- RT @Dave_Champion Obama asks DOJ to look at whether AZ immigration law is constitutional. Odd that he never did that with #Healthcare #tcot #

- RT @wilw: You know, kids, when I was your age, the internet was 80 columns wide and built entirely out of text. #

- RT @BudgetsAreSexy: RT @FinanciallyPoor "The real measure of your wealth is how much you'd be worth if you lost all your money." ~ Unknown #

- Official review of the double-down: Unimpressive. Not enough bacon and soggy breading on the chicken. #

- @FARNOOSH Try Ubertwitter. I haven't found a reason to complain. in reply to FARNOOSH #

- Personal inbox zero! #

- Work email inbox zero! #

- StepUp3D: Lame dancing flick using VomitCam instead or choreography. #

- I approve of the Nightmare remake. #Krueger #

Consumer Action Handbook

- Image by ivers via Flickr

The Consumer Action Handbook is a book published by the federal government for the express purpose of giving you “the most current information on all your consumer needs.” In short, the Consumer Action Handbook wants to help you with everything that takes your money.

The best part? It’s free.

The book covers topics ranging from banking to health care to cell phones to estate planning. It covers both covering your butt in a transaction and filing a complaint if things go poorly. It explains the options and pitfalls involved in buying, renting, leasing, or fixing a car. You can learn about financial aid for college and maneuvering through an employment agency. And more. So much more.

I’m not sure if you’ve noticed, but I spend quite a bit of time explaining scams and how to avoid them. This book has provided some of the source material for that theme.

It’s 170 pages on not getting screwed, either through fraud or ignorance. Every house should have one. Really, the list of consumer and regulatory agencies alone is worth the price of admission, which–if I wasn’t clear earlier–is $0.

To get yours, go to http://www.consumeraction.gov/caw_orderhandbook.shtml and fill out the form. You can order up to 10 at a time, so pick a few up for your friends and family. They won’t complain, I promise.

Winning the Mortgage Game

There’s a game that’s often mistakenly called “The American Dream”. This game is expensive to play and fraught with risk. It single-handedly ties up more resources for most people than anything else they ever do.

The game is called Home Ownership.

At some point, most people consider buying a house. On the traditional, idealized life-path, this step comes somewhere between marriage and kids. That’s usually the easiest way to organize it. If you have kids first, you’re much less likely to buy a home. This is a game with handicaps.

Once you get to the point where you are emotionally ready to invest in the 30-year commitment that is a house, your first impulse tends to be to rush to the bank to find out how much money you can borrow.

That’s a mistake. If you take as much as the bank will qualify you for, you’re most likely to overextend yourself and end up losing your house. That’s the quick way to lose the home ownership game.

The best thing you could do is figure out how much you can afford before you visit a bank. Conventional wisdom says that your mortgage payment should be no more than 28% of your gross income, but that’s absurd. Who builds their budget on their gross income? I like 28%, but only of your net income. To make the numbers easier to remember, I’d round it to 30%. If you take home $3000 per month, your mortgage payment should be no more than $900 per month.

From there, it pretty easy to figure out how much house you can afford. Using this e mortgage calculator, you’d be able to afford a mortgage of $175,000 if we assume an interest rate of 4.5%. Throughout most of the United States, that will buy you a reasonably sized home, though certainly nothing ostentatious. Clydesdale Bank also has an excellent loan calculator.

Some people like to start out with an interest-only loan. That same emortgage calculator shows that an income of $3000 per month would be able to afford a $240,000 with almost the same payment. That seems like a good plan, but eventually, you’ll have to pay more than just the interest. Taking out a loan that will one day be more than you can afford on the assumption that you’ll be making more money by then is not sound financial planning. That’s the same logic that helped me bury myself in debt.

When you buy a house, make sure to base your payments and your mortgage on what you can realistically afford. Anything else, and you’ll only end up poorer and less happy than when you started.

Inadvertent BOGO

I refuse to buy my kid more expensive video game systems. He’s got a friend who’s got one of each, going back 15 years.

We don’t do that, so he’s spent the last 6 months saving to buy his own XBox 360. After his birthday this month, he finally had enough, so we ordered it a few days ago.

Wednesday was the Great Unboxing.

I was making dinner in the kitchen while the punk and his friend unpacked the box from Amazon.

The squeals were normal. The shouts of “Dad, why did you buy two XBoxes?” were a surprise.

Two?

No.

Actually, yes. There were two of the things in the box. Did I order two? Did I accidentally pay for two?

Nope. The packing slip only listed one, my order history only showed one, and my credit card was only charged for one.

Yet, there were two in the box. Free XBox! Woot!

That means an XBox in the bedroom for Grand Theft Auto and Red Dead Redemption, and an XBox in the basement for Madden and Star Wars. No fighting. No turns to take. And it didn’t cost us an extra $200.

That’s all win.

If there’s nothing on the packing slip, then Amazon didn’t know I had it. Even if they did, I didn’t do anything to make them send it. There was no fraud. Legally, I had no obligation of any kind to do anything other than enjoy my new prize.

Lots of win.

The kids were excited. Everyone gets a turn. Multiplayer games.

The parents were excited. We get a turn. M-rated games.

So much freaking win in that box.

But….

There’s always a but.

We didn’t order it. We didn’t pay for it. It wasn’t ours.

A friend told me to sell it. She knows how hard we’re working to pay off debt.

A coworker said, “Screw them. They’re just a big corporation who’d be happy to screw you first.”

But it wasn’t ours.

I spent 12 hours trying to rationalize a way to keep it that wouldn’t be unethical, make me feel guilty, or–most important–send a horrible message to my kids.

I couldn’t do it.

It wasn’t ours.

I had a talk with my son. It was his money that got this little prize into our house, after all. He wanted to keep it, naturally. He’s got a lot to learn about persuasion. He acknowledged that sending it back was the right thing to do. He agreed that it would suck if the roles were reversed. His only argument in favor of keeping it was “I want it.”

Even he admitted that was completely lame.

It’s going back. I let him think that was his decision.

I talked to Amazon. They apologized for the inconvenience and gave me a UPS label to send it back at no cost. It didn’t cover pickup, but I’ve got a drop box in my office building, so I can deal with that.

My wife was pissed. The customer service rep never bothered to say thank you. She called Amazon to complain to a manager. After reminding him that we had no duty to return the free XBox, he gave us a $25 gift card to say thank you.

I love my wife.

My son, for deciding to to the right thing, gets to spend the gift card. My wife, for being awesome, gets to be with me. I miss my free XBox.

What would you do? Would you keep the free XBox, sell it, or send it back?

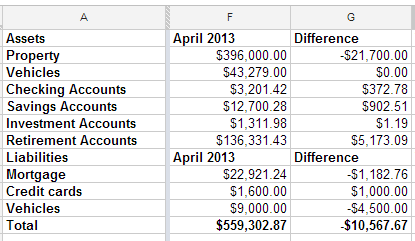

Net Worth Update

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.

Refinancing Your Existing Loan to Purchase An Investment Property

Many people are looking at the housing market slump right now as an investment opportunity. Here are a few of the things that you need to know before getting a new home loan or refinancing your existing loan in order to make that happen.

Amount You Want to Borrow

A lot of borrowers go shopping for real estate and have exactly no idea how much money they can borrow. One of the first questions that you need to ask before going real estate hunting is how much can I borrow. You can ask a bank, lender, or financial institution to give you a ballpark figure of the amount of loan that you would qualify for. This will make it easier for you to narrow down exactly what type of property you can afford and what areas you can concentrate on.

Amount of Interest You Will Pay

Too many people are overly concerned with the purchase price of the home that they are buying. They fail to find out how much interest they will have to pay back to the bank in order to make their home ownership dreams come true. This is where a home loan calculator can be really useful. You can find out exactly how much interest you will repay over a 10, 20, or 30 year loan time period. You can also change the interest rate and down payment amount on those calculators to see if you can secure a lower monthly payment.

Credit Score Needed to Qualify

It doesn’t matter if you are buying a home for the first time or refinancing an existing loan. Your credit score matters. You need to start doing some research now if you want to secure a loan with a really low interest rate. This involves taking the time to see what credit scores traditional lenders are looking for and doing the work necessary to qualify for this loan. Your credit score will make a big difference in determining if an investment property purchase is a profitable endeavor or one that winds up costing you money. It will depend heavily on what kind of loan your credit score allowed you to negotiate.

Make the Choice

Once you know how much you will need and exactly how much you will be paying out over the life of another mortgage, you can decide whether you want to refinance your current home loan to get another one. Adding on another huge debt to an existing one is a big risk. Make sure to think it through fully before jumping in.