on the scale of divorce pain. Again, the procedures vary heavily by state.

Other resources for finding legal information free or cheap include www.legalzoom.com and www.nolo.com.

Have you had to do any of your own legal work? How did it work out?

Make Extra Money Part 4: Keyword Research

In this installment of the Make Extra Money series, I’m going to show you how I do keyword research.

Properly done–unless you get lucky–this is the single most time-consuming part of making a niche site. If you aren’t targeting search terms that people use, you are wasting your time. If you are targeting terms that everybody else is targeting, it will take forever to get to the top of the search results.

Spend the extra time now to do proper keyword research. It will save you a ton of time and hassle later. This is time well-spent.

If you remember from the last installment, when we researched products to promote, we narrowed our choices down to a few products.

What I’ve done is create a spreadsheet to score the products. You can see the spreadsheet here. I’ll explain the columns as we populate them.

The first column contains the name of the product. Easy. We’ve got 10 products. I’m going to walk through scoring 1 product, then, through the magic of the internet, I’ll populate the rest, and you’ll get to see the results instantly. Wow.

The second column is the global search volume for the exact search term. I base my product niche sites primarily on the demand for a given product. Everything else is a secondary consideration.

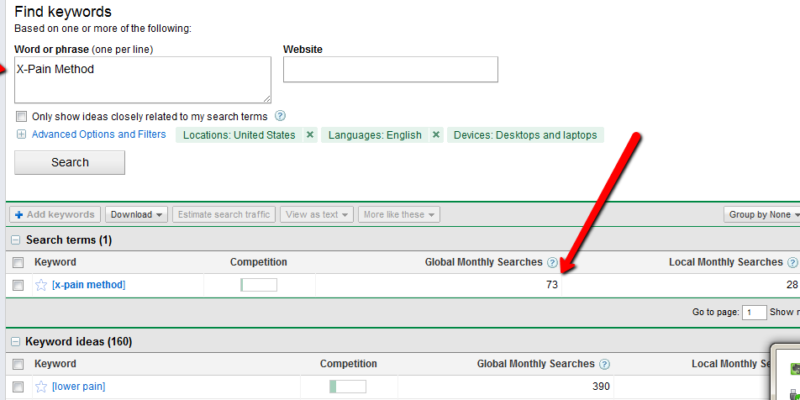

To find the demand for a product, go to the Google Adwords Keyword Tool. In the “word or phrase” box, enter your product name, exactly. In this case, it’s “X-Pain Method”. When the search results come up, change the match type to “Exact”. You should have something like this:

Enter the global search volume in column 2. In this case, it’s 73. Keep this window open, because we’ll be coming back to it.

Column 3 is the search competition. Go to google and enter your product name, in quotes. In this case, “X-Pain Method”. Put the total number of search results in column 3: 223000.

Column 4 is the search competition, but only what appears in a page’s title. Your search query is intitle:”X-Pain Method”, which yields 4400 results.

The next column is for the average PageRank of the first page of search results. For this, I use Traffic Travis. I use the 4th edition, which is paid software, but you can get the free version of version 3, instead. I’ll use version 3 for this example. Open the software and click on “SEO Analysis” on the bottom left of the screen. Put your search term (“X-Pain Method”) in the “phrase to analyze” and set the “Analyze Top” to 10, then hit “Analyze”. When it’s done running, just add up all of the PRs and divide by 10. Ignore Travis’s difficulty rating.

Now, for the rest of the columns, we’re going to look at the keyword tool again. We’re going to pick 3 alternate search terms. Here are the criteria:

- At least 1000 global monthly searches. We want terms that people are searching for.

- Competition bar at medium or less. This bar is just a rough guess on competition, so it’s really an arbitrary exclusion factor, but it helps narrow down the choices.

- A “buying” keyword is preferred, but not necessary. This is a term that indicates people are looking to spend money. “Back pain doctor” is a buying keyword, but it’s not an indicator that someone wants to buy a product, so we’ll skip it. A buying keyword isn’t absolutely necessary, because these will also be the terms we’ll use to generate content later.

- It has to be related to our product.

Once we pick the keywords, we’ll throw them into google to get the competition, just like we did to populate column 2.

“Exercises for back pain” has medium competition and 1900 monthly searches. It also has an estimated cost-per-click of $3.02, which means people are paying for this.

“Lower back pain exercises” has 6600 searches and medium competition. It’s actually on the lower end of medium, so it looks really promising.

“Lower back” has 4400 searches and low competition, with a CPC of $6.24. This should be a good one. Scratch that. It has 40 million search results, but only 4400 searches. That’s a lot of competition for a small market.

Instead, I’m going to search for “cure back pain” in the keyword tool and see what I get. “Upper back pain” is better. Low competition, 18000 searches each month, and only 2000000 competing search results. Now, I’ll score it.

You really want at least 500 searches per month for the product name. More than 2500 is better. I’m going to assign 1 point per 500 monthly searches.

You also want a lower number of search results. Less than 10,000 is ideal. Less than 100,000 is still decent. More than 250,000, I’d walk. So, under 10,000 gets 5 points. Under 50,001 gets 4. Under 100,001 gets 3. Under 200,001 gets 2. Under 250,001 gets 1. Any higher gets 0.

The ideal intitle search will have less than 2000 results. More than 100,000 is too time-consuming to deal with. 0-2000: 5 points; 2001-10,000: 4 points; 10001-25000: 3 points; 25001-50000: 2 points; 50001 to 100000: 1 point.

The perfect product will have the first page of search result all with a PageRank of 0. That’s a 5 point product. I’ll knock off half a point for every point of average PR.

The related terms are more relaxed. They are what’s known as “Latent Semantic Indexing” (LSI) terms. We will be creating articles to match those search terms, mostly to make our niche site look as natural and real as possible. Any actual traffic those pages drive is just gravy. Points for the related searches start at 10 and get 1 point knocked off for each 3 million results. We’ll be treating the 3 terms as one for this score.

That gives us a perfect score of about 25. There’s no actual upper limit, since the score for the search volume has no upper limit. X-Pain Method scored 18.22.

Now, excuse me a moment while I score the rest.

I’m back. Did you miss me?

I’ve finished scoring each of the products and sorted the results by score. The clear winner is the back pain product, but the lack of searches bothers me. The wedding guide looks much nicer, especially if I target the phrase “wedding planning guide” during the SEO phase of the project. That change alone brings the score almost to first place.

Frankly, I’d take either 2nd or 3rd place over the back pain product. The bare numbers don’t support it, but my judgement tells me they are better products to promote.

There is one final step before deciding on the product. I have to buy it. I can’t review the product without seeing it and I can’t promote it without approving of it.

That’s the secret to ethical niche marketing, you know. Only promote good products that you’ve personally read, watched, or used.