This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

The no-pants guide to spending, saving, and thriving in the real world.

This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

It’s almost time to pay Uncle Sam for the privilege of living in the US.

Since my business partner and I just finished our corporate taxes last week, I thought it would be a good time to finish my personal taxes. I’ve got a relatively complicated tax situation. I’ve got personal taxes, my side-hustle taxes, and our side-hustle taxes. I had my side hustle taxes done and my personal taxes were just waiting for the final numbers from our corporate filing. We’re an LLC, run as a partnership, filing as an S-Corp.

I was all set to get about $100 back from my personal and side-hustle #1 taxes. That’s a perfect tax year. No more money out-of-pocket and no free large loans to the government.

Side-hustle #2 ruined that. It started taking off in September, so we’d never paid any estimated taxes. When I added those numbers in, I owed a bit under $2000.

Ick. I hate owing.

Thankfully, I set aside 25% of all of my side-hustle income just to cover this.

It was still too much. What could I do to lower my tax bill?

My IRA!

I’d only contributed $100 to my traditional IRA last year. Contributions are tax deductible and you can make them until April 15th of the following year.

That’s great. I had money sitting in a savings account, earmarked to get wasted by the government, and I had an unused tax deduction that I could still contribute to.

That got it down to a $1000 tax liability.

Was there more? What could I do?

When I paid off my car last year, I started sending half of my car payment to an account earmarked for the next car. I had $1700 sitting there, so I sent $1200 of it to my IRA, leaving $500 to hopefully cover any car repairs that come up. Hope isn’t a good financial strategy, but I’ve also got a straight brokerage account that’d doing pretty well, so I can cash that out, if necessary.

Down to $800.

Contributing a bit over $3000 to my retirement saved me more than $1000 right now. That’s sweet, but I still owed money.

Did I miss something on my first side hustle?

$67 to oDesk? How did I manage to keep my annual oDesk bill down to $67? I had a full-time guy in the Philippines for a while last year, and I regularly hire writers for my niche sites.

So I hit oDesk and ran some reports. I was off in that deduction. By $2400. I have no idea where that $67 came from. Including it dropped my side-hustle profit considerably, and brought my total tax bill to a net $7 refund.

There is a reason I never file my taxes as soon as I finish with Turbo Tax. I always wait a week or two, and I always come up with something I missed. This time, the wait saved me nearly $2000.

Lately, I’ve been traveling for work about twice per month. The trips have generally been to my company headquarters, about 5 hours east of my house, though at the time this goes live, I will be ending another trip in the Chicago area.

Earlier this month, I was out there to conduct some training webinars and enjoy the company Christmas party. After the party, my insomnia kicked in and I couldn’t sleep. At 6AM, I decided to give it up for a lost cause and pack my stuff for the 5 hour drive home.

On no sleep.

The morning after a nasty ice storm.

I do not have a death wish.

Really.

I got packed, ready to go. Then crawled back in bed with the nap timer on my phone set. Thirty minutes later, I checked out of the hotel and got in my car.

I really don’t want to die, though this trip scared me a bit. It’s a long 5 hours, 4.5 of those hours are on one road, driving across southern Wisconsin. Tedious is one word that comes to mind. Mind-numbing and lullaby-driving are two others.

Instead of getting on the highway, I drove to Wal-mart. I stocked up on cigarettes and Rockstar.

Now, I quit smoking 6 years ago when we found out brat #3 was coming a bit faster than we expected. It was purely a financial decision at that point, but breathing turned out to be a nice change, too.

Nicotine is a stimulant with immediate effects. That means, if I start feeling drowsy, I can smoke a cigarette and I quit feeling drowsy while I chug energy drinks.

Good plan, Jason.

It worked. I made it home, then fell on the couch and didn’t move for 4 hours. Then I ate dinner and went to bed.

Unfortunately, even after quitting for 6 years, by the time I got home, it felt like I’d never quit. So I get the joy of quitting again.

By the time you read this, the craving should be gone and I should just be getting ready to climb in my car for a long drive on not enough sleep.

Vegans and hippies won’t enjoy this post.

Friday, I went to a cabin in the woods for a weekend hunting trip with my dad, my brother, and a few other people.

My wife didn’t think it’s a good idea. In fact, she was terrified that I’d walk into the woods and come out in a body bag.

Statistically, it’s safe. Out of 12.5 million hunters, there are only around 100 fatal hunting accidents every year. I think I went hunting for the first time when I was 12, and continued to do so until I was 17, then life started interfering.

That doesn’t matter. By definition phobias aren’t rational. She’s worried and stressing hard.

If she’s had such a hard time with it, why did I go?

First, I asked her six months ago if she’d be all right with the trip. I knew she had some phobias, and have–in fact–tried to make the trip before. Six months ago, she said yes. It was a bit late to back out after I’ve committed to a share of the cabin, bought the bright orange gear, and agreed to drive my brother.

The second reason was more important.

This is one of the few things my dad and I both enjoy. I’m a geek, he’s not. I dig horror and sci-fi, he’s into westerns.

But we both enjoy hunting. The first time he treated me like an adult was the first year we went hunting together, 15 years ago.

My dad taught me to be the man I am. Without him, I have no idea who I’d be or what I’d be doing. My integrity, my work ethic, and my moral code can all be traced to the things he taught me.

This is my chance to spend time with him and have a good time with no TV or whiny kids interfering.

Trading this for a few days of stress at home is something I’m willing to do.

How much would you pay for a kiss from the world’s sexiest celebrity?

That was the focus of a recent study that I can’t find today. There is no celebrity waiting in the wings to deliver the drool, and the study doesn’t name which celebrity it is. That’s an exercise for the reader.

This was a study into how we value nice things.

The fascinating part of the study is that people would be willing to pay more to get the kiss in 3 days than they would to get the tongue slipped immediately.

Anticipation adds value.

Instant gratification actually causes us to devalue the object of our desire.

This goes well beyond “Will you respect me in the morning?”

The last time I talked about delayed gratification, it was in the context of my kids. That still holds true. Kids don’t value the things that are handed to them.

The surprising–and disturbing–bit is that adults don’t, either. If I run out to the store to buy an iPad the first day I see one, I won’t care about it nearly as much as if I spend a week or two agonizing over the decision.

The delay alone adds to the perceived value. The agony turns the perceived value into gold.

If I spend a month searching for the perfect car, the thrill of the successful hunt adds less value than the time it took to do the hunting.

Here’s my frugal tip for today: Delay your purchases. While it may not actually save you any money, you will feel like you got a much better deal if you wait a few days for something you really want.

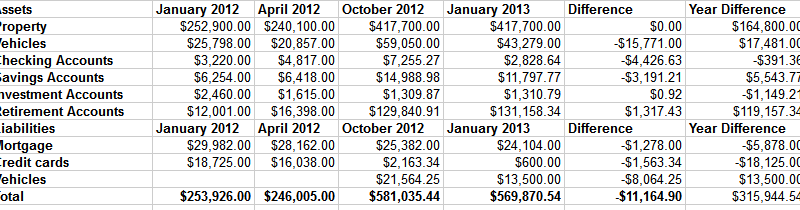

Welcome to the New Year. 2013 is the year we all get flying cars, right?

Here is my net worth update, along with the progress we made over the course of 2012.

As you can see, our net worth contracted by about $11,000. Part of that difference is due to selling our spare cars and–against my better judgement–taking payments with a lien on one of them. That is supposed to be paid off within a couple of months. If not, I’ll play repo man again.

The other part of the difference is in the final preparations for our rental property. The only things left to do are sanding and polishing the hardwood floors and cleaning the living room carpet. The final push to get to this point cost some money. All told, we’re nearly $30,000 into getting the house ready to rent. For the naysayers who think we should have sold it, we would have spent more getting it ready to sell.

Other than that, we’re not doing poorly. Our credit card is still being paid off every month and our mortgage is shrinking. If things continue to go well, we’ll have our truck paid off in a couple of months and the mortgage by mid summer.