- RT @MoneyMatters: Frugal teen buys house with 4-H winnings http://bit.ly/amVvkV #

- RT @MoneyNing: What You Need to Know About CSAs Before Joining: Getting the freshest produce available … http://bit.ly/dezbxu #

- RT @freefrombroke: Latest Money Hackers Carnival! http://bit.ly/davj5w #

- Geez. Kid just screamed like she'd been burned. She saw a woodtick. #

- "I can't sit on the couch. Ticks will come!" #

- RT @chrisguillebeau: U.S. Constitution: 4,543 words. Facebook's privacy policy: 5,830: http://nyti.ms/aphEW9 #

- RT @punchdebt: Why is it “okay” to be broke, but taboo to be rich? http://bit.ly/csJJaR #

- RT @ericabiz: New on erica.biz: How to Reach Executives at Large Corporations: Skip crappy "tech support"…read this: http://www.erica.biz/ #

The Magic Toilet

- Image by tokyofortwo via Flickr

My toilet is saving me $1200.

For a long time, my toilet ran. It was a nearly steady stream of money slipping down the drain. I knew that replacing the flapper was a quick job, but it was easy to ignore. If I wasn’t in the bathroom, I couldn’t hear it. If I was in the bathroom, I was otherwise occupied.

When I finally got sick of it, I started researching how to fix a running toilet because I had never done it before. I found the HydroRight Dual-Flush Converter. It’s the magical push-button, two-stage flusher. Yes, science fiction has taken over my bathroom. Or at least my toilet.

I bought the dual-flush converter, which replaces the flusher and the flapper. It has two buttons, which each use different amounts of water, depending on what you need it to do. I’m sure there’s a poop joke in there somewhere, but I’m pretending to have too much class to make it.

I also bought the matching fill valve. This lets you set how much water is allowed into the tank much better than just putting a brick in the tank. It’s a much faster fill and has a pressure nozzle that lies on the bottom of the tank. Every time you flush, it cleans the inside of the tank. Before I put it in, it had been at least 5 years since I had opened the tank. It was black. Two weeks later, it was white again. I wouldn’t want to eat off of it, or drink the water, but it was a definite improvement.

Installation would have been easier if the calcium buildup hadn’t welded the flush handle to the tank. That’s what reciprocating saws are for, though. That, and scaring my wife with the idea of replacing the toilet. Once the handle was off, it took 15 minutes to install.

“Wow”, you say? “Where’s the $1200”, you say? We’ve had this setup, which cost $35.42, since June 8th, 2010. It’s now September. That’s summer. We’ve watered both the lawn and the garden and our quarterly water bill has gone down $30, almost paying for the poo-gadget already. $30 X 4 = $120 per year, or $1200 over 10 years.

Yes, it will take a decade, but my toilet is saving me $1200.

How to Prioritize Your Spending

Don’t buy that.

At least take a few moments to decide if it’s really worth buying.

Too often, people go on auto-pilot and buy whatever catches their attention for a few moments. The end-caps at the store? Oh, boy, that’s impossible to resist. Everybody needs a 1000 pack of ShamWow’s, right? Who could live without a extra pair of kevlar boxer shorts?

Before you put the new tchotke in your cart, ask yourself some questions to see if it’s worth getting.

1. Is it a need or a want? Is this something you could live without? Some things are necessary. Soap, shampoo, and food are essentials. You have to buy those. Other things, like movies, most of the clothes people buy, or electronic gadgets are almost always optional. If you don’t need it, it may be a good idea to leave it in the store.

2. Does it serve a purpose? I bought a vase once that I thought was pretty and could hold candy or something, but it’s done nothing but collect dust in the meantime. It’s purpose is nothing more than hiding part of a flat surface. Useless.

3. Will you actually use it? A few years ago, my wife an cleaned out her mother’s house. She’s a hoarder. We found at least 50 shopping bags full of clothes with the tags still attached. I know, you’re thinking that you’d never do that, because you’re not a hoarder, but people do it all the time. Have you ever bought a book that you haven’t gotten around to reading, or a movie that went on the shelf, still wrapped in plastic? Do you own a treadmill that’s only being used to hang clothes, or a home liposuction machine that is not being used to make soap?

3. Is it a fad? Beanie babies, iPads, BetaMax, and bike helmets. All garbage that takes the world by storm for a few years then fades, leaving the distributors rich and the customers embarrassed.

4. Is it something you’re considering just to keep up with the Joneses? If you’re only buying it to compete with your neighbors, don’t buy it. You don’t need a Lexus, a Rolex, or that replacement kidney. Just put it back on the shelf and go home with your money. Chances are, your neighbors are only buying stuff so they can compete with you. It’s a vicious cycle. Break it.

5. Do you really, really want it? Sometimes, no matter how worthless something might be, whether it’s a fad, or a dust-collecting knick-knack, or an outfit you’ll never wear, you just want it more than you want your next breath of air. That’s ok. A bit disturbing, but ok. If you are meeting all of your other needs, it’s fine to indulge yourself on occasion.

How do you prioritize spending if you’re thinking about buying something questionable?

Comfort Zone

Even though some people disagree, I am an introvert.

Crowds, strangers, and activities I don’t understand are all things that make me uncomfortable.

A couple of weeks ago, my business partner forwarded an invitation to me. One of our clients invited us to his annual “Giant-Ass Poker Tournament.”

I haven’t played more than a hand or two of poker in more than 20 years. If you do the math, that’s junior high school or earlier. I’ve never played Texas Hold ‘Em at all. Thirty to forty people were expected to be there.

Crowds? Check.

Strangers? Check.

An activity I don’t understand? Check.

I was planning to blow it off. My partner could handle the social niceties, I could stay home and watch Dexter. Win/win.

Saturday, I got a text telling me that our client wants to talk business at the tournament.

Cue four letter words.

I tried to get out of it. I tried to play sick. My partner–also my best friend and designated extrovert–wouldn’t hear of it.

So I walk into this tournament full of people I don’t know. I was late. I thought that would make a good compromise. I’ll deal with the crowd, and ignore the activity I don’t understand.

First words out of the client’s mouth? “Jason! Great to see you, we just started, so let’s buy you in!”

Crap.

I sat out the first game, and talked the business that needed to be talked. Mission accomplished.

Half an hour into it, my friend sends me a text telling me to do a quick wiki search.

Teach myself to play poker using wikipedia while watching a $50 buy-in game played by experienced players? That’s effen nuts.

I knew the hands, I was already familiar with the bet/call/raise process in general. I was really just missing a few details and the mechanics of Hold ‘Em.

What the hell, it’s only $50.

I went out to the living room/bar area and pulled up wikipedia. After reading everything I could, plus a few terms that had never previously registered (A check isn’t what happens when you bet more than you have. Who knew?), I went back to the game and watched with a bit of understanding about what I was seeing.

When the second game started, I bought in and played until almost 2AM. I had a great time and went home $150 richer than I arrived.

Leaving your comfort zone is, by definition, uncomfortable. Sometimes, it’s downright painful. Without it, you can’t grow as a person. Find yourself someone who is willing to obnoxiously drag you into situations that push your limits. It really can be fun.

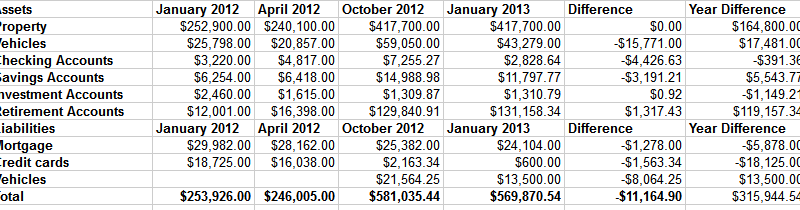

Net Worth Update

Welcome to the New Year. 2013 is the year we all get flying cars, right?

Here is my net worth update, along with the progress we made over the course of 2012.

As you can see, our net worth contracted by about $11,000. Part of that difference is due to selling our spare cars and–against my better judgement–taking payments with a lien on one of them. That is supposed to be paid off within a couple of months. If not, I’ll play repo man again.

The other part of the difference is in the final preparations for our rental property. The only things left to do are sanding and polishing the hardwood floors and cleaning the living room carpet. The final push to get to this point cost some money. All told, we’re nearly $30,000 into getting the house ready to rent. For the naysayers who think we should have sold it, we would have spent more getting it ready to sell.

Other than that, we’re not doing poorly. Our credit card is still being paid off every month and our mortgage is shrinking. If things continue to go well, we’ll have our truck paid off in a couple of months and the mortgage by mid summer.

Beat the Check

- Image via Wikipedia

Have you ever played a game of “Beat the Check”? Your rent is due tomorrow, but you don’t get paid until Friday, so you write the check today an, on payday, you run to the bank to get your paycheck deposited before it has a chance to clear. To stretch out the time, you write yourself a check from another account to cover the deficit, knowing that will take a few more days to clear. This is called “floating” a check.

Sound familiar?

I think most people who write checks have tried to rush a deposit in before a check clears.

In 2004, the Check 21 act went into effect, which turned the game on its head. This law gave check recipients an option to make a digital copy of a check, slashing processing time. Instead of boxes of checks being transported around the country, the check began getting scanned and instantly transferred, along with all of the encoding necessary to keep the digital checks organized. This dramatically cut the amount of time it took to clear a check. What was once a week was reduced to as little as 48 hours.

Now, as technology improves and banks update their infrastructure to match, the “float” time has been reduced even further. Many banks are using image control systems to instantly convert all incoming checks to digital format. Within a couple of hours, these images can be transmitted to the Federal Reserve, to be transmitted nearly instantly to the issuing bank. If both the issuing and the receiving banks are using modern image control systems, it is impossible to float a check. “Beat the Check” is a thing of the past. It’s like betting on purple at the roulette wheel.

Of course, this doesn’t mean that the funds are instantly available. That would eliminate the banks being able make use of the funds during that time. Don’t expect the banks to make a habit of allowing you the use of your money before the federal regulations demand it.