- RT @ScottATaylor: Get a Daily Summary of Your Friends’ Twitter Activity [FREE INVITES] http://bit.ly/4v9o7b #

- Woo! Class is over and the girls are making me cookies. Life is good. #

- RT @susantiner: RT @LenPenzo Tip of the Day: Never, under any circumstances, take a sleeping pill and a laxative on the same night. #

- RT @ScottATaylor: Some of the United States’ most surprising statistics http://ff.im/-cPzMD #

- RT @glassyeyes: 39DollarGlasses extends/EXPANDS disc. to $20/pair for the REST OF THE YEAR! http://is.gd/5lvmLThis is big news! Please RT! #

- @LenPenzo @SusanTiner I couldn’t help it. That kicked over the giggle box. in reply to LenPenzo #

- RT @copyblogger: You’ll never get there, because “there” keeps moving. Appreciate where you’re at, right now. #

- Why am I expected to answer the phone, strictly because it’s ringing? #

- RT: @WellHeeledBlog: Carnival of Personal Finance #235: Cinderella Edition http://bit.ly/7p4GNe #

- 10 Things to do on a Cheap Vacation. https://liverealnow.net/aOEW #

- RT this for chance to win $250 @WiseBread http://bit.ly/4t0sDu #

- [Read more…] about Twitter Weekly Updates for 2009-12-19

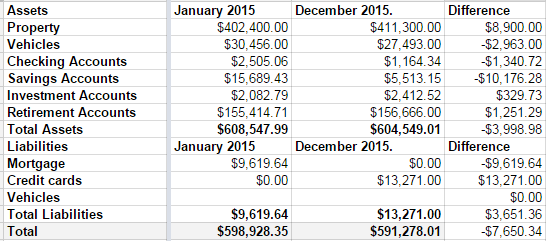

Net Worth and other stuff

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

- We’re going to save for college at a rate we should have started 10 years ago.

- We’re going to max out both of our retirement plans.

- We’re going to take some nicer family vacations.

- We’re going to buy a pony.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

3 Ways to Keep Your Finances Organized

I have 16 personal savings accounts, 3 personal checking accounts, 2 business checking accounts, and 2 business savings accounts. That’s 23 traditional bank accounts, spread across 3 banks. Just talking about that gives my wife a headache.

Every account has a reason. Three of the savings accounts exist just to make the matching checking accounts free. One of the checking accounts handles all of my regular spending that isn’t put on my rewards card. 14 of the savings accounts are CapitalOne 360 accounts that have specific goals attached. A couple of the accounts were opened to boost the sales numbers for a friend who is a banker. Really, it’s almost too much to keep track of. One credit card, 5 checking accounts, 18 savings account, all on 4 websites.

Sometimes, when you extend your bank accounts this far, it gets easy to let it all slip away and lose track of where your money is going. How do I keep track of it all?

1. Simplify

Whoa, you say? Simplify? I don’t simplify the number of accounts I have, I simplify the tracking, or specifically, the need to track.

Twice a month, I have an automated transfer that moves a chunk of money from my main checking account to C1360. I have a series of transfers set up there that move that money around to each of my savings goals. I move $100 to the vacation account, $75 to the braces account, and $10 to the college fund, among all of the other transfers. Doing that eliminates any need to keep track of the transfers, since it is all automated.

Using the same rules, I make every possible payment happen automatically, so I don’t have to worry about paying the gas bill or sending a check to the insurance company.

Simple.

2. Complicate

As you saw in the opening sentence of this post, I also complicate the hell out of my accounts. On the surface, it would seem like that would make it harder to keep track, but in reality, the opposite is true. I have 14 savings accounts at C1360, each for a specific savings goal, like paying my property taxes or going to the to Financial Blogger Conference in October. I can log in to my account and tell at a glance exactly how much money I have for each of my goals. In the account nickname, I include how much each goal is for, so I can easily see if I am on track.

3. Quicken

Everything I do gets set up in Quicken. This makes it easy to track how much actual money I have available. Since I’ve moved my daily expenses to a credit card, I only have about a dozen entries to worry about when I balance my checkbook at the end of the month. At that time, any excess funds get dropped into my debt snowball.

This may all leave me with a needlessly complicated system, but it’s a system that grew slowly to meet my needs and it is working well for me. I spend about 2 hours a month tracking my finances, and can–at any time–tell at a glance exactly how my finances look.

How do you keep your finance organized? Have you tried any unique savings strategies?

Make Extra Money Part 2: Niche Selection

If you want to make money, help someone get healthy, wealthy or laid.

This section was quick.

Seriously, those three topics have been making people rich since the invention of rich. Knowing that isn’t enough. If you want to make some money in the health niche, are you going to help people lose weight, add muscle, relieve stress, or reduce the symptoms of some unpleasant medical condition? Those are called “sub-niches”. (Side question: Viagra is a sub-niche of which topic?)

Still not enough.

If you’re going to offer a product to help lose weight, does it revolve around diet, exercise, or both? For medical conditions, is it a way to soothe eczema, instructions for a diabetic diet, a cure for boils, or help with acne? Those are micro-niches.

That’s where you want to be. The “make money” niche is far too broad for anyone to effectively compete. The “make money online” sub-niche is still crazy. When you get to the “make money buying and selling websites” micro-niche, you’re in a territory that leaves room for competition, without costing thousands of dollars to get involved.

Remember that: The more narrowly you define your niche market, the easier it is to compete. You can take that too far. The “lose weight by eating nothing but onions, alfalfa, and imitation caramel sauce” micro-niche is probably too narrowly defined to have a market worth pursuing. You need a micro-niche with buyers, preferably a lot of them.

Now the hard part.

How do you find a niche with a lot of potential customers? Big companies pay millions of dollars every year to do that kind of market research.

Naturally, I recommend you spend millions of dollars on market research.

No?

Here’s the part where I make this entire series worth every penny you’ve paid. Times 10.

Steal the research.

My favorite source of niche market research to steal is http://www.dummies.com/. Click the link and notice all of the wonderful niches at the top of the page. Jon Wiley & Sons, Inc. spends millions of dollars to know what topics will be good sellers. They’ve been doing this a long time. Trust their work.

You don’t have to concentrate on the topics I’ve helpfully highlighted, but they will make it easier for you. Other niches can be profitable, too.

Golf is a great example. Golfers spend money to play the game. You don’t become a golfer without having some discretionary money to spend on it. I’d recommend against consumer electronics. There is a lot of competition for anything popular, and most of that is available for free. If you choose to promote some high-end gear using your Amazon affiliate link, you’re still only looking at a 3% commission.

I like to stick to topics that people “need” an answer for, and can find that answer in ebook form, since I will be promoting a specific product.

With that in mind, pick a topic, then click one of the links to the actual titles for sale. The “best selling titles” links are a gold mine. You can jump straight to the dummies store, if you’d like.

Of the topics above, here’s how I would narrow it down:

1. Business and Careers. The bestsellers here are Quickbooks and home buying. I’m not interested in either topic, so I’ll go into “More titles”. Here, the “urgent” niches look like job hunting and dealing with horrible coworkers. I’m also going to throw “writing copy” into the list because it’s something I have a hard time with.

2. Health and Fitness. My first thought was to do a site on diabetic cooking, but the cooking niche is too competitive. Childhood obesity, detox diets and back pain remedies strike me as worth pursuing. I’m leaning towards back pain, because I have a bad back. When you’ve thrown your back out, you’ve got nothing to do but lie on the couch and look for ways to make the pain stop. That’s urgency.

3. Personal Finance. The topics that look like good bets are foreclosures and bankruptcies. These are topics that can cost thousands of dollars if you get them wrong. I hate to promote a bankruptcy, but some people are out of choices. Foreclosure defense seems like a good choice. Losing your home comes with a sense of urgency, and helping people stay in their home makes me feel good.

4. Relationships and Family. Of these topics, divorce is probably a good seller. Dating advice definitely is. I’m not going to detail either one of those niches here. Divorce is depressing and sex, while fun, isn’t a topic I’m going to get into here. I try to be family friendly, most of the time. Weddings are great topic. Brides are planning to spend money and there’s no shortage of resources to promote.

So, the niches I’ve chosen are:

- Back pain

- Bankruptcy

- Conflict resolution at work

- Detox diets

- Fat kids

- Foreclosure avoidance

- Job hunting

- Weddings

- Writing copy

I won’t be building 9 niche sites in this series. From here, I’m going to explore effective keywords/search terms and good products to support. There’s no guarantee I’ll find a good product with an affiliate program for a niche I’ve chosen that has keywords that are both highly searched and low competition, so I’m giving myself alternatives.

For those of you following along at home, take some time to find 5-10 niches you’d be willing to promote.

The important things to consider are:

1. Does it make me feel dirty to promote it?

2. Will there be customers willing to spend money on it?

3. Will those customers have an urgent need to solve a problem?

I’ve built sites that ignore #3, and they don’t perform nearly as well as those that consider it. When I do niche sites, I promote a specific product. It’s pure affiliate marketing, so customers willing to spend money are necessarily my target audience.

Avoiding the Downside of Saving

Like all good silver linings, saving often comes with a storm cloud. Too often, people fall into the trap of forgetting to live while they are digging out of debt. Once you get into the habit of spending every spare cent to pay down debt, retirement, or a college fund, it gets easy to ignore the present in favor of the future. The downside–or potential downside–to saving, debt repayment, and frugality is a deferred life. Whether it’s deferred fun, deferred education, or deferred personal development, it can be detrimental to you and your relationships.

My wife and I have had this conversation. We’re in the groove on our debt repayment. We are making excellent progress right now. Since we’ve got it all automated, it leaves us time to plan, dream and consider our options. We’ve been looking at converting a hobby into a business venture. Doing so will involve a $1-2000 investment. If we can make it work, my wife will be able to quit her tolerable, comfortable, soul-sucking job within a couple of years. If we can’t, she will still have moved her hobby into an advanced–and more fun–level. That’s a win either way, but our initial reaction is to postpone. We already know we’ll have to postpone the purchases until we’ve saved for it, because we refuse debt in all forms. Our initial reaction has been to postpone saving, effectively deferring development with long-term potential to improve our lives until our debt is completely gone.

We’ve been discussing this, off and on, for months. We have finally decided to start saving, but only when we have money that is purely extra and we’ve tucked money into all of our other savings goals. It’s not a perfect solution, but it seems to be an acceptable compromise given our situation and values.

Regardless of your situation, it is important to remember not to defer your life while you tackle your debt or savings goals.

Update: This post has been included in the Carnival of Personal Finance.

Make Extra Money, Part 5: Domains and Hosting

In this installment of the Make Extra Money series, I’m going to show you how to pick a domain and a host.

If you remember from the last installment, I’ve decided to promote The Master Wedding Planning Guide. Since then, I have bought the product and read enough to decide that’s it worth promoting. That is the secret to ethical internet product. Never promote a crap product. Now, when I bought the Guide, I used my own affiliate link, so the $37 product will have cost me about $13, once the commission check comes through. You can’t do that just to get a discount because Clickbank has measures in place to ensure that you are actually selling products.

Domain Name

The first thing we need is a domain name.

You can skip this if you want to host on blogger, but I wouldn’t do that, unless $10 is a major financial hardship. I dislike the idea of leaving everything in Google’s hands. Even if you use blogger for hosting(discussed later), pop for the domain name. That way, if you change your mind about hosting, you can move without losing everything.

Where should you go for your domain name? I use NameCheap and GoDaddy. I try to divide my domain names across each of the providers so all of my sites don’t look identical to Google. I may be paranoid, but it works for me.

Before you order, hit Google for a coupon code. Search for “namecheap coupon” or “godaddy coupon” and save some money. GoDaddy is offering $7.49 domains.

How do you pick a domain name?

I try to pick something that matches the product name, or the product’s site. In this case, the product’s site is http://www.masterweddingplanning.com and http://www.masterweddingplanning.net was available, so I grabbed it. I would have been happy with .com, .net, or .org. I won’t touch a .info domain. They are generally cheap, but they cost more to renew and people assume they are spam sites.

If the exact match domain isn’t available, I look for exact matches for the product. If that’s not available, I stick other words at the end that would be attractive to people looking to buy a product.

Acceptable domains would include:

- http://www.masterweddingplanning.org

- http://www.masterweddingplanningreview.com

- http://www.masterweddingplanningguide.net

- http://www.masterweddingplanningreviewed.org

Or nearly anything along those lines. Other good words to attach would be “revealed”, “exposed”, or something similar. Just put yourself in the shoes of a buyer. Would the domain name look like something that could help you decide whether or not to buy a product?

Hosting

Your host is where your website lives. Without a host, you can’t have a website.

When it comes to picking a host, you have some choices to make.

First, do you want to go free or paid? Free sounds great, and if money is tight, it’s not a bad choice, but it does limit your options.

If you’re going free, you’re going with Google’s Blogger. WordPress.com’s hosting eliminates your advertising options, as does almost every other free host. I do know of a couple of free WordPress hosts that will let you run ads and advertising campaigns, but the performance is horrible.

Another problem with using Google is that they can decide your site violates their Terms of Service and shut it down. It shouldn’t happen, but it’s not unheard of with affiliate marketing sites. If you go this route, plan to move to paid hosting when you start making money.

That leaves us with paid hosting.

There are a ton of hosts out there, but only three I have personal experience with.

I won’t use GoDaddy for hosting. I’ve never been happy with their technical support.

I have most of my domains on HostGator (c0upon code: HOSTINGBUDDY). I’m happy with them. Performance is good and the customer service is excellent. Their hosting packages start at $3.96 per month.

I also have a hosting account at HostTheName. I got that because, using coupon code “STARTUPWARRIOR”, hosting prices get down to $1 per month. At $36 for 3 years, I couldn’t turn it down. Initially performance was rocky, but they’ve upgraded and it’s good, now.

Once you’ve created your hosting account, you’ll need to go back to your domain name registrar and set the name servers. At NameCheap, after you log in, you’ll go to Domains > Manage Domains and click on the domain name. From there, click on “Domain Name Server Setup” on the left of the screen and enter the custom name server information listed on your hosting account.

When that’s done, go to your hosting account and add the domain. If you’re creating a new hosting account, this will be your main domain and the hosting company will ask you for the information during setup. If you’re adding this to an existing hosting account, log in, look for “Addon Domains” and follow the prompts.

At this point, you’ve chosen a product to promote and keywords/search terms to go with it. You’ve chosen and registered a domain name and you’ve set up a hosting account to hold your website. Next time, I’ll walk through setting up a WordPress site to make some money.

Any questions?