- RT @Dave_Champion Obama asks DOJ to look at whether AZ immigration law is constitutional. Odd that he never did that with #Healthcare #tcot #

- RT @wilw: You know, kids, when I was your age, the internet was 80 columns wide and built entirely out of text. #

- RT @BudgetsAreSexy: RT @FinanciallyPoor "The real measure of your wealth is how much you'd be worth if you lost all your money." ~ Unknown #

- Official review of the double-down: Unimpressive. Not enough bacon and soggy breading on the chicken. #

- @FARNOOSH Try Ubertwitter. I haven't found a reason to complain. in reply to FARNOOSH #

- Personal inbox zero! #

- Work email inbox zero! #

- StepUp3D: Lame dancing flick using VomitCam instead or choreography. #

- I approve of the Nightmare remake. #Krueger #

ING Rocks

I just got an email from INGDirect. To celebrate Independence Day, they are having a sweet, sweet sale.

You can:

- Open a checking account and get between $50 and $126 for doing so.

- Open a Sharebuilder account and get $76 to start buying stocks.

- Get $1776 knocked off the closing costs of a mortgage.

- Get $76 in a new IRA, to give you a little boost for retirement.

Take advantage of all of that and you’ll get $2054 in cash or discounts.

Seriously, this deal rocks. If you don’t have an INGDirect account, get one. There are no overdraft fees and no monthly fees.

The sale ends tomorrow at midnight, so hurry.

Saturday Roundup

- Image via Wikipedia

This weekend, my wife is spending three days scrapbooking, which makes it a great time to visit my parents and let my niece and nephew entertain my girls for me.

Best Posts

Following your passion doesn’t always pay the bills. Sometimes, there is a tangent that can cover the mortgage while still allowing you to do what you love.

Not everyone enjoys it, but cooking isn’t hard. It’s not even a talent, but a skill that can be learned. Winging it, or creating your own dishes is a talent.

Did you know the spork’s predecessor was invented thousands of years ago?

Here’s a site to help you avoid conflicts with local customs when you travel.

Potluck game night. I think we need to make this happen at our house.

Carnivals I’ve Rocked

6 Ways to Stretch a Meal was an Editor’s Pick in this week’s Festival of Frugality. GenX Finance rocks.

Cheap Drugs – How I Saved $25 in 3 Minutes was included in the Carnival of Personal Finance.

Questions From a Reader was in the Carnival of Money Stories.

Thank you!

If I’ve missed anyone, please let me know.

Consumer Action Handbook

- Image by ivers via Flickr

The Consumer Action Handbook is a book published by the federal government for the express purpose of giving you “the most current information on all your consumer needs.” In short, the Consumer Action Handbook wants to help you with everything that takes your money.

The best part? It’s free.

The book covers topics ranging from banking to health care to cell phones to estate planning. It covers both covering your butt in a transaction and filing a complaint if things go poorly. It explains the options and pitfalls involved in buying, renting, leasing, or fixing a car. You can learn about financial aid for college and maneuvering through an employment agency. And more. So much more.

I’m not sure if you’ve noticed, but I spend quite a bit of time explaining scams and how to avoid them. This book has provided some of the source material for that theme.

It’s 170 pages on not getting screwed, either through fraud or ignorance. Every house should have one. Really, the list of consumer and regulatory agencies alone is worth the price of admission, which–if I wasn’t clear earlier–is $0.

To get yours, go to http://www.consumeraction.gov/caw_orderhandbook.shtml and fill out the form. You can order up to 10 at a time, so pick a few up for your friends and family. They won’t complain, I promise.

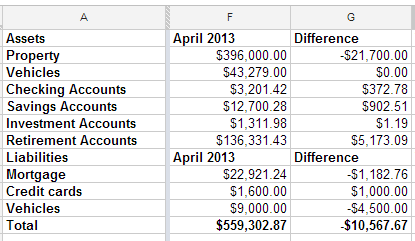

Net Worth Update

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.

Refinancing Your Existing Loan to Purchase An Investment Property

Many people are looking at the housing market slump right now as an investment opportunity. Here are a few of the things that you need to know before getting a new home loan or refinancing your existing loan in order to make that happen.

Amount You Want to Borrow

A lot of borrowers go shopping for real estate and have exactly no idea how much money they can borrow. One of the first questions that you need to ask before going real estate hunting is how much can I borrow. You can ask a bank, lender, or financial institution to give you a ballpark figure of the amount of loan that you would qualify for. This will make it easier for you to narrow down exactly what type of property you can afford and what areas you can concentrate on.

Amount of Interest You Will Pay

Too many people are overly concerned with the purchase price of the home that they are buying. They fail to find out how much interest they will have to pay back to the bank in order to make their home ownership dreams come true. This is where a home loan calculator can be really useful. You can find out exactly how much interest you will repay over a 10, 20, or 30 year loan time period. You can also change the interest rate and down payment amount on those calculators to see if you can secure a lower monthly payment.

Credit Score Needed to Qualify

It doesn’t matter if you are buying a home for the first time or refinancing an existing loan. Your credit score matters. You need to start doing some research now if you want to secure a loan with a really low interest rate. This involves taking the time to see what credit scores traditional lenders are looking for and doing the work necessary to qualify for this loan. Your credit score will make a big difference in determining if an investment property purchase is a profitable endeavor or one that winds up costing you money. It will depend heavily on what kind of loan your credit score allowed you to negotiate.

Make the Choice

Once you know how much you will need and exactly how much you will be paying out over the life of another mortgage, you can decide whether you want to refinance your current home loan to get another one. Adding on another huge debt to an existing one is a big risk. Make sure to think it through fully before jumping in.