There comes a time when it’s too late to tell people how you feel.

There will come a day when the person you mean to talk to won’t be there. Don’t wait for that day.

“There’s always tomorrow” isn’t always true.

The no-pants guide to spending, saving, and thriving in the real world.

There comes a time when it’s too late to tell people how you feel.

There will come a day when the person you mean to talk to won’t be there. Don’t wait for that day.

“There’s always tomorrow” isn’t always true.

I’m so excited. Yesterday, I transferred the final payment for my personal line of credit. This LOC was originally my overdraft protection LOC that had worked it’s way up to $6000 at 21%. Today, it is non-existent.

We started to pay down debt on April 15th, 2009. Since that time, we have paid off $22, 370.70 of our debt. That isn’t $22,370.00 in payments, that is a $22k reduction in our total debt! By my calculations, we have made approximately $28,000 in payments to get that reduction. Next week, we cross the line for 25% of debt eliminated. This is a good day.

Over the last 14 months, we’ve settled into much more responsible spending and saving habits. It no longer feels like we’re sacrificing our lifestyle. We’ve built up a useful emergency fund and set aside money for some things that we know are coming, like braces for my son. In 6 weeks, we are taking our first debt-less vacation.

Now, we start on the long slog to the end. We have 3 debts left to pay: Our last car loan(ever!), one credit card which was an accumulation of pretending we were making progress on our debt by combining many debts onto one card, and finally, our mortgage. The car will be paid by the end of the year. When summer childcare expenses are over, we’ll be making triple payments until it is gone. After that, we have a long, slow couple of years paying off the credit card.

It hasn’t always been easy, but right now, it feels good to look at the progress we’ve made.

Update: This post has been included in the Carnival of Debt Reduction.

This was a guest post I wrote last year to answer the question posed by the Yakezie blog swap, “Name a time you splurged and were glad you did.”

There are so many things that I’ve wanted to spend my money on, and quite a few that I have. Just this week, we went a little nuts when we found out that the owner of the game store near us was retiring and had his entire stock 40% off. Another time, we splurged long-term and bought smartphones, more than doubling our monthly cell phone bill.

This isn’t about those extravagances. This is about a time I splurged and was glad I did. Sure, I enjoy using my cell phone and I will definitely get a lot of use out of our new games, but they aren’t enough to make me really happy.

The splurge that makes me happiest is the vacation we took last year.

Vacations are clearly a luxury. Nonessential. Unnecessary. A splurge.

When we were just a year into our debt repayment, we realized that, not only is debt burnout a problem, but our kids’ childhoods weren’t conveniently pausing themselves while we cut every possible extra expense to get out of debt. No matter how we begged, they insisted on continuing to grow.

Nothing we will do will ever bring back their childhoods once they grow up or—more importantly—their childhood memories. They’ll only be children for eighteen years. That sounds like a long time, but that time flies by so quickly.

We decided it was necessary to reduce our debt repayment and start saving for family vacations.

Last summer, we spent a week in a city a few hours away. This was a week with no internet access, no playdates, no work, and no chores. We hit a number of museums, which went surprisingly well for our small children. Our kids got to climb high over a waterfall and hike miles through the forest. We spent time every day teaching them to swim and play games. Six months later, my two year old still talks about the scenic train ride and my eleven year old still plays poker with us.

We spent a week together, with no distractions and nothing to do but enjoy each other’s company. And we did. The week cost us several extra months of remaining in debt, but it was worth every cent. Memories like we made can’t be bought or faked and can, in fact, be treasured forever.

As I mentioned last month, Crystal and I are in a race to pay off our mortgages. The loser(henceforth known as “Crystal”) has to visit the winner. Now, since–judging by the temperature–Crystal lives in Hell, I think it would be good for her to visit in the winter. There something about the idea of going ice fishing, staring at a hole in the ice while sitting on a 5 gallon bucket, cursing the day I was born.

Today, she threw down the gauntlet again. She has apparently decided that, since her prerequisites are met, she’s going to win. Sure, she’s closed on her house and built her savings back up to $20000, but it doesn’t matter. I’ve sent a small army of arson-ninjas to keep her from getting ahead. They are so small, they can only carry tiny matches and single drops of gasoline, so the damage they can do is tiny, but it will add up. Just a word of advice: if you hire an army of arson-ninjas, go for the upsell and get ninjas that are at least 2 feet tall. Anything less is just inefficient.

When I announced the race last month, my mortgage balance was $26,266.40. Today, it is $25,382.53. In three days, there will be another $880 applied to the principal.

In February, our renters will move in and we’ll conservatively have another $650 to pay. When that starts, our balance should be around $23,000. Adding a portion of the rent payment should mean we pay off the house in May 2014. However, when I bring in our side hustle money, that will bring us back to September 2013.

Crystal’s projected payoff is July 2013, so I’ll have to hustle.

My favorite book series is the Sword of Truth by Terry Goodkind. It’s a good sword-and-sorcery, good-versus-evil fantasy.

But I’m not here to talk about that series. Rather, I’m going to talk about one particular scene in book 6, Faith of the Fallen.

There’s a scene where Richard, the protagonist, ends up in a socialist workers’ paradise, where the government controls distribution and everybody is starving. Jobs are hard to come by, because everything is unionized and unions control access to work. That’s a non-accidental parallel to every country that has embrace socialist principles, or even leans that way. Go open a business with employees in France, I dare you.

So Richard goes out of his way to help someone with no expectation of reward. This person then offers to vouch for him at the union meeting, effectively offering him a job.

This is the conversation that follows:

Nicci shook her head in disgust. “Ordinary people don’t have your luck, Richard. Ordinary people suffer and struggle while your luck gets you into a job.”

“If it was luck,” Richard asked, “then how come my back hurts?”

If it was luck, how come my back hurts?

Seneca, a 2000-year-dead Roman philosopher said, “Luck is where the crossroads of opportunity and preparation meet.”

I won’t lie, I’ve got a pretty cushy job. I make decent money, I work from home, I love my company’s mission, and I kind of fell into the job.

By fell into, I mean:

That’s 25 years and tens of thousands of dollars spent earning my luck. How come my back hurts?

I have a friend on disability. He has a couple of partially-shattered vertebrae in his back, but he keeps pushing off the corrective surgery because the payments would stop after he heals. He refuses to get a regular job, because his payments would stop. He lives on $400 per month and whatever he can hustle for cash, and he will make just that until the day he dies. And he complains about his bad luck.

His back literally hurts, but not metaphorically. His bad luck is the product of deliberately holding himself down to keep that free check flowing.

I have another friend who made some bad decisions young. Some years ago, he decided that was over. He took custody of his kid and started a business that rode the housing bubble. When the bubble popped, so did his business. Instead of whining about his luck, he worked his way into an entry-level banking job.

He put in long (long!) hours, bending over backwards to help his customers and coworkers, and managed a few promotions, far earlier than normal. His coworkers whined about it. He’s so lucky. If it was luck, why does his back hurt?

We make our own luck.

If you bust your ass, working hard and helping people–your coworkers, your customers, your friends, your neighbors–and you are willing to seize an opportunity when it appears, you will get ahead. When you do, the people around you who do the bare minimum, who refuse–or are afraid–to seize an opportunity, who always ask what’s in it for them, they will will whine about your luck.

When they do, you will get to ask, “If it was luck, how come my back hurts?”

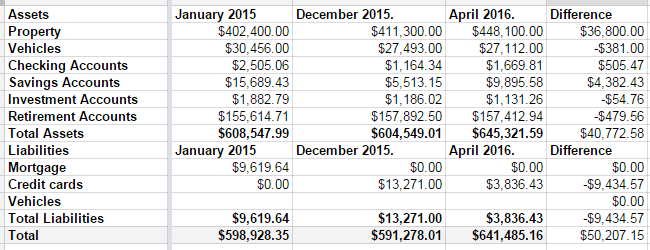

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.