- RT @MoneyMatters: Frugal teen buys house with 4-H winnings http://bit.ly/amVvkV #

- RT @MoneyNing: What You Need to Know About CSAs Before Joining: Getting the freshest produce available … http://bit.ly/dezbxu #

- RT @freefrombroke: Latest Money Hackers Carnival! http://bit.ly/davj5w #

- Geez. Kid just screamed like she'd been burned. She saw a woodtick. #

- "I can't sit on the couch. Ticks will come!" #

- RT @chrisguillebeau: U.S. Constitution: 4,543 words. Facebook's privacy policy: 5,830: http://nyti.ms/aphEW9 #

- RT @punchdebt: Why is it “okay” to be broke, but taboo to be rich? http://bit.ly/csJJaR #

- RT @ericabiz: New on erica.biz: How to Reach Executives at Large Corporations: Skip crappy "tech support"…read this: http://www.erica.biz/ #

How to Prioritize Your Spending

Don’t buy that.

At least take a few moments to decide if it’s really worth buying.

Too often, people go on auto-pilot and buy whatever catches their attention for a few moments. The end-caps at the store? Oh, boy, that’s impossible to resist. Everybody needs a 1000 pack of ShamWow’s, right? Who could live without a extra pair of kevlar boxer shorts?

Before you put the new tchotke in your cart, ask yourself some questions to see if it’s worth getting.

1. Is it a need or a want? Is this something you could live without? Some things are necessary. Soap, shampoo, and food are essentials. You have to buy those. Other things, like movies, most of the clothes people buy, or electronic gadgets are almost always optional. If you don’t need it, it may be a good idea to leave it in the store.

2. Does it serve a purpose? I bought a vase once that I thought was pretty and could hold candy or something, but it’s done nothing but collect dust in the meantime. It’s purpose is nothing more than hiding part of a flat surface. Useless.

3. Will you actually use it? A few years ago, my wife an cleaned out her mother’s house. She’s a hoarder. We found at least 50 shopping bags full of clothes with the tags still attached. I know, you’re thinking that you’d never do that, because you’re not a hoarder, but people do it all the time. Have you ever bought a book that you haven’t gotten around to reading, or a movie that went on the shelf, still wrapped in plastic? Do you own a treadmill that’s only being used to hang clothes, or a home liposuction machine that is not being used to make soap?

3. Is it a fad? Beanie babies, iPads, BetaMax, and bike helmets. All garbage that takes the world by storm for a few years then fades, leaving the distributors rich and the customers embarrassed.

4. Is it something you’re considering just to keep up with the Joneses? If you’re only buying it to compete with your neighbors, don’t buy it. You don’t need a Lexus, a Rolex, or that replacement kidney. Just put it back on the shelf and go home with your money. Chances are, your neighbors are only buying stuff so they can compete with you. It’s a vicious cycle. Break it.

5. Do you really, really want it? Sometimes, no matter how worthless something might be, whether it’s a fad, or a dust-collecting knick-knack, or an outfit you’ll never wear, you just want it more than you want your next breath of air. That’s ok. A bit disturbing, but ok. If you are meeting all of your other needs, it’s fine to indulge yourself on occasion.

How do you prioritize spending if you’re thinking about buying something questionable?

Carnival Roundup

Live Real, Now was included in two carnivals last week:

Carnival of Personal Finance #348 hosted by Money Qanda

and

Yakezie Carnival hosted by 101 Centavos

Thanks to all of the hosts for including my posts.

Get More Out of Live Real, Now

There are so many ways you can read and interact with this site.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!

Carnivals This Week

I seem to be failing frugal parenting. My son spent the entire week telling me how happy he’d be if we could go to the game store so he could spend some of his money. Tying emotions to shopping is badbadbad.

Live Real, Now was included in four carnivals last week:

Carnival of Financial Planning – Edition #224 at AaronHung.com

Yakezie Carnival – Mardi Gras Edition at Young Adult Finances

Canadian Finance Carnival #76 at Canadian Finance Blog

Carnival of Financial Camaraderie – Rain Man Edition at Thirty Six Months

Thanks to all of the hosts for including my posts.

Get More Out of Live Real, Now

There are so many ways you can read and interact with this site.

You can subscribe by RSS and get the posts in your favorite news reader. I prefer Google Reader.

You can subscribe by email and get, not only the posts delivered to your inbox, but occasional giveaways and tidbits not available elsewhere.

You can ‘Like’ LRN on Facebook. Facebook gets more use than Google. It can’t hurt to see what you want where you want.

You can follow LRN on Twitter. This comes with some nearly-instant interaction.

You can send me an email, telling me what you liked, what you didn’t like, or what you’d like to see more(or less) of. I promise to reply to any email that isn’t purely spam.

Have a great week!

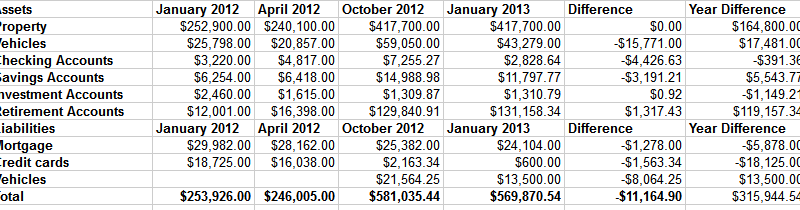

Net Worth Update

Welcome to the New Year. 2013 is the year we all get flying cars, right?

Here is my net worth update, along with the progress we made over the course of 2012.

As you can see, our net worth contracted by about $11,000. Part of that difference is due to selling our spare cars and–against my better judgement–taking payments with a lien on one of them. That is supposed to be paid off within a couple of months. If not, I’ll play repo man again.

The other part of the difference is in the final preparations for our rental property. The only things left to do are sanding and polishing the hardwood floors and cleaning the living room carpet. The final push to get to this point cost some money. All told, we’re nearly $30,000 into getting the house ready to rent. For the naysayers who think we should have sold it, we would have spent more getting it ready to sell.

Other than that, we’re not doing poorly. Our credit card is still being paid off every month and our mortgage is shrinking. If things continue to go well, we’ll have our truck paid off in a couple of months and the mortgage by mid summer.

Beat the Check

- Image via Wikipedia

Have you ever played a game of “Beat the Check”? Your rent is due tomorrow, but you don’t get paid until Friday, so you write the check today an, on payday, you run to the bank to get your paycheck deposited before it has a chance to clear. To stretch out the time, you write yourself a check from another account to cover the deficit, knowing that will take a few more days to clear. This is called “floating” a check.

Sound familiar?

I think most people who write checks have tried to rush a deposit in before a check clears.

In 2004, the Check 21 act went into effect, which turned the game on its head. This law gave check recipients an option to make a digital copy of a check, slashing processing time. Instead of boxes of checks being transported around the country, the check began getting scanned and instantly transferred, along with all of the encoding necessary to keep the digital checks organized. This dramatically cut the amount of time it took to clear a check. What was once a week was reduced to as little as 48 hours.

Now, as technology improves and banks update their infrastructure to match, the “float” time has been reduced even further. Many banks are using image control systems to instantly convert all incoming checks to digital format. Within a couple of hours, these images can be transmitted to the Federal Reserve, to be transmitted nearly instantly to the issuing bank. If both the issuing and the receiving banks are using modern image control systems, it is impossible to float a check. “Beat the Check” is a thing of the past. It’s like betting on purple at the roulette wheel.

Of course, this doesn’t mean that the funds are instantly available. That would eliminate the banks being able make use of the funds during that time. Don’t expect the banks to make a habit of allowing you the use of your money before the federal regulations demand it.