This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

The no-pants guide to spending, saving, and thriving in the real world.

This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

We had a garage sale last week, as a wrap-up to the April 30 Day Project. We got rained out halfway through the first day of our 3-day sale, but we still managed to clear $1500. We held the sale in our neighbor’s garage because it had more space and better visibility.

Wednesday night, while carrying boxes over, I missed the step to their property from our driveway and crashed while carrying three boxes. That’s a twisted ankle and a bleeding knee. Naturally, while I’m hopping and swearing, everyone is concerned that I’m okay. The worry-warts. Anyway, it hurt, so we stopped setting up while we still had a few boxes left in the basement.

[ad name=”inlineleft”]Thursday morning, I decided to show them all. At 5:30AM, before anybody else is strongly considering the possibility of maybe thinking about getting ready to hit the snooze button, I decided to get the rest of the boxes ready. They’d all wake up, worried about how I’m feeling, asking if I’m to stiff to carry boxes. The best way to show them they don’t need to worry would be to have all of the boxes dealt with before they woke up. So I started. Up and down the stairs, with a stiff, twisted ankle, gloating to myself about how tough I was…BOOM, down the stairs. I was on my back, sliding down the stairs. I caught a stair-tread in the small of my back and another on the point of my tailbone. Mommy?

After I stopped twitching on the floor at the base of the stairs, I managed to get the last of the boxes ready. Instead of sympathy, I spent the rest of the weekend getting asked if I needed an inflatable doughnut to sit on. There are places I’d prefer not to have bruised.

Unpacking the boxes made me glad that everything was priced. We spent 6 weeks going through our entire house–every room, every dresser, every drawer–to eliminate the clutter. As something went into a box, it got priced, so we didn’t have to do it all at the last minute. That is the most important time-saving step for a garage sale. Price it as you pack it. You don’t want to waste hours pricing stuff while tripping over potential customers.

Another preparation tip to do early: Find tables! Ask around. You’d be surprised at who has a dozen folding tables collecting dust in his basement. It’s better to borrow that to rent. The best price I found was $17.50 to rent an 8′ X 30″ table for a week. We didn’t have to do that, but we thought we would have to. I borrowed a few, found a few, and built a few out of sawhorses.

The week before the sale, we placed an ad in the paper. When I placed the ad, the paper called to suggest we change it from running the weekend before to running just the days of the sale. I agreed, to a point, but their Sunday circulation is miles ahead of the weekday circulation, so why pay to run an ad nobody will see on Thursday? I ran it Sunday through Tuesday, because I wanted the Sunday ad and we got 3 consecutive days in the price. Did I actually know better than the paper’s sales-weasel? Who knows? I think I made the right decision.

The Sunday before the sale, I posted an ad on Craigslist. Interesting fact: little old ladies use Craiglist to plan their garage-sale adventures.

Two days before the sale, we made signs. Bright pink signs with brighter yellow starbursts. They were all simple. “Mega Sale! 8-5” followed by an arrow and our address. Simple, easy-to-read, and bright. The morning of the sale, after the ibuprofen kicked in, I put the signs up. When you make signs out of paper, always include a crossbar. It rained a lot the first day of the sale, so the signs wilted. The second morning, I went out with some duct tape and crossbars and fixed them all.

The day before the sale, we got cash and change. We had $50 in 1s and 5s and $25 in silver change. No pennies. Nothing was priced to make us need them.

The morning of the sale, we set up two canopy tents in the driveway and pulled the prepared-and-filled table out under them. We finished stacking as much as we could on the tables and called it “open”. There were a few boxes we couldn’t put out due to the rain. We simply ran our of room. At noon, $65 into the sale, we decided enough was enough and shut down–cold, wet, and miserable. Lunch and a nap made the day better.

Later, I’ll discuss the other parts of our successful sale.

Note: The entire series is contained in the Garage Sale Manual on the sidebar.

Update: This post has been included in the Money Hacks Carnival.

I just realized that I screwed up on Friday’s post and accidentally scheduled it for July 31 instead of July 1. Sorry about that.

I am pretty excited about tomorrow’s post. I’m going to…well, that should wait for tomorrow. It’ll be fun, though.

It’s a basic economic principle: If you want to sell less of something, charge more for it. That works for labor costs, too. Raising the minimum wage, especially when there is a recession, will only cause less employment.

This is a neat business idea. Sometimes, a small business wants a mailing address that isn’t the owner’s home address.

Foreign CDs seem tempting. You can make a decent return in India. Just make sure it’s a legit bank, instead of the “Cayman Island” banks that exist just to collect wire transfers from the US.

In a high-tax, high-regulation environment, the underground economy will thrive, every time. Working for cash and no paperwork can be tempting.

Here’s a sample email to help you buy a car.

Shattering Taboos was included in the Carnival of Personal Finance.

Thank you! If I missed anyone, please let me know. I’ve been slacking off on carnival submissions lately.

There are so many ways you can read and interact with this site.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!

I know I haven’t been doing the Sunday roundups very regularly. Do you miss them? Would you like to see something else here? When I do post them, I use it as a place to post some updates about my life that aren’t necessarily finance-related, and I post some links worth visiting.

Please let me know, I love feedback.

In the meantime….

Vacation, Shmaycation, Staycation? was included in the Canadian Finance Carnival.

The Unfrugal Meal was included in the Yakezie Carnival and the Totally Money Carnival.

Annoying Your Wife: 5 Ways to Succeed was included in the Carnival of Financial Planning.

Money Problems, Day 11 was included in the Best of Money Carnival.

Is that the best you can do? was included in the Totally Money Carnival, by a different host.

Thank you! If I missed anyone, please let me know.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!

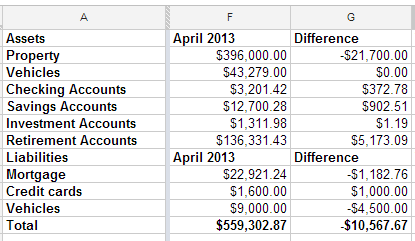

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.

When I found myself doing an abrupt unemployment tour this month, the first thing I did was dig into my budget. I did it so I could see how long it would be before our finances got scary and to see what could be eliminated.

Gah! So much could be eliminated.

There were things that I’d set up on automatic payments, added to my budget, then ignored.

There were things that I’d signed up for and used, but didn’t get as much enjoyment out of any more.

Example Number 1: Netflix

We love Netflix. It gets used every single day. But the DVDs often sit on the kitchen counter for a month before we get around to watching them. We clearly don’t need the DVD plan any more.

Example Number 2: Software Subscription

I use some software to track the Google rank of several of my websites. There is an addon that makes the software work much better. The addon costs $20 per quarter. The problem is that I’m not looking at the rankings of these sites any more. Some of the sites have been shut down, or I’m no longer involved with the clients. That makes the paid addon a total waste. I canceled it and told the tracking software to run slower so it would give Google a fit.

Example Number 3: Extra Domains

Hello, my name is Jason and I’m a domain addict. Seriously, for a while, I was buying domains every time I had a good idea for a website. Some of them were developed, and some were sketched out and put on hold. I also bought domains to help with the search engine rankings of the developed websites. I topped out at about 120 domains. All of them were on auto-renew. I’ve been letting them expire, but some didn’t have the auto-renew settings changed, so they (surprise!) renewed automatically.

These are just three examples of several years of development, exploration, and automation of my complicated financial life, and they add up to more than $100 a month essentially wasted.

Here’s what I want you to do.

Right now.

Not “tomorrow”, not “when you get around to it”.

Now.

Pull up your bank statement, your Paypal account and your credit card statements.

Is there anything in there that’s happening every month that you forgot about, don’t need, or don’t even want?

Ax that crap. Kill it with fire. Nuke it from orbit. Stop wasting your money.

I’d be willing to bet 99% of everyone has something they are paying for every month that they don’t even want, but either forgot was happening or have just let inertia keep paying the bills.

Be the 1%.