Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

The no-pants guide to spending, saving, and thriving in the real world.

Am I the only one who just noticed that it’s Wednesday? The holiday week with the free day is completely screwing me up.

Just to make this a relevant post:

Spend less!

Save more!

Invest!

Wee!

Grr!

Monday, I brought Punk #1 to the orthodontist. He’s got an underbite and some crooked teeth, but I didn’t realize how off it was until I saw the pictures they took. Some of the closeups could be inspiration for a Halloween mask.

It look like he started with a small underbite that made his teeth line up wrong, which–as they grew–accentuate the wrong. Now, it’s very, very wrong.

Next week he goes in to get his top teeth done.

At a cost of $5800.

If we pay up-front, they’ll knock 5% off, bringing it down to $5500. That covers everything, all of the follow-ups, broken hardware, every stage the whole way through. If we pay monthly, it will be $1450 down and $200 per month (interest free) for almost 2 years.

Almost six grand.

Fortunately, we knew this was coming, so we’ve been saving for this for a few years.

Unfortunately, we’ve only been saving $50-100 a month. We can’t wait much longer. With an underbite, you have more options if you do the work before the kid is done growing. I’d really like to avoid jaw surgery for him, so we have to make things happen.

Our braces account has $3100 in it. My HSA account has $875. That’s from my last job, so that’s as big as it gets. That leaves us almost exactly $1500 short.

I hate the idea of touching our emergency fund, although it does have enough money in it.

We’ve also got some money tucked away in an account leftover from my mother-in-law dying last year. I think that’s where we’re going to come up with the difference.

How else could we save money?

We could shop around, but this isn’t something I want to give to the lowest bidder. I want to do it right, and I know several people who have had braces put on by this office, either by this orthodontist or her father.

I asked about a cash discount and got turned down.

That’s it. Next week, I burn $5500. Hope the kid eventually appreciates it.

I’m overbanked.

The National Bank, Oamaru, built 1871: a prostyle Palladian portico on a neoclassical facade (Photo credit: Wikipedia)I’ve mentioned that before.

I won’t give up my herd of CapitalOne 360 accounts. I use those to track my savings goals, all 17 of them. I can’t drop my business accounts, my kids’ savings accounts, or the personal accounts that I actually use to spend money.

I do, however, need to simplify a bit.

Last month, I went through the hassle of transferring my 401k from two jobs ago and my IRA from my last job. Now, I’m down to just two retirement accounts. One is for my current job, and the other is a self-managed IRA with Sharebuilder.

Two down.

A few months ago, I went to yet another bank to close an account. My last job offered crappy health insurance, but balanced it out with an HSA. It complicated things, but the actual costs came to almost the same as the previous plan that didn’t have a high deductible. When I left, my HSA just sat there.

Last year, my oldest got braces, so I cleaned out the HSA ahead of time so we could pay up front and save 5% without paying interest.

Another one down.

That’s three accounts down out of 34.

Thirty-four?

Crap. That’s retirement accounts, business accounts, and personal accounts for two adults and three kids.

Bank 1 has the checking account we use, plus two savings accounts, one of which is where we store the rent money until we take a payday.

Bank 2 has a checking account, 16 savings accounts, and stock-trading account, a CD, and two IRAs for my wife and I.

Bank 3 has a checking account, and savings account for each of two businesses I own, a spare set of personal accounts, a savings account for each of the kids, and a checking account for my teenager.

Bank 4 holds nothing but my current 401k.

The only thing I can simplify without sacrificing my organizational jungle is to combine the personal accounts from bank 1 and 3. The problem is that Bank 1 has all of my bill pay information and there is still an account open for my mother-in-law’s estate. We keep that open just in case we find any other checks we need to cash. Bank 3 has my business accounts tied to my personal account and is the bank that my business partner uses, so that’s convenient to move money around.

I may be stuck.

I have a confession, but it’s probably not going to be a big shocker if you read the title of this post.

I hide money from my wife.

Some of you just started screaming at your monitor that I’m a horrible person.

That’s cool.

You’re wrong, but the fact that I got that reaction out of you makes me smile.

Ok, I might be a little bit horrible, but not because I hide money.

My wife has an admitted shopping problem. If she thinks we’re broke, she shops less. That’s a win and allows me to save up for our long-term goals and provide for our financial security.

I don’t lie about it. If she asks how we’re doing, I tell her. At least in general terms.

But I didn’t tell her about my annual bonus, until we had a bunch of car repairs come up that would have swamped our emergency fund.

I also haven’t told her about the cash I’ve been stockpiling.

A couple of years ago, the power went out here for four days. It wasn’t just our house, it was 75% of everything within 5 miles of our house.

When the power came on in some places after a day or two, the phone lines were still down, which meant gas stations couldn’t process credit cards.

Quick, look in your wallet and tell me how much cash you have on you….

Most people live on their credit or debit cards.

Could you buy food or water if your plastic was gone?

I could that week, but not for long, so I started taking the cash payments from my side hustle and putting it aside. I’d come home, give my wife a little cash, keep a little cash for myself, and put at least 80% of it away. I absolutely refuse to touch that money for anything.

Part of the “set it aside and forget about” means not revealing its existence. It would be too easy to dip into it to pay the pizza guy or when we go to Rennfest.

So I don’t talk about, and it gets to sit all by itself in the safe, comfy and warm. It’s my security blanket, and nobody gets to touch my binky.

Recently Russian spy Anna Chapman tweeted a proposal to fellow spy Edward Snowden, as in a marriage proposal. News reports covering the Internet event report that Chapman would not reveal whether she was serious but asked reporters to use their imaginations. So it is yet to be seen whether there will be spy marriage ahead for the two notorious leakers. What is true, however, is that no nuptials can take place at the moment, even if Anna Chapman were serious and Edward Snowden. That is because the United States has revoked Snowden’s U.S. passport, and marriage ceremonies cannot take place in the airport where Snowden is trying to buy time. So how can Chapman and Snowden afford a long-distance relationship? Follow this quick guide of tips for helping the spies survive what could be a long road ahead!

Anna Chapman has the most mobility right now, so she should be looking out for cheap flights to where Snowden is hiding out. A long-distance relationship can be expensive, so that is why finding deals on air travel is key. She can drop into the airport for a quick rendevouz. Why not?

These two potential spy lovers and super team need to save their money at every turn. Hiding out in secrete is costly, so they should create a special account that they both can add to for getaway and meeting expenses. Meeting at the airport is going to get old after a while, so they need to find a safe space where they can enjoy one another and sustain their relationship. Long-distance relationships are known for their difficulty because a couple spend so much time trying to reconnect every time they see one another.

Long-distance relationships have little room for petty fighting. You see each other so infrequently that you have to cherish the time you have together. Instead of talking spy business, Anna Chapman and Edward Snowden should make sure they are focusing on each other by getting to know each other and focusing on the small things that make them happy together. Petty fighting will destroy a long-distance relationship. Chapman and Snowden should part each meeting feeling good about the other instead of feeling frustrated.

The key to long-distance relationships is always to kiss and makeup before leaving. No matter what the spies face together or apart, they cannot let their professions and media scrutiny come between them. Instead, they need to focus on their love and passion. Make sure to share a passionate kiss before leaving each meeting so that the memory of love and admiration is fresh on the mind. With a little effort in the romance department, Chapman and Snowden will be well on their way to creating harmony in their relationship. Moving from shallow levels to more deeper levels, however, is going to take time.

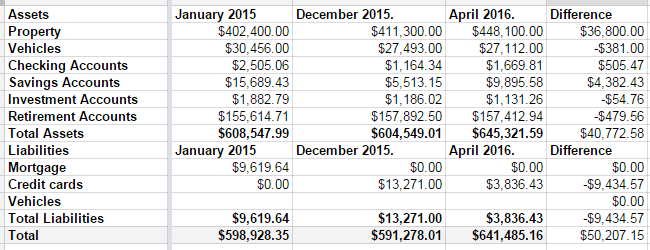

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.