- @Elle_CM Natalie's raid looked like it was filmed with a strobe light. Lame CGI in reply to Elle_CM #

- I want to get a toto portable bidet and a roomba. Combine them and I'll have outsourced some of the least tasteful parts of my day. #

- RT @freefrombroke: RT @moneybeagle: New Blog Post: Money Hacks Carnival #115 http://goo.gl/fb/AqhWf #

- TED.com: The neurons that shaped civilization. http://su.pr/2Qv4Ay #

- Last night, fell in the driveway: twisted ankle and skinned knee. Today, fell down the stairs: bruise makes sitting hurt. Bad morning. #

- RT @FrugalDad: And to moms, please be more selective about the creeps you let around your child. Takes a special guy to be a dad to another' #

- First Rule of Blogging: Don't let real life get in the way. Epic fail 2 Fridays in a row. But the garage sale is going well. #

Winning the Mortgage Game

There’s a game that’s often mistakenly called “The American Dream”. This game is expensive to play and fraught with risk. It single-handedly ties up more resources for most people than anything else they ever do.

The game is called Home Ownership.

At some point, most people consider buying a house. On the traditional, idealized life-path, this step comes somewhere between marriage and kids. That’s usually the easiest way to organize it. If you have kids first, you’re much less likely to buy a home. This is a game with handicaps.

Once you get to the point where you are emotionally ready to invest in the 30-year commitment that is a house, your first impulse tends to be to rush to the bank to find out how much money you can borrow.

That’s a mistake. If you take as much as the bank will qualify you for, you’re most likely to overextend yourself and end up losing your house. That’s the quick way to lose the home ownership game.

The best thing you could do is figure out how much you can afford before you visit a bank. Conventional wisdom says that your mortgage payment should be no more than 28% of your gross income, but that’s absurd. Who builds their budget on their gross income? I like 28%, but only of your net income. To make the numbers easier to remember, I’d round it to 30%. If you take home $3000 per month, your mortgage payment should be no more than $900 per month.

From there, it pretty easy to figure out how much house you can afford. Using this e mortgage calculator, you’d be able to afford a mortgage of $175,000 if we assume an interest rate of 4.5%. Throughout most of the United States, that will buy you a reasonably sized home, though certainly nothing ostentatious. Clydesdale Bank also has an excellent loan calculator.

Some people like to start out with an interest-only loan. That same emortgage calculator shows that an income of $3000 per month would be able to afford a $240,000 with almost the same payment. That seems like a good plan, but eventually, you’ll have to pay more than just the interest. Taking out a loan that will one day be more than you can afford on the assumption that you’ll be making more money by then is not sound financial planning. That’s the same logic that helped me bury myself in debt.

When you buy a house, make sure to base your payments and your mortgage on what you can realistically afford. Anything else, and you’ll only end up poorer and less happy than when you started.

Mortgage Race, Part 2

As I mentioned last month, Crystal and I are in a race to pay off our mortgages. The loser(henceforth known as “Crystal”) has to visit the winner. Now, since–judging by the temperature–Crystal lives in Hell, I think it would be good for her to visit in the winter. There something about the idea of going ice fishing, staring at a hole in the ice while sitting on a 5 gallon bucket, cursing the day I was born.

Today, she threw down the gauntlet again. She has apparently decided that, since her prerequisites are met, she’s going to win. Sure, she’s closed on her house and built her savings back up to $20000, but it doesn’t matter. I’ve sent a small army of arson-ninjas to keep her from getting ahead. They are so small, they can only carry tiny matches and single drops of gasoline, so the damage they can do is tiny, but it will add up. Just a word of advice: if you hire an army of arson-ninjas, go for the upsell and get ninjas that are at least 2 feet tall. Anything less is just inefficient.

When I announced the race last month, my mortgage balance was $26,266.40. Today, it is $25,382.53. In three days, there will be another $880 applied to the principal.

In February, our renters will move in and we’ll conservatively have another $650 to pay. When that starts, our balance should be around $23,000. Adding a portion of the rent payment should mean we pay off the house in May 2014. However, when I bring in our side hustle money, that will bring us back to September 2013.

Crystal’s projected payoff is July 2013, so I’ll have to hustle.

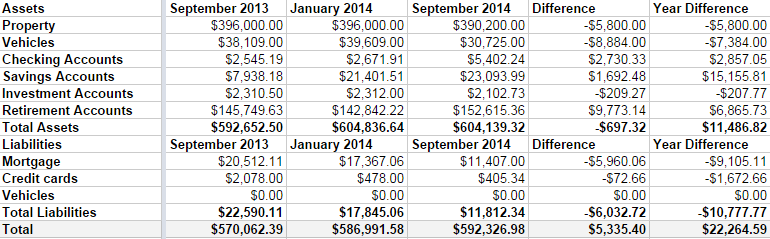

Net Worth Update – September 2014

It’s time for my irregular-but-usually-quarterly net worth update. It’s boring, but I like to keep track of how we’re doing. Frankly, I was a bit worried when I started this because we’ve been overspending this summer and Linda was off work for the season.

But, all in all, we didn’t do too bad.

Some highlights:

- Both of our properties lost around $3000 in value. I’m not worried, because we are keeping them both for the long haul. The rental is basically on auto-pilot, so that’s free money every month.

- We sold a boat that appraised for much less I had estimated in the last few updates. I had it listed for $5000, but it was worth $2000.

- I do have a credit card balance at the moment, but that goes away as soon as my expense check clears the bank, which will be in a day or two.

- We’re in the home stretch with the mortgage. There is $11,407 left to go, and we’ve paid down $9105 in the last year. By this time next year, I want that gone, gone, gone.

I can’t say I’m upset with our progress. We’ve paid down $6000 in debt in 2014, including 3 months with 1 income. We aren’t maxing our retirement accounts, yet, but I’d like to be completely debt free before I do that. It’s bad math, but having all of my debt gone will give me such a warm fuzzy feeling, I can’t not do it.

My immediate goal is to hit a $600,000 net worth by my next update in January. I’m only about $7000 off.

Time to hit the casino. Err, I mean, time to up my 401k contribution from 5% to 7%.

Birthday Parties are Evil

This is a post from my archives.

I hate birthday parties. Well, not all birthday parties. Not even most parties. Just the expensive-for-the-sake-of-expensive parties. The bar-raising parties. The status-boosting parties. I’m done.

My son is seven years older than my first daughter. In those seven years, with only one kid, we managed to spoil him regarding birthday parties. Every party was big and there were a lot of presents. That’s an expensive way to run a birthday and it is a lot of stress. We even moved the parties home, but still invited all of our friends and family. It was much too stressful.

A good friend used the pizza and game place, buying tokens for everyone at the party. That’s incredibly expensive. Even if I wanted to, I couldn’t afford that for three kids. There’s an element of keeping up with everyone around me, but I just can’t make myself care about that anymore. They aren’t paying my debt or cleaning my house. They don’t get a vote.

My plan this year was to have a sleepover for my son. He had five friends spend the night, playing games and watching movies. They giggled and squealed for eighteen hours, all for the cost of some take-and-bake pizzas and snacks. It was a hit for everyone involved. The other parents got a night off and all of the kids had a blast.

My girls are one and two. We’re done with parties for them, too. They got big parties for their first birthdays. Those are parties for the adults; the kids don’t care. In a few years–even a few months–they won’t remember the party. My older daughter’s birthday will be a trip to the apple orchard, followed by cake and ice cream. She’ll get presents. She’ll get “her day”. She’ll remember that her birthday is special, without costing a lot of money.

We want them to have fun. We want them all to feel special. We also want to manage their expectations and keep the parties from breaking the budget. So far this year, it is working.

How do you run a birthday party on a budget?

Cutting Costs While Cutting Hair

About once per quarter, my wife and I have a…I won’t call it a fight. It’s more like she-comes-home-looking-stunning-while-I-make-disapproving-grunting-sounds-while-giving-the-checkbook-dirty-looks.

I hate salons.

$80 for highlights, $30 for a haircut and $15 for eyebrow “shaping”. It’s an afternoon of chemicals and hot-wax torture, for the low, low price of $125 + tip. Frugal it’s not, but that’s an argument I lost long ago.

This weekend, she tried something new.

Beauty school.

For roughly the cost of materials, she got her eyebrows “shaped” and her hair highlighted and cut by a senior student at the beauty school, under the supervision of a licensed beautician/instructor.

It looks good, and she said she had more fun during her appointment than any other salon trip she’s had. I guess there’s something to be said for interacting with someone who isn’t burned out on interacting with the general public.

What does it cost? What normally runs $125 cost just $35. That’s for a $5 cut, $25 highlighting, and $5 wax. That’s a $90 savings or 72% off. Yay!

Other services they offer include:

- Full color, cut and shampoo for $20.

- A Perm for $25.

- Mani/pedi for $24.

- Full set of acrylic nails for $15.

- Wax for $5. Have I ever mentioned that I am happy to be a guy?

- Seaweed treatment for $10. I don’t even know what this is. A buffet, maybe?

They also have a “Princess” package that we’re going to use for brat #2’s birthday party next month. It’s an up-do, nail polish, make-up, and tiara for $10 per kid. We’ll take the girls out to get made up all pretty-like, then off to the dollar theater, for a $35 party.

The school my wife visited has more than 90 locations in 21 states, but I’d be willing to be every city big enough to support a Wal-Mart also has a beauty school nearby. They don’t tend to advertise their customer services, so you’ll have to call, but for a 70% discount, it worth spending a bit of time on the phone, isn’t it?

I have two questions for you, dear readers:

- Would you consider going to a beautician trainee?

- What the heck is a seaweed treatment?