Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

The no-pants guide to spending, saving, and thriving in the real world.

Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

I’m overbanked.

The National Bank, Oamaru, built 1871: a prostyle Palladian portico on a neoclassical facade (Photo credit: Wikipedia)I’ve mentioned that before.

I won’t give up my herd of CapitalOne 360 accounts. I use those to track my savings goals, all 17 of them. I can’t drop my business accounts, my kids’ savings accounts, or the personal accounts that I actually use to spend money.

I do, however, need to simplify a bit.

Last month, I went through the hassle of transferring my 401k from two jobs ago and my IRA from my last job. Now, I’m down to just two retirement accounts. One is for my current job, and the other is a self-managed IRA with Sharebuilder.

Two down.

A few months ago, I went to yet another bank to close an account. My last job offered crappy health insurance, but balanced it out with an HSA. It complicated things, but the actual costs came to almost the same as the previous plan that didn’t have a high deductible. When I left, my HSA just sat there.

Last year, my oldest got braces, so I cleaned out the HSA ahead of time so we could pay up front and save 5% without paying interest.

Another one down.

That’s three accounts down out of 34.

Thirty-four?

Crap. That’s retirement accounts, business accounts, and personal accounts for two adults and three kids.

Bank 1 has the checking account we use, plus two savings accounts, one of which is where we store the rent money until we take a payday.

Bank 2 has a checking account, 16 savings accounts, and stock-trading account, a CD, and two IRAs for my wife and I.

Bank 3 has a checking account, and savings account for each of two businesses I own, a spare set of personal accounts, a savings account for each of the kids, and a checking account for my teenager.

Bank 4 holds nothing but my current 401k.

The only thing I can simplify without sacrificing my organizational jungle is to combine the personal accounts from bank 1 and 3. The problem is that Bank 1 has all of my bill pay information and there is still an account open for my mother-in-law’s estate. We keep that open just in case we find any other checks we need to cash. Bank 3 has my business accounts tied to my personal account and is the bank that my business partner uses, so that’s convenient to move money around.

I may be stuck.

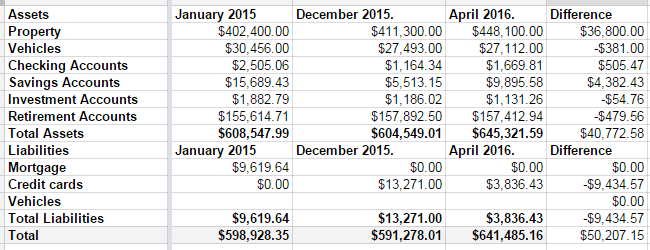

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.

Put one foot in front of the other

And soon you’ll be walking cross the floor

Put one foot in front of the other

And soon you’ll be walking out the door

You never will get where you’re going

If you never get up on your feet

Come on, there’s a good tail wind blowing

A fast walking man is hard to beat

Put one foot in front of the other

And soon you’ll be walking cross the floor

Put one foot in front of the other

And soon you’ll be walking out the door

If you want to change your direction

If your time of life is at hand

Well don’t be the rule be the exception

A good way to start is to stand

Put one foot in front of the other

And soon you’ll be walking cross the floor

Put one foot in front of the other

And soon you’ll be walking out the door

If I want to change the reflection

I see in the mirror each morn

You mean that it’s just my election

To vote for a chance to be reborn

Last week, the washing machine in our rental house died. It was older than I am, so this wasn’t really a surprise. It was one of just two appliances we didn’t replace before we moved the renters in.

My wife–bargain shopper that she is–found a replacement on Craigslist. We got it in, then left the dead washing machine next to the replacement, as a warning to any other appliance that thinks it can shirk its assigned work.

This morning, we went over to pull the corpse of our washing machine out of the basement.

Now, I am an out-of-shape desk jockey, my wife is considerably weaker than I am, and a 40 year old washing machine weighs more than 200 pounds.

In the basement.

I’m Superman. Although at one point, I did trade 10 years of the useful life of my right knee in exchange for not letting that thing tumble down the stairs on top of me.

What do you do with a dead washing machine?We could have the garbage company pick it up for $25. Or we could leave it on the curb and wait for some stinking scrapper to take it.

Or…we could join the dark side and scrap it ourselves.

For the uninitiated, scrappers are the people who drive around looking for fence-posts to steal out of other people’s yards, or cut the catalytic converters out of cars parked at park-and-ride bus stops, or steal all of the copper pipes out of your house while your on vacation. Sometimes, they get scrap metal from legitimate sources, I’ve heard.

We decided to go the legitimate route and take the washing machine to the scrap metal dealer in the next town over.

It was pretty easy. We pulled in with the washer in the trailer. A guy on a forklift pulled up and took it, then handed us a receipt to bring to the cashier. She paid us in cash, and we were on our way.

$7.50 richer.

200 pounds of steel, and we made less than $10.

There are people who pay their bills by recycling scrap metal, but I have no idea how. Driving around looking for things to scrap would seem to burn more gas than you’d make turning it in.

Some people scour Craigslist looking for metal things in the free section.

Some people have an arrangement with mechanics to remove their garbage car parts.

Some people are only looking to supplement their government handout checks enough to pay for cigarettes.

Us? We’re going to leave scrapping to the scavengers.

Many people are looking at the housing market slump right now as an investment opportunity. Here are a few of the things that you need to know before getting a new home loan or refinancing your existing loan in order to make that happen.

Amount You Want to Borrow

A lot of borrowers go shopping for real estate and have exactly no idea how much money they can borrow. One of the first questions that you need to ask before going real estate hunting is how much can I borrow. You can ask a bank, lender, or financial institution to give you a ballpark figure of the amount of loan that you would qualify for. This will make it easier for you to narrow down exactly what type of property you can afford and what areas you can concentrate on.

Amount of Interest You Will Pay

Too many people are overly concerned with the purchase price of the home that they are buying. They fail to find out how much interest they will have to pay back to the bank in order to make their home ownership dreams come true. This is where a home loan calculator can be really useful. You can find out exactly how much interest you will repay over a 10, 20, or 30 year loan time period. You can also change the interest rate and down payment amount on those calculators to see if you can secure a lower monthly payment.

Credit Score Needed to Qualify

It doesn’t matter if you are buying a home for the first time or refinancing an existing loan. Your credit score matters. You need to start doing some research now if you want to secure a loan with a really low interest rate. This involves taking the time to see what credit scores traditional lenders are looking for and doing the work necessary to qualify for this loan. Your credit score will make a big difference in determining if an investment property purchase is a profitable endeavor or one that winds up costing you money. It will depend heavily on what kind of loan your credit score allowed you to negotiate.

Make the Choice

Once you know how much you will need and exactly how much you will be paying out over the life of another mortgage, you can decide whether you want to refinance your current home loan to get another one. Adding on another huge debt to an existing one is a big risk. Make sure to think it through fully before jumping in.