- RT @Dave_Champion Obama asks DOJ to look at whether AZ immigration law is constitutional. Odd that he never did that with #Healthcare #tcot #

- RT @wilw: You know, kids, when I was your age, the internet was 80 columns wide and built entirely out of text. #

- RT @BudgetsAreSexy: RT @FinanciallyPoor "The real measure of your wealth is how much you'd be worth if you lost all your money." ~ Unknown #

- Official review of the double-down: Unimpressive. Not enough bacon and soggy breading on the chicken. #

- @FARNOOSH Try Ubertwitter. I haven't found a reason to complain. in reply to FARNOOSH #

- Personal inbox zero! #

- Work email inbox zero! #

- StepUp3D: Lame dancing flick using VomitCam instead or choreography. #

- I approve of the Nightmare remake. #Krueger #

Twitter Weekly Updates for 2010-05-29

- RT @ramseyshow: RT @E_C_S_T_E_R_I_: "Stupid has a gravitational pull." -D Ramsey as heard n NPR. I know many who have not escaped its orbit. #

- @BudgetsAreSexy KISS is playing the MINUTE state fair in August. in reply to BudgetsAreSexy #

- 3 year old is "reading" to her sister: Goldilocks, complete with the voices I use. #

- RT @marcandangel: 40 Useful Sites To Learn New Skills http://bit.ly/b1tseW #

- Babies bounce! https://liverealnow.net/hKmc #

- While trying to pay for dinner recently, I was asked if other businesses accepted my $2 bills. #

- Lol RT @zappos: Art. on front page of USA Today is titled "Twitter Power". I diligently read the first 140 characters. http://bit.ly/9csCIG #

- Sweet! I am the number 1 hit on Ask.com for "I hate birthday parties" #

- RT @FinEngr: Money Hackers Carnival #117 Wedding & Marriage Edition http://bit.ly/cTO4FU #

- Nobody, but nobody walks sexy wearing flipflops. #

- @MonroeOnABudget Sandals are ok. Flipflops ruin a good sway. 🙂 in reply to MonroeOnABudget #

- RT @untemplater: RT @zappos: "Do one thing every day that scares you." -Eleanor Roosevelt #

The Luxury of Vacation

This was a guest post I wrote last year to answer the question posed by the Yakezie blog swap, “Name a time you splurged and were glad you did.”

There are so many things that I’ve wanted to spend my money on, and quite a few that I have. Just this week, we went a little nuts when we found out that the owner of the game store near us was retiring and had his entire stock 40% off. Another time, we splurged long-term and bought smartphones, more than doubling our monthly cell phone bill.

This isn’t about those extravagances. This is about a time I splurged and was glad I did. Sure, I enjoy using my cell phone and I will definitely get a lot of use out of our new games, but they aren’t enough to make me really happy.

The splurge that makes me happiest is the vacation we took last year.

Vacations are clearly a luxury. Nonessential. Unnecessary. A splurge.

When we were just a year into our debt repayment, we realized that, not only is debt burnout a problem, but our kids’ childhoods weren’t conveniently pausing themselves while we cut every possible extra expense to get out of debt. No matter how we begged, they insisted on continuing to grow.

Nothing we will do will ever bring back their childhoods once they grow up or—more importantly—their childhood memories. They’ll only be children for eighteen years. That sounds like a long time, but that time flies by so quickly.

We decided it was necessary to reduce our debt repayment and start saving for family vacations.

Last summer, we spent a week in a city a few hours away. This was a week with no internet access, no playdates, no work, and no chores. We hit a number of museums, which went surprisingly well for our small children. Our kids got to climb high over a waterfall and hike miles through the forest. We spent time every day teaching them to swim and play games. Six months later, my two year old still talks about the scenic train ride and my eleven year old still plays poker with us.

We spent a week together, with no distractions and nothing to do but enjoy each other’s company. And we did. The week cost us several extra months of remaining in debt, but it was worth every cent. Memories like we made can’t be bought or faked and can, in fact, be treasured forever.

You’re not alone: Help with Bankruptcy & Debt

Frequently regarded as an indication of personal failure, bankruptcy is still today widely considered a highly sensitive topic. Many will even feel uneasy speaking about their debt problems with close relatives and friends. If you, too, are facing serious debt issues and are in need of help, rest assured you are not the only one afraid of sliding into bankruptcy. In fact, thousands of households in the UK are threateningly close to insolvency and most are experiencing the exact same feelings of shame and despair. This perfectly understandable reaction has, meanwhile, unfortunately overshadowed the fact that there are hands-on practical steps especially designed to help you resolve your debt situation.

Frequently regarded as an indication of personal failure, bankruptcy is still today widely considered a highly sensitive topic. Many will even feel uneasy speaking about their debt problems with close relatives and friends. If you, too, are facing serious debt issues and are in need of help, rest assured you are not the only one afraid of sliding into bankruptcy. In fact, thousands of households in the UK are threateningly close to insolvency and most are experiencing the exact same feelings of shame and despair. This perfectly understandable reaction has, meanwhile, unfortunately overshadowed the fact that there are hands-on practical steps especially designed to help you resolve your debt situation.

There is a good reason why addressing the issue of bankruptcy has an urgent ring to it. Recent statistics indicate a steady rise of individual company insolvencies in the UK, particularly since the 1990s. According to the British Insolvency Service, the rate of bankruptcy on an individual level has risen from a total of 24,441 in 1997 to staggering 106,645 in 2007 in England and Wales. Alarmingly, the peak doesn’t seem to have been reached yet. As respected online-service ‘This is Money’ reports, ‘record numbers of people were declared insolvent in England and Wales’ in 2010, further noting that ‘an all-time high of 135,089 people were declared insolvent in 2010—0.7% up on the total for 2009.’ As you can gather from these numbers, you are certainly not alone with your debt problems: Around 140,000 adults are facing bankruptcy as a direct consequence of mishandling their debt issues, which translates to 385 new cases per day. It has already been pointed out that ‘the number of victims will be enough to fill both the London 2012 Olympic stadium and the Emirates Stadium.’

So, if you’re facing bankruptcy, there’s no need to feel ashamed. By taking an active stance and addressing your debt issues, you may even be able to avert insolvency altogether. With years of experience and several distinctions to our credit, the Debt Advisory Line have established themselves as leading experts in the field of debt management. We’ve already helped thousands of individuals and households who thought bankruptcy was their only option. Settling debt issues is our forte – and you shouldn’t settle with anything less.

This post brought to you by Debt Advisory Line.

Late Pass: Insurance for the Terminally Ill?

This is a guest post.

Uh oh. Not only have you put in decades of loyal service for a company that does not offer a life insurance policy to employees, now you have a terminal disease that has numbered your days. You always meant to get a life insurance policy at some point, but it was just one of those things that there was never enough money left for at the end of a month after bills, groceries and just enough fun to make worthwhile.

Your life is one that needs insuring to protect your family following the now-inevitable, but has that ship sailed? Is it possible to make up for lost time by obtaining a life insurance policy as a terminally ill patient?

You already know that insurance companies are experts at assessing risk. Each potential policy holder is effectively examined to determine their likelihood of living a reasonably long time, and a terminal illness is an obvious negative in this department.

Many insurance companies will be hesitant to offer a comprehensive policy that they know they will have to pay out in fairly short order, but you may be able to get a type of life insurance known as graded premium life insurance.

With graded premium life insurance, you pay a monthly premium to retain coverage. If your illness should terminate within two years, your family will receive all the premiums you have paid as a benefit. Should you last longer, the insurance provider pays the full value of the policy. This is a compromise that gives you the peace of mind that a life insurance policy can provide while allowing the insurance provider to minimize their risk.

These policies typically have cash values ranging from $10,000 to $50,000, so while they might not guarantee the permanent stability of your family, it will offer them much-needed assistance through what is sure to be a difficult time in their lives. Premium amounts vary by age and relative health, but generally the closer you are to qualifying for a payout, the more it costs to enter the lottery.

Life is unpredictable except for its certain end, and sometimes this reality leaves us less prepared for the future as we would like. Fortunately, a terminal illness does not make a person completely uninsurable in most cases. Of course, it is much easier and less expensive to get life insurance as a person who is not dying, so the best strategy may be to invest before your health becomes an issue.

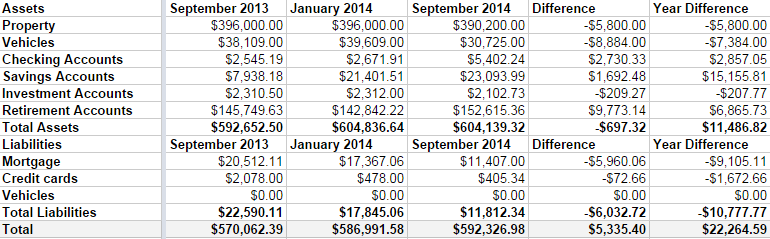

Net Worth Update – September 2014

It’s time for my irregular-but-usually-quarterly net worth update. It’s boring, but I like to keep track of how we’re doing. Frankly, I was a bit worried when I started this because we’ve been overspending this summer and Linda was off work for the season.

But, all in all, we didn’t do too bad.

Some highlights:

- Both of our properties lost around $3000 in value. I’m not worried, because we are keeping them both for the long haul. The rental is basically on auto-pilot, so that’s free money every month.

- We sold a boat that appraised for much less I had estimated in the last few updates. I had it listed for $5000, but it was worth $2000.

- I do have a credit card balance at the moment, but that goes away as soon as my expense check clears the bank, which will be in a day or two.

- We’re in the home stretch with the mortgage. There is $11,407 left to go, and we’ve paid down $9105 in the last year. By this time next year, I want that gone, gone, gone.

I can’t say I’m upset with our progress. We’ve paid down $6000 in debt in 2014, including 3 months with 1 income. We aren’t maxing our retirement accounts, yet, but I’d like to be completely debt free before I do that. It’s bad math, but having all of my debt gone will give me such a warm fuzzy feeling, I can’t not do it.

My immediate goal is to hit a $600,000 net worth by my next update in January. I’m only about $7000 off.

Time to hit the casino. Err, I mean, time to up my 401k contribution from 5% to 7%.