This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

The no-pants guide to spending, saving, and thriving in the real world.

This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

Having a well-funded emergency fund is one of the foundation blocks for almost every saving or debt-repayment plan. The theory is that you’ll be better able to weather a financial storm if you don’t have to raid your budget or beat on your credit card every time an unexpected expense rears its ugly head. The number varies based on your pundit and your stage of life, but generally ranges from $1000 to 8 months of your expenses. The money needs to go in a liquid account, so it can be accessed when necessary, but it needs to be completely ignored otherwise. What good is an emergency fund that has been spent?

Now that you have your emergency fund, you are set, right? But what happens when something comes up? When is it okay to spend that money? Emergencies can take so many forms: medical emergencies, car repairs, accidents, a good sale. Wait. What was the last one? What actually constitutes an emergency that is worth shredding your security blanket?

Here are three questions to ask yourself before you spend that money:

Your emergency fund should only be used on things that are important, necessary, and urgent. Anything else should get postponed until you can afford to pay it using your on-budget expense items. As the wise man once said: “Lack of planning does not constitute an emergency.” Of course, if you are in a financially stable situation and willing to take a small risk for a short time, eliminating an entire debt item to save the interest can be the right decision.

What would you be willing to spend your emergency fund on?

I just got an email from INGDirect. To celebrate Independence Day, they are having a sweet, sweet sale.

You can:

Take advantage of all of that and you’ll get $2054 in cash or discounts.

Seriously, this deal rocks. If you don’t have an INGDirect account, get one. There are no overdraft fees and no monthly fees.

The sale ends tomorrow at midnight, so hurry.

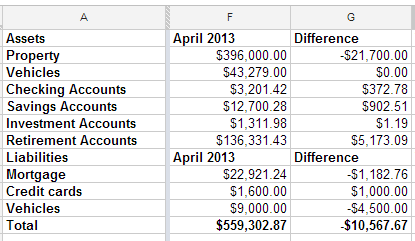

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.

I like to party.

Actually, that’s a lie. I’m too introverted to be a partier. More accurately, I like to throw two parties per year. I am also cheap frugal, so I try not to break the bank feeding fifty of my closest friends.

I have two entirely different parties. The first, known as the “Fourth Annual Second Deadly Sin Barbecue of Doom”, is a daytime party with a lot of food. The second is a Halloween party which takes place at night and refreshments are more of the liquid variety. Two different parties, two different strategies to keep them affordable.

For the Halloween party, meat consists entirely of a meat/cheese/cracker tray and a crock-pot full of either sloppy joes or chili. Quick and easy for about $20. For the barbecue, meat is the main attraction. The menu varies a bit from year to year. Last year, we had burgers, brats, hot dogs, a leg of lamb, pulled pork, and a couple of fatties. The year before, we had a turducken, but no fatties. From a frugal standpoint, the only meat mistakes were the turducken and the lamb. Neither are cheap, but both as delicious. The rest of the meat needs to be bought over the months preceding the party, as they go on sale. Ten pounds of beef, 2 dozen brats, 2 dozen hot dogs and a pork roast can be had for a total of about $75, without having to worry about picking out the hooves and hair. Fatties cost less than $5 to make.

Both parties have chips, crackers and a vegetable tray. Chips are usually whatever is on sale or the store brand if it’s cheaper. Depending on our time management, we try to cut the vegetables ourselves, but have resorted to paying more for a pre-made veggie tray in the past. This runs from $15-30.

For kids and adults who don’t drink, I make a 5 gallon jug of Kool-Aid. Cost: About $3. For adults, I provide a few cases of beer. I don’t drink fancy beer, so this runs about $50. For the Halloween party, I throw open my liquor cabinet. Whatever is in there is available for my guests. The rule is “I provide the beer. If you want something specific, bring it yourself.” I have a fairly well-stocked liquor cabinet, but I don’t stock what I don’t like or don’t use. Part of the stock is what guests have left in the past. I don’t drink much and I buy liquor sporadically when I have a whim for something specific, so raiding the leftovers in the liquor cabinet doesn’t register on my party budget.

While it seems like an obvious and easy way to keep costs down, I do not and will not expect my guests to bring anything. I throw a party to showcase either A) my cooking, or B) my Halloween display. I don’t charge admission. I don’t charge for a glass. I throw a party so I can have fun with the people I care about and the people the people I care about care about. I consider it a serious breach of etiquette to ask anybody to bring something. On the other hand, if someone offers, I will not turn it down.

The most important part of either of my parties is fun. All else is secondary. I seem to be successful, since reservations are made for my spare beds a full year in advance. Last Halloween, people came from 3 states.

How much do my mildy-over-the-top parties cost? The barbecue runs about $150-180 plus charcoal and propane. Yes, I use both. I’ll have 2 propane grills, 1 charcoal grill, and a charcoal smoker running all day. The Halloween party costs $80-100 for the basics. The brain dip costs another $20 and there’s always at least another $50 in stuff that seems like a good idea to serve.

Update: This post has been included in the Festival of Frugality.

When I found myself doing an abrupt unemployment tour this month, the first thing I did was dig into my budget. I did it so I could see how long it would be before our finances got scary and to see what could be eliminated.

Gah! So much could be eliminated.

There were things that I’d set up on automatic payments, added to my budget, then ignored.

There were things that I’d signed up for and used, but didn’t get as much enjoyment out of any more.

Example Number 1: Netflix

We love Netflix. It gets used every single day. But the DVDs often sit on the kitchen counter for a month before we get around to watching them. We clearly don’t need the DVD plan any more.

Example Number 2: Software Subscription

I use some software to track the Google rank of several of my websites. There is an addon that makes the software work much better. The addon costs $20 per quarter. The problem is that I’m not looking at the rankings of these sites any more. Some of the sites have been shut down, or I’m no longer involved with the clients. That makes the paid addon a total waste. I canceled it and told the tracking software to run slower so it would give Google a fit.

Example Number 3: Extra Domains

Hello, my name is Jason and I’m a domain addict. Seriously, for a while, I was buying domains every time I had a good idea for a website. Some of them were developed, and some were sketched out and put on hold. I also bought domains to help with the search engine rankings of the developed websites. I topped out at about 120 domains. All of them were on auto-renew. I’ve been letting them expire, but some didn’t have the auto-renew settings changed, so they (surprise!) renewed automatically.

These are just three examples of several years of development, exploration, and automation of my complicated financial life, and they add up to more than $100 a month essentially wasted.

Here’s what I want you to do.

Right now.

Not “tomorrow”, not “when you get around to it”.

Now.

Pull up your bank statement, your Paypal account and your credit card statements.

Is there anything in there that’s happening every month that you forgot about, don’t need, or don’t even want?

Ax that crap. Kill it with fire. Nuke it from orbit. Stop wasting your money.

I’d be willing to bet 99% of everyone has something they are paying for every month that they don’t even want, but either forgot was happening or have just let inertia keep paying the bills.

Be the 1%.