- I tried to avoid it. I really did, but I’m still getting a much bigger refund than anticipated. #

- Did 100 pushups this morning–in 1 set. New goal: Perfect form by the end of the month. #

- RT @BudgetsAreSexy: Carnival of Personal Finance is live 🙂 DOLLAR DOODLE theme: http://tinyurl.com/ykldt7q (haha…) #

- Hosting my first carnival tomorrow. Up too late tonight. #

- Woot! My boy won his wreslting match! Proud daddy. #

- The Get Home Card is a prepaid emergency transportation card. http://su.pr/329U6L #

- Real hourly wage calculator. http://su.pr/1jV4W6 #

- Took my envelope budget out in cash, including a stack of $2s. That shouldn’t fluster the bank teller. #

Unlicensed Health “Insurance”

Health insurance is–without a doubt–expensive.

As much as I hate the idea of socialized health care, it does have one shiny selling point to counter its absolute immorality: it’s cheap. Assuming, of course, you ignore the higher taxes and skewed supply/demand balance.

Here in the US, we’re free from that burdensome contrivance. Instead, we have health care and health insurance industries that are heavily regulated and ultimately run by people who have A) never held a job outside of government or academia, and B) have no idea how to run either a hospital or a business. That works so much better. Some days, I think our health system would be better run by giving syringes and band-aids to drunken monkeys. The high-level decision making wouldn’t be worse.

Thanks to that mess and the high unemployment rate that somehow hasn’t been remedied by the 27 bazillion imaginary jobs that have been save or created in the last 2 years, some people are hurting. Not the poor. We have so many “safety net” programs that the poor are covered. I’m talking about the “too rich to be considered poor, but too poor to be comfortable”, the middle class.

If are much above the poverty line, you will stop qualifying for some of the affordable programs. The higher above the line you go, the less you qualify for. That makes sense, but the fact that we have so many safety net programs means there is a lot of demand created by all of the people who are getting their health care “free”.

That drives the prices up for the people who actually have to pay for their own care. Yes, even if you have an employer-sponsored plan, you are paying for the health insurance. That insurance is a benefit that is a part of your total compensation. If employers weren’t paying that, they could afford higher wages.

As the price goes up, employers are moving to a high-deductible plans, which puts a squeeze on the employees’ budgets. Employees–you and I, the people who actually have to pay these bills–are looking for ways to save money on the care, so they can actually afford to see a doctor.

In response to that squeeze, some unscrupulous people(#$%#@%! scammers) are capitalizing on the financial pain and selling “health discount plans” which promise extensive discounts for a cheap membership fee. These plans are not insurance. In a best-case scenario, the discount plans will get you a small discount from a tiny network of doctors and clinics. Prescription drug plans are no better. You may get a 60% discount, but only if you use a back-alley pharmacy in Nome, Alaska between the hours of 8 AM and 8:15 AM on January 32nd of odd leap years.

How can you tell it’s a scam?

The scammers will try to sell you on false scarcity. They’ll say the plan is filling up fast and you have to buy now if you want to get in on it. For all major purchases, if you aren’t going to be allowed time to research your options, assume it’s a scam. Good deals won’t evaporate.

They aren’t licensed. Call the Department of Commerce for your state and see if the company is a licensed insurance provider. Pro tip: they aren’t.

They don’t want you to read the plan until after you’ve paid. That’s a flashing, screaming, electro-shock warning sign for anything. Once you’ve given them your money, your options are reduced.

The price is amazingly low. Of course it is. They aren’t actually providing any services, so their overhead is nonexistent. They only have to pay for gas to get to the bank to cash your checks.

Really, the best way to judge if something is a scam is to go with your gut. Does it feel like a scam? Do you feel like you’re getting away with something? Does it sound too good to be true?

To recap: health care/prescription discount plans = bad juju.

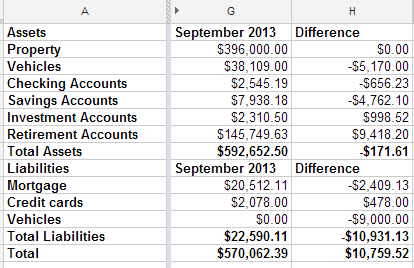

Net Worth Update

Time to update my net worth. Here are the highlights:

We paid off the Tahoe we bought last fall, but the value of my Pacifica fell $5,000 since April. That made me sad.

In August, we had $1000 worth of car repairs and $5500 for braces. We had most of the money saved for braces, but had to juggle some savings accounts around to cover it. We didn’t have enough money in our car repair fund to cover the repairs. Between the two, we beat up our credit card a bit more than usual last month. I’m not happy about it, but I’m confident we’ll catch up this month. My current goal is to get that paid off by the end of September. If I do, I should be able to avoid paying any interest on the balance.

All in all, it’s not bad progress. Our assets dropped $171.61, but our liabilities dropped $10,931.13, so our net worth is up $10,000. You won’t catch me complaining about that.

What’s going to happen in the future? We’re going to remodel both of our bathrooms this winter. We’re hoping to buy a pony before spring.

I’m excited to see our budget evolve over the next few months.

My wife is working and my kids are all in school. With the way our schedules work, we’ve pulled the youngest two out of daycare, so that expense is gone. And there are a couple of other things in the works that I’ll be sharing when they are finalized. If things progress the way they are looking, we’re going to spend the winter living off of my income, and saving her’s. That makes me feel like putting on an ant costume and kicking grasshopper’s butt all over town.

Investments are a Gamble

- Image via Wikipedia

Or a scam.

If you’ve been reading Live Real, Now for long, you’ll know I hate scammers. I particularly loathe scammers who prey on the hopes of the naive. There is a special corner of hell reserved for those who live to steal the futures of the innocent.

For many people, especially day-traders, it is absolutely true that stocks are the same as gambling. For too many other people, investments are an opening for con-men to ply their trade.

People invest their money to secure their futures. They put their life saving into some investment vehicle and, hopefully, it grows to bring financial security. Properly done, it’s not a gamble.

In the worst case, you get investment advice from a slimy, scum-sucking 3-card-monte dealer. These blood-suckers–at best–don’t care about your future. They only care about their commissions. Others will do anything possible to run away with your nest egg.

So how do you avoid the karmicly-destined-to-be-cockroach fraudsters?

First, never invest more then you can afford to lose. Gambling rules apply. If you can’t afford to lose it, you need to keep your money someplace absolutely secure. Your mattress, buried mayonnaise jars, or a simple savings account come to mind.

Do your research. Is the person selling the investment licensed to do so? What is the historic return? Can you independently verify that? If you run across anything that looks too good to be true, it probably is. Run away.

Don’t fall for a time crunch. If something is a good investment today, it will still be a good investment tomorrow. Take you time, do the research, get the details in writing, and get a second opinion. If you are supposed to keep the investment a secret, it’s either a scam or a crime. Always cover your own butt.

Be safe. Keep your money.

For more information, see the SEC, the FTC, the CFTC and FINRA.

Can I Sell My Lottery Payments for a Lump Sum?

This is a guest post.

Winning the lottery is everyone’s dream. You hit the lotto, cash in your ticket and kiss all your troubles goodbye, right? Actually, that might not be true. Just look at the number of lottery winners who’ve ended up worse off than they were before they hit it big. There are several problems here. One problem is that people often spend their money unwisely, without learning how to manage it properly. Lottery annuity payments were designed to help with this. However, those annuity payments might not actually be enough to make a significant difference in your life. If that’s the case, you might be wondering if you can sell your payments for a lump sum. The answer is, yes, you can. But there’s a catch. Actually, there are a couple of catches.

Buyers Matter

First, let’s talk about buyers. They’re the ones who’ll be paying you a lump sum for your lottery payments. Now, you can’t expect a buyer to offer the full amount you’re owed from the lottery, but you should be able to expect a significant percentage of the winnings. That’s not the case with many buyers. They recognize your desperation and have no qualms about taking advantage of your situation. That’s not true for all buyers, though. You need to recognize qualified buyers from those better left alone. Obviously, that’s tough to do on your own. Most people have never been in the position of having to sell lottery payments before, and it’s easy to get lost in a world with which you’re not familiar.

Sell Only Part of It

Another important consideration is whether you need to sell all of your lottery winnings or only a percentage of them. You can easily sell just a specific portion of your winnings, enough to cover your immediate needs, and retain the remainder as regular ongoing payments. This ensures that you have the money you need right now, as well as a financial cushion for the future.

Work with a Go-Between

The ideal solution to your quandary is to work with a firm that acts as a go-between. The company will vet and investigate buyers, ensuring that you only have the cream of the crop to choose from. Not only that, but working with a reputable firm will also ensure that you get the highest percentage possible of your winnings, rather than leaving you with a mere pittance.

Of course, not all such firms are the same, and you need to recognize a reputable company. Look for a firm that’s been in business for a number of years – one with an established reputation and a list of satisfied clients. Second, make sure the company doesn’t work for the buyers – the firm should work for you, the seller. This ensures there’s no conflict of interest. A company that works on behalf of the buyer has no incentive to go above and beyond to ensure you get a fair deal. One that works for you certainly does.

What to Take Away From John Cleese’s Divorce

If you haven’t been kept under a rock your whole life, you’re likely familiar with actor and comedian John Cleese. Part of the infamous Monty Python crew, he starred in films such as Monty Python’s Quest for the Holy Grail, and television shows such as Faulty Towers. However, are you familiar with what has happened to Mr. Cleese financially over the past few years?

When Cleese divorced his third wife she ended up with a divorce settlement that quite literally made her richer than him, despite the fact that they were married for only 16 years and had produced no children.

Divorce is, unfortunately, a fixture of modern society, and people of both sexes need to know how they can protect their personal finances in case of a divorce. After all, these days more than 50% of marriages end in divorce, so not preparing yourself financially for it is engaging is some rather wishful thinking. So how best to protect yourself and your personal finances, should you be unfortunate enough to have to go through one?

If you are the higher-earning party, get a pre-nup prior to marriage; this simply cannot be overemphasized. Cleese himself, already married to wife number four, incidentally, was told that he should have her sign a prenuptial agreement, he initially didn’t want to, despite having just been taken to the proverbial cleaners. He only reluctantly had one written up when his legal team essentially insisted. Even though prenups can be challenged or modified in court, if you are the party bringing more assets to the relationship, it is irresponsible of you not to solicit a prenuptial agreement from a potential spouse.

Another thing to keep in mind is that you should protect assets you have in joint accounts with your spouse, and also begin to actively monitor your credit, if things become acrimonious between you two. This way, you will prevent them from absconding with the totality of your shared funds, or ruining your credit if they are feeling malicious. If you need further information on how to do this properly, speak with a qualified financial planner.

So if you find yourself considering marriage and either have significant assets to protect or suspect you might have them in the future, you owe it to yourself to look into the legalities surrounding prenuptial agreements, and other thorny issues related to personal finance. Failure to do so can end up seriously impacting your life in a negative way, should you ever be faced with a vindictive or greedy spouse; protect yourself!