LRN got hacked this morning. Thankfully, I backup weekly and subscribe to my own RSS feed. 20 minutes to total restoration.

ING Rocks

I just got an email from INGDirect. To celebrate Independence Day, they are having a sweet, sweet sale.

You can:

- Open a checking account and get between $50 and $126 for doing so.

- Open a Sharebuilder account and get $76 to start buying stocks.

- Get $1776 knocked off the closing costs of a mortgage.

- Get $76 in a new IRA, to give you a little boost for retirement.

Take advantage of all of that and you’ll get $2054 in cash or discounts.

Seriously, this deal rocks. If you don’t have an INGDirect account, get one. There are no overdraft fees and no monthly fees.

The sale ends tomorrow at midnight, so hurry.

Apple Launches iPad Air in November

With a lighter and thinner chasis, the newly announced iPad Air has a more powerful processor with a great new design and performance features that’s sure to continue Apple’s trend setting reputation. Apple senior vice president Phil Schiller is calling it the biggest leap forward for a full-sized iPad. We expect people have already started packing overnight bags for their long wait on the sidewalks outside the stores.

Apple is promoting its newest innovation as having the power of lightness, hence the addition of the “Air” moniker. That’s because the iPad Air weighs a mere pound and even then doesn’t feel like it. It’s 7.5 millimeters thin and has a design that might remind you of the iPad mini. It’s been engineered with a smaller bezel that shrinks the tablet without losing any screen size. The new dimensions and weight actually makes it easier to hold the tablet in one hand.The device will certainly impress its fans with its incredible power. The new A7 chip has a 64 bit architecture, providing graphics and CPU processing that’s significantly faster than the previous version. Working alongside the A7, the M7 motion co-processor, according to Apple, provides a graphic performance that’s over 70 times faster than the processor in the original iPad model. In fact, in terms of graphics, the Retina Display is likely the most impressive aspect of the new iPad. Graphics promise to render at two times the speed of the last iPad. The pared down bezel makes the screen stand out prominently.The iPad Air is supposed to give a user the chance to do more in more places with an advanced wireless connection. It’s faster than ever in more locations than ever before. The iPad Air brings a WiFi performance twice the speed of the last iPad. It utilizes two antennas instead of one, and MIMO, the latest in communication and smart antenna technology. The WiFi and Cellular model will support more LTE brands, offering greater support and quicker connection anywhere in the world.

With almost a half million apps already available for the iPad, you have a great head start on things to do. Apps built into the iPad Air will include solutions for routine tasks, like web surfing and checking email. A number of previously apps that had to be purchased are now free, such as iMovie, Keynote, iPhoto, GarageBand and Pages. Popular apps for other Apple products, they have all been upgraded to work with iOS 7 and the iPad. Quickly put together an original song or detail a presentation anywhere. As a lot of apps are developed solely for Apple products, these can look stunning on their displays.

The iPad Air’s current launch date is November 1. It will come in black and gray or silver and white. It will start at $499 for a 16 gigabyte WiFi version. This is $100 more than previous generation launches, but supporters say the consumer is getting more screen real estate. The Cellular model will retail for $629. The iPad 2 will continue in the stores for $399.

Related articles

Net Worth Update

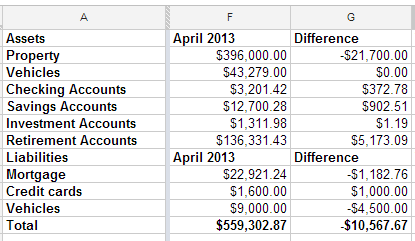

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.

Why I Hate Payday Loans

I hate payday loans and payday lenders.

The way a way a payday loan works is that you go into a payday lender and you sign a check for the amount you want to borrow, plus their fee. They give you money that you don’t have to pay back until payday. It’s generally a two-week loan.

Now, this two week loan comes with a fee, so if you want to borrow $100, they’ll charge you a $25 fee, plus a percent of the total loan, so for that $100 loan, you’ll have to pay back $128.28.

That’s only 28% of actual interest; that’s not terrible. However, if you prorate that to figure the APR, which is what everyone means when they say “I’ve got a 7% interest rate”, it comes out to 737%. That’s nuts.

They are a very bad financial plan.

Those loans may save you from an overdraft fee, but they’ll cost almost as much as an overdraft fee, and the way they are rigged–with high fees, due on payday–you’re more likely to need another one soon. They are structured to keep you from ever getting out from under the payday loan cycle.

For those reasons, I consider payday loan companies to be slimy. Look at any of their sites. Almost none are upfront about the total cost of the loan.

So I don’t take their ads. When an advertiser contacts me, my rate sheet says very clealy that I will not take payday loan ads. The reason for that is–in my mind–when I accept an advertiser, I am–in some form–endorsing that company, or at least, I am agreeing that they are a legitimate business and I am helping them conduct that business.

In all of the time I’ve been taking ads, I’ve made exactly one exception to that rule. On the front page of that advertiser’s website, they had the prorated APR in bright, bold red letters. It was still a really bad deal, but with that level of disclosure, I felt comfortable that nobody would click through and sign up without knowing what they were getting into. That was a payday lender with integrity, as oxymoronic as that sounds.