Please email me at:

![]()

Or use the form below.

[contact-form 1 “Contact form 1”]

The no-pants guide to spending, saving, and thriving in the real world.

Please email me at:

![]()

Or use the form below.

[contact-form 1 “Contact form 1”]

In this installment of the Make Extra Money series, I’m going to show you how I do keyword research.

Properly done–unless you get lucky–this is the single most time-consuming part of making a niche site. If you aren’t targeting search terms that people use, you are wasting your time. If you are targeting terms that everybody else is targeting, it will take forever to get to the top of the search results.

Spend the extra time now to do proper keyword research. It will save you a ton of time and hassle later. This is time well-spent.

If you remember from the last installment, when we researched products to promote, we narrowed our choices down to a few products.

What I’ve done is create a spreadsheet to score the products. You can see the spreadsheet here. I’ll explain the columns as we populate them.

The first column contains the name of the product. Easy. We’ve got 10 products. I’m going to walk through scoring 1 product, then, through the magic of the internet, I’ll populate the rest, and you’ll get to see the results instantly. Wow.

The second column is the global search volume for the exact search term. I base my product niche sites primarily on the demand for a given product. Everything else is a secondary consideration.

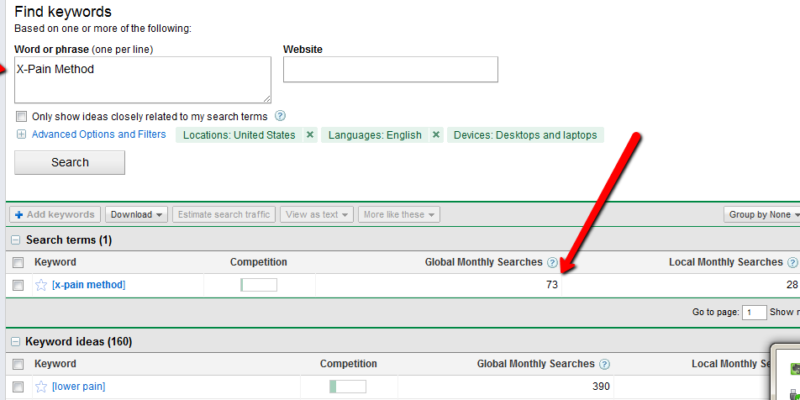

To find the demand for a product, go to the Google Adwords Keyword Tool. In the “word or phrase” box, enter your product name, exactly. In this case, it’s “X-Pain Method”. When the search results come up, change the match type to “Exact”. You should have something like this:

Enter the global search volume in column 2. In this case, it’s 73. Keep this window open, because we’ll be coming back to it.

Column 3 is the search competition. Go to google and enter your product name, in quotes. In this case, “X-Pain Method”. Put the total number of search results in column 3: 223000.

Column 4 is the search competition, but only what appears in a page’s title. Your search query is intitle:”X-Pain Method”, which yields 4400 results.

The next column is for the average PageRank of the first page of search results. For this, I use Traffic Travis. I use the 4th edition, which is paid software, but you can get the free version of version 3, instead. I’ll use version 3 for this example. Open the software and click on “SEO Analysis” on the bottom left of the screen. Put your search term (“X-Pain Method”) in the “phrase to analyze” and set the “Analyze Top” to 10, then hit “Analyze”. When it’s done running, just add up all of the PRs and divide by 10. Ignore Travis’s difficulty rating.

Now, for the rest of the columns, we’re going to look at the keyword tool again. We’re going to pick 3 alternate search terms. Here are the criteria:

Once we pick the keywords, we’ll throw them into google to get the competition, just like we did to populate column 2.

“Exercises for back pain” has medium competition and 1900 monthly searches. It also has an estimated cost-per-click of $3.02, which means people are paying for this.

“Lower back pain exercises” has 6600 searches and medium competition. It’s actually on the lower end of medium, so it looks really promising.

“Lower back” has 4400 searches and low competition, with a CPC of $6.24. This should be a good one. Scratch that. It has 40 million search results, but only 4400 searches. That’s a lot of competition for a small market.

Instead, I’m going to search for “cure back pain” in the keyword tool and see what I get. “Upper back pain” is better. Low competition, 18000 searches each month, and only 2000000 competing search results. Now, I’ll score it.

You really want at least 500 searches per month for the product name. More than 2500 is better. I’m going to assign 1 point per 500 monthly searches.

You also want a lower number of search results. Less than 10,000 is ideal. Less than 100,000 is still decent. More than 250,000, I’d walk. So, under 10,000 gets 5 points. Under 50,001 gets 4. Under 100,001 gets 3. Under 200,001 gets 2. Under 250,001 gets 1. Any higher gets 0.

The ideal intitle search will have less than 2000 results. More than 100,000 is too time-consuming to deal with. 0-2000: 5 points; 2001-10,000: 4 points; 10001-25000: 3 points; 25001-50000: 2 points; 50001 to 100000: 1 point.

The perfect product will have the first page of search result all with a PageRank of 0. That’s a 5 point product. I’ll knock off half a point for every point of average PR.

The related terms are more relaxed. They are what’s known as “Latent Semantic Indexing” (LSI) terms. We will be creating articles to match those search terms, mostly to make our niche site look as natural and real as possible. Any actual traffic those pages drive is just gravy. Points for the related searches start at 10 and get 1 point knocked off for each 3 million results. We’ll be treating the 3 terms as one for this score.

That gives us a perfect score of about 25. There’s no actual upper limit, since the score for the search volume has no upper limit. X-Pain Method scored 18.22.

Now, excuse me a moment while I score the rest.

I’m back. Did you miss me?

I’ve finished scoring each of the products and sorted the results by score. The clear winner is the back pain product, but the lack of searches bothers me. The wedding guide looks much nicer, especially if I target the phrase “wedding planning guide” during the SEO phase of the project. That change alone brings the score almost to first place.

Frankly, I’d take either 2nd or 3rd place over the back pain product. The bare numbers don’t support it, but my judgement tells me they are better products to promote.

There is one final step before deciding on the product. I have to buy it. I can’t review the product without seeing it and I can’t promote it without approving of it.

That’s the secret to ethical niche marketing, you know. Only promote good products that you’ve personally read, watched, or used.

When you are up to your eyeballs in debt, praying for a step-stool, sometimes life–more accurately, con-artists–try to trip you when you are vulnerable and look for a solution. They aren’t muggers on the street. They come at you wearing ties, invite you to a real office, with real furniture and a real nameplate on a real desk. They are a real company, but that doesn’t mean they aren’t trying to scam you out of the little money you have left to put towards your debt.

Yes, I am talking about debt management scams. These scams come in 4 main varieties.

Debt Settlement companies instruct you to stop paying your bills completely and send them the money instead to be placed in a settlement fund. When your creditors get desperate enough, they will be willing to settle for pennies on the dollar.

In theory, this can be a good strategy for some debtors. Unfortunately, it has some drawbacks, even if the company is legitimate. They tend to charge high fees as a percentage of your deposits. Some take another fee when a settlement is accepted. The entire time you are building your settlement fund, your credit rating is sinking, leaving you open to being sued or garnished. The bad companies take the fund and run, while even the good companies can’t guarantee your creditors will play ball.

Ultimately, they aren’t doing anything you can’t easily do yourself. If you want to go the settlement route, stop making your payments and funnel the money into a savings account that you will use to offer settlements from. It takes discipline, but there is no upside to paying someone else for the same function.

Debt Management plans are used when you owe more than you can afford to pay. These companies work with your creditors to adjust interest rates and minimum payments and they try to get some fees waived for you.

A good company will work with you and your creditors to make sure everyone is working together towards the goal of eliminating the debt. A bad company will tell you they are working with your creditors while ignoring any contact from the creditor. They’ll tell you the creditor isn’t willing to negotiate while never stepping up to the negotiation table. Another trick is to offer the creditor a set payment, with a “take it or leave it” clause. Any input from the creditor is interpreted as a refusal to participate. This, coupled with high fees paid by the debtor, make debt management firms a risky proposition. Most states require the firms to be licensed. Check to make sure they are before giving them any information.

Debt/Credit Counseling companies work with you to establish a budget and eliminate expenses; in effect, they are training you to be in control of your finances. They are often organized as a nonprofit, but not always.

Some–the sleazy ones–lie about what they are doing, or attempt to misconstrue what you are agreeing too. Be careful not to use your home as collateral to consolidate unsecured debt and don’t walk into a Chapter 13 bankruptcy without that being your intention. Both of those are common debt counseling scams. If the company isn’t able to provide all of the details of a transaction–company name, address, licensing information–or they aren’t willing to spend as much time as necessary explaining the details of the transaction, walk away. This is your life, you are in charge of it. Don’t let anyone bully or prod you into signing something you aren’t comfortable with.

Credit Repair is almost always a scam. There are ways to get correct bad information removed from your credit report. If the information is correct, those methods are illegal. There are two legal methods to repair your credit. First, stop generating bad credit. Make your payments on time and eventually, the bad items will fall off. Second, write letters disputing the actual incorrect items on your credit report. There are no quick fixes, and anybody telling you different is flirting with a jail sentence, possibly yours.

How do you avoid the scammers?

There is no magic bullet to kill debt. You’re not fighting a werewolf, you’re fighting a lifetime of bad or unfortunate choices and circumstances. It’s important to keep a realistic outcome in mind.

Update: This post has been included in the Carnival of Debt Reduction.

Ahhh, New York City. The Mecca of all that is glamorous, rich, luxurious and exciting. To some, the good life. So, you’re ready to pack your bags and head for the big city? Slow down there, big dreamer. The cost of

EVERYTHING in the city is higher than the national average, meaning your 70K per year needs to be 166K in New York City to keep your current lifestyle. Let’s talk about the basics here: lodging, food and entertainment:

If rent has not broken you, you must also eat! I mean, you won’t be eating MUCH after paying rent, but you will need a nibble here and there. It will come as no surprise that the restaurants in New York City are pricey. Celebrity favorites such as the Four Seasons, Le Cirque and Nobu are over $50.00 PER PERSON. I just choked on my Diet Coke. Eateries such as McDonald’s and local Mexican restaurants are abundant, but they too are higher priced than elsewhere. Your best bet? Learn to cook. Eat leftovers. Use coupons. Pair those coupons with sale items. Find a generous and rich companion. Skip meals.

As far as entertainment goes, I’m afraid at this point, your only entertainment will be browsing the web for supplementary forms of income. Seriously, unless you are in the 1%, utilize the many forms of free entertainment that New York City has to offer. A jog through Central Park, window shopping or a walk through the city all offer ample opportunity for fun free of charge. Sadly, Broadway plays and designer shopping must be left to the rich and famous.

In conclusion, one can lead a good, but not extravagant, life in New York City on a normal income. Be prepared to work hard, save hard and live frugally. Unless you’re living on money that is coming from an investment or dividend, you shouldn’t expect anything more. Listen, New York City is exciting, good grief, it’s the “city that never sleeps,” but it isn’t cheap. Of course, the people I know who have lived there for a short stint of time had little money and have since moved on – with no regrets and countless memories from that season of life.

Even as a growing number of analysts are questioning the details of Obamacare, the sudden hospitalization of Teresa Heinz Kerry, the wife of former senator and current U.S. Secretary of State John Kerry, provides additional fodder to the ongoing healthcare debate.

Heinz, who is 74 years old, is the heir to the Heinz ketchup fortune. She is the widow of former Senator John Heinz, who was killed in 1991 in an aviation accident. Her marriage to Kerry in 1995 occurred when he was the senator from Massachusetts. Heinz was hospitalized on Sunday and is reported to be in critical condition after being flown to Massachusetts General Hospital in Boston.

Heinz was treated for breast cancer in December 2009 and went through two operations for lumpectomies. It is not known what specific health issues resulted in the current hospitalization. However, sources indicated that there was concern over the return of the cancer.

Regardless of the source of the current illness, it is taken for granted that Heinz will receive the very best of medical care, with cost being of no concern to treatments pursued. In the earlier process of treating her cancer, numerous doctors at the nation’s finest medical facilities were consulted. The issue of Heinz not having to worry about the costs of her care is the central theme of many who criticize our nation’s health care system.

For the millions of Americans who live daily without health insurance or any form of coverage, there is a constant concern over how they would deal with a medical emergency. These individuals know that they are one accident or serious illness away from devastating financial hardship. In fact, the single biggest reason for bankruptcy in the U.S. today is medical bills. According to the latest studies, the average hospital stay billed out at $15, 700, with an average daily cost of nearly $4,000.

These costs are onerous because so many people today find health insurance increasingly unaffordable. While the political debate over the current healthcare reform continues, there is one simple fact. That reality is that the annual cost of private health insurance, already out of the reach of many, has risen by as much as 50 percent in the last two years. Many plans for a family of four are now over $15,000 and it is predicted that a bronze plan under the implemented Obamacare will exceed $20,000 for that same family.

All of this brings us back to the hospitalization of Heinz. The reality we live in today means that many people diagnosed with cancer or other similar diseases have little hope of receiving the treatment or care that the wealthy can afford. Even with quality health care insurance, the co-pays and other costs create burdens that many cannot carry.

There are no simple or ready solutions to this situation. The morality of one patient dying because chemotherapy is too expensive while one with a large bank account survives is an issue that will see intensified debate in the coming months and years. Regardless of what caused the current hospitalization, Heinz is one of the lucky ones who will have superb medical care without financial considerations.

board game")

There’s a saying that you are the average of your 5 closest friends. Take a look at the people you hold dearest. Combined, they are you. If they are all in debt, chances are, so are you.

As a corollary, you are a part of your friends. If you become more financially responsible, it will rub off on the people who care about you.

Given these two rules, one way to improve yourself is to help those around you improve themselves. If your influence convinces your friends to move closer to your ideal, it will be easier, almost effortless to move closer to it, yourself.

It sound manipulative, but if you are manipulating your friends, you are doing it wrong. Don’t try to force or trick your friends, just be honest and sincere in your efforts to help. Nobody wants to be in debt. This is you being nice.

While it is okay to splurge occasionally, don’t be afraid to suggest less expensive activities. If someone suggests going to a movie, mention the dollar theater. If they want to go out for dinner, offer to host a potluck. Trip to the casino? Game night at your house. There are almost always cheaper ways to have fun. As long as you are spending time with the people you love, you’ll have a good time. Do you really need to drop $100 to do that?

If you buy an iPod and immediately run to show it off, you are going to trigger a case of “keeping up with the Joneses”. If your friends spend all of their time around people who are constantly buying expensive toys, buying expensive toys becomes normalized in their minds. Debt becomes the norm. Then extreme debt. Don’t reinforce the destructive debt cycle by showing off the expensive trophies of excessive, unnecessary consumerism.

This is a fine line to walk. If mention how much money your friend is wasting on 13 shot venti soy hazelnut vanilla cinnamon white mochas with extra white mocha and caramel every single morning, you’re going to get annoying fast. In fact, you are already annoying me, so knock it off. On the other hand, if Caribou is having a sale on the 13 shot monstrosity, speak up. Nobody is going to complain about getting a $15 coffee for less than $10.

If you’ve got a friend who’s into landscaping and you’ve got a neighbor who needs a landscaper, make the connection! If you know a web designer and a business in need of a website, get them together. Do what you can to match the needs of the people around with each other. They will all appreciate it, and everyone will be better off. Be the guy who helps everyone connect with the people they need.

Put another way, don’t be a dick. Nobody likes being nagged. Nobody likes being told they are doing everything wrong. Be encouraging, not mean.

If you can do all of that, it’s natural that your friends will start acting the way you want yourself to act. The less they want to waste on a trip into debt, the less tempted you will be to do the same.