- Uop past midnight. 3am feeding. 5am hurts. Back to bed? #

- Stayed up this morning and watched Terminator:Salvation. AWAKs make for bad plot advancement. #

- Last night, Inglorious Basterds was not what I was expecting. #

- @jeffrosecfp It's a fun time, huh. These few months are payment for the fun months coming, when babies become interactive. 🙂 in reply to jeffrosecfp #

- RT @BSimple: RT @bugeyedguide: When we cling to past experiences we keep giving them energy…and we do not have much energy to spare #

- RT @LivingFrugal: Jan 18, Pizza Soup (GOOOOOD Stuff) http://bit.ly/5rOTuc #budget #money #

- Free Turbotax for low income or active-duty military. http://su.pr/29y30d #

- To most ppl,you're just somebody [from casting] to play the bit part of "Other Office Worker" in the movie of their life http://su.pr/1DYMQZ #

- RT @MoneyCrashers: Money Crashers 2010 New Year Giveaway Bash – $8,300 in Cash and Amazing Prizes http://bt.io/DQHw #

- RT: @flexo: RT @wisebread: Tylenol, Motrin, Rolaids, and Benadryl RECALLED! Check your cabinets: http://bit.ly/4BVJfJ #

- New goal for Feb. 100 pushups in 1 set. Anyone care to join me? #

- RT @BSimple: Your future is created by what you do today, not tomorrow"— Robert Kiyosaki So take action now. #

- RT @hughdeburgh: "Everything you live through helps to make you the person you are now." ~ Sophia Loren #

- Chances of finding winter boots at a thrift store in January? Why do they wear our at the worst time? #

- @LenPenzo Anyone who make something completely idiot proof underestimates the ingenuity of complete idiots. in reply to LenPenzo #

- RT @zappos: "Lots of people want to ride w/ you in the limo, but what you want is someone who will take the bus w/ you…" -Oprah Winfrey #

- RT @chrisguillebeau: "The cobra will bite you whether you call it cobra or Mr. Cobra" -Indian Proverb (via @boxofcrayons) #

- RT @SuburbanDollar: I keep track of all my blogging income and expenses using http://outright.com it is free&helps with taxes #savvyblogging #

- Reading: Your Most Frequently Asked Running Questions – Answered http://bit.ly/8panmw via @zen_habits #

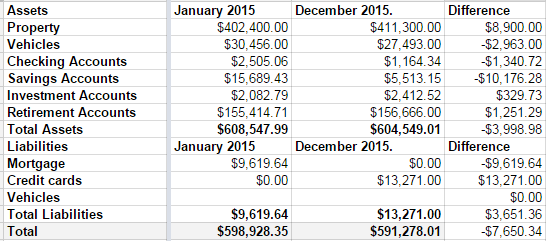

Net Worth and other stuff

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

- We’re going to save for college at a rate we should have started 10 years ago.

- We’re going to max out both of our retirement plans.

- We’re going to take some nicer family vacations.

- We’re going to buy a pony.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

Sunday Roundup – Life’s Been Busy

I’ve been skipping the Sunday roundups for the last month. Over the last 4 weekends, I have put 2000 miles on my car, taking 4 trips–only one of which I consider optional and that was the only fun trip. With the extra gas, and having to pay for my son’s vision therapy, we went over budget by more than $4,000.

Ouch.

It’s the first debt I’ve picked up in more than 2 years. It’s leaving me twitchy and crabby. I don’t like it much at all.

And, with all of the traveling, I have let the Sunday posts slip.

Weight Loss Update

I am on the Slow Carb Diet. At the end of the month, I’ll see what the results were and decide if it’s worth continuing. For those who don’t know, the Slow Carb Diet involves cutting out potatoes, rice, flour, sugar, and dairy in all their forms. My meals consist of 40% proteins, 30% vegetables, and 30% legumes(beans or lentils). There is no calorie counting, just some specific rules, accompanied by a timed supplement regimen and some timed exercises to manipulate my metabolism. The supplements are NOT effedrin-based diet pills, or, in fact, uppers of any kind. There is also a weekly cheat day, to cut the impulse to cheat and to avoid letting my body go into famine mode.

I’m measuring two metrics, my weight and the total inches of my waist , hips, biceps, and thighs. Between the two, I should have an accurate assessment of my progress.

Weight: I have lost 45 pounds since January 2nd. I haven’t weighed in since my last Sunday update. For the last week, I haven’t been terribly strict about being on the diet and I haven’t stressed about staying on it while traveling.

Total Inches: I have lost 27 inches in the same time frame.

Best Posts

Every home needs a secret tunnel. Every time a house in my neighborhood goes up for sale, I try to convince my wife we should buy it and connect it to ours with tunnels.

Some day, when I’m a brazillionaire, if I hate my descendants, I’m going to set up my will to frustrate them all.

Haggling is a skill I need to work on.

The Monster Hunter Alpha early advanced reader copy is available. The Monster Hunter books are fun, fast reads.

Bacon art makes me cultured and hungry.

Making strangers smile is a way to make your day memorable.

I always get a warm fuzzy feeling when I hear about people successfully chasing their dreams.

I need to find a use for some of the unique materials here.

Carnivals I’ve Rocked and Guest Posts I’ve Rolled

Karate Guess So was the winner of last week’s Best of Money Carnival! Woo!

Debt Options was included in the Festival of Frugality.

Budgeting Sucks was included in the Carnival of Personal Finance.

The Benefits of Ignorance was included in the Totally Money Blog Carnival.

New Debt was included in the Yakezie Carnival.

Thank you! If I missed anyone, please let me know.

Get More Out of Live Real, Now

There are so many ways you can read and interact with this site.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!

My Financial Plan – How I Improve on Ramsey

In April, my wife and I decided that debt was done. We have hopefully closed that chapter in our lives. I borrowed, then purchased, The Total Money Makeover by Dave Ramsey.  budget” width=”300″ height=”213″ />We are almost following his baby steps. Our credit has always been spectacular, but we used it a lot. Our financial plan is Dave Ramsey’s The Total Money Makeover, with some adjustments.

budget” width=”300″ height=”213″ />We are almost following his baby steps. Our credit has always been spectacular, but we used it a lot. Our financial plan is Dave Ramsey’s The Total Money Makeover, with some adjustments.

Step 1. Budget:

The budget was painful, and for the first couple of months, impossible. We had no idea what bills were coming due. There were quarterly payments for the garbage bill and annual payments for the auto club. It was all a surprise. Surprises are setbacks in a budget.

When something came up, we’d start budgeting for it, but stuff kept coming up. We’re not on top of all of it, yet, but we are so much closer. We’ve got a virtual envelope system for groceries, auto maintenance, baby needs(we have two in diapers) and some discretionary money. We set aside money for everything that isn’t a monthly expense, and have a line item for everything that is. My wife is eligible for overtime and monthly bonuses. That money does not get budgeted. It’s all extra and goes straight on to debt, or to play catch-up with the bills we had previously missed. I figure it will take a full year to get all of the non-monthly expenses in the budget and caught up.

Step 2. The initial emergency fund:

Ramsey recommends $1000, adjusted for your situation. I decided $1000 wasn’t enough. That isn’t even a month’s worth of expenses. We settled on $1800, plus $25/month. It’s still not enough, but it’s better. Hopefully, we’ll be able to ignore it long enough that the $25/month accrues to something worthwhile.

Step 3. The Debt Snowball:

This is the controversial bad math. Pay off the lowest balance accounts first, then take those payments and apply them to the higher balance accounts. Emotionally, it’s been wonderful. We paid off the first credit card in a couple of weeks, followed 6 weeks later by my student loan. Since April, we’ve dropped nearly $10,000 and we haven’t made huge cuts to our standard of living. At least monthly, we re-examine our expenses to see what else can be cut.

Step 4. Three to six months of expenses in savings:

We aren’t on this step yet. In step 2, we are consistently depositing more, making us more secure every month.

Step 5. Invest 15% of household income into Roth IRAs and pre-tax retirement:

I have not stopped my auto-deposited contribution. It’s stupid to pass up an employer match. My wife’s company does not match, so she is currently not contributing.

Step 6. College funding for children:

We have started a $10 College fund.

Step 7. Pay off home early:

I don’t see the point in handling this one separately. Our mortgage is debt, and when the other debts are paid, we will be less than a year from owning our house, free and clear. This is rolled in with step three. All debt is going away, immediately.

Step 8. Build wealth and give!

We have cut off most of our charitable giving. Every other year, it has been a significant percent of our income, and in a few more years, will be so again. The only exception to this is children knocking on the door for fundraisers. I have no problems with saying no to a parent fundraising for their kid, but when the kids is doing the work, door-to-door, especially in the winter, I buy something. My son’s school, on the other hand, gets fundraisers ignored. When they come home, I send a check to the school, ignoring the program. I bypass the overhead and make a direct donation.

2010 Budget Changes

We’re making some changes to how we manage our finances this year. Our destination isn’t changing, but the trip is.

- All of the cards are going away. Not necessarily destroyed, but certainly inconvenient. There’s a $7000 overdraft protection account attached to our debit cards. There’s no need for an “emergency” card. If it’s truly an emergency, we are covered. We are going to destroy some and ice the rest.

- We’re going to go “cash only”. We’ve going to the envelope system. There will be an envelope for grocery money, gas money, discretionary money, and baby crap. If there isn’t enough money in an envelope, it will have to come out of another envelope. If we don’t have enough money, we’ll have to do without, instead of spending imaginary money at 10% interest. Gas will be the exception, so we don’t have to bundle the kids up to pay for gas. No money, no spendy. We tried a “virtual envelope”, with every purchase tracked by category in a spreadsheet, but it didn’t work. Real cash, real empty envelopes. Discretionary money covers school activities, miscellaneous household item, and anything else that pops up.

- We’re going to start the “30 day list”. If we want something, we’ll put it on a list. If we still want it 30 days later, it will be okay, provided there’s money for it. This is part of what the discretionary budget is for.

- My wife is getting $50/month “blow money”. Absolutely unaccountable. If she doesn’t have this vent, the whole system will fall apart.

This is all stuff my wife and I have talked about and agreed to, but now, it’s organized and laid out. We HAVE to do it or something similar. We are both on board with this plan. We should see our debt management plan skyrocket, without feeling like we are missing out on life.

Sunday Roundup

I know I haven’t been doing the Sunday roundups very regularly. Do you miss them? Would you like to see something else here? When I do post them, I use it as a place to post some updates about my life that aren’t necessarily finance-related, and I post some links worth visiting.

Please let me know, I love feedback.

In the meantime….

Here are some great Yakezie sites to check out.

Carnivals I’ve Rocked

Vacation, Shmaycation, Staycation? was included in the Canadian Finance Carnival.

The Unfrugal Meal was included in the Yakezie Carnival and the Totally Money Carnival.

Annoying Your Wife: 5 Ways to Succeed was included in the Carnival of Financial Planning.

Money Problems, Day 11 was included in the Best of Money Carnival.

Is that the best you can do? was included in the Totally Money Carnival, by a different host.

Thank you! If I missed anyone, please let me know.

Get More Out of Live Real, Now

There are so many ways you can read and interact with this site.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!