- Bad. My 3yr old knows how the Nationwide commercial ends…including the agent's name. Too much TV. #

- RT @MoneyCrashers: Money Crashers 2010 New Year Giveaway Bash – $9,100 in Cash and Amazing Prizes http://bt.io/DZMa #

- Watching the horrible offspring of Rube Goldberg and the Grim Reaper: The Final Destination. #

- Here's hoping the franchise is dead: #TheFinalDestination #

- Wow. Win7 has the ability to auto-hibernate in the middle of installing updates. So much for doing that when I leave for the day. #

- This is horribly true: Spending Other People's Money by @thefinancebuff http://is.gd/75Xv2 #

- RT @hughdeburgh: "You can end half your troubles immediately by no longer permitting people to tell you what you want." ~ Vernon Howard #

- RT @BSimple: The most important thing about goals is having one. Geoffry F. Abert #

- RT @fcn: "You have enemies? Good. That means you've stood up for something, sometime in your life." — Winston Churchill #

- RT @FrugalYankee: FRUGAL TIP: Who knew? Cold water & salt will get rid of onion smell on hands. More @ http://bit.ly/WkZsm #

- Please take a moment and vote for me. (4 Ways to Flog the Inner Impulse Shopper) http://su.pr/2flOLY #

- RT @mymoneyshrugged: #SOTU 2011 budget freeze "like announcing a diet after winning a pie-eating contest" (Michael Steel). (via @LesLafave) #

- RT @FrugalBonVivant: $2 – $25 gift certificates from Restaurant.com (promo code BONUS) http://bit.ly/9mMjLR #

- A fully-skilled clone would be helpful this week. #

- @krystalatwork What do you value more, the groom's friendship or the bride's lack of it?Her feelings won't change if you stay home.His might in reply to krystalatwork #

- I ♥ RetailMeNot.com – simply retweet for the chance to win an Apple iPad from @retailmenot – http://bit.ly/retailmenot #

- Did a baseline test for February's 30 Day Project: 20 pushups in a set. Not great, but not terrible. Only need to add 80 to that nxt month #

Fall From Grace

When you accumulate a certain level of debt, it feels like you’re wading through an eyeball-deep pool of poo, dancing on your tiptoes just to keep breathing. Ask me how I really feel.

It shouldn’t be a surprise that I’m in debt. We have gone over this before. The story isn’t one of my proudest, so I’ve never talked much about how it happened.

Our debt was entirely our fault. We messed up and dug our own poo-pool. There were no major medical bills, no extended unemployment, just a strong consumer urge and an apparent need for instant gratification. Delayed gratification wasn’t a skill I’d considered learning. The idea of it was a thoroughly foreign concept. Why wait when every store we visited offered no payments/no interest for a year? We didn’t give much thought to what would happen when the year was up.

We got married young. We bought our house young. We started our family young. We did all of that over the course of two years, well before we were financially ready. Twenty years old, we had excellent credit and gave our credit reports a workout. Credit was so easy to get. By the time I was 22, we had a total credit limit more than twice our annual income. We fought so hard to keep up with the Joneses. A new pickup, a remodel on our house. Within a month of paying off the truck, I got a significant raise and rushed out to buy a new car.

Every penny that hit the table was caught in a net of lifestyle expansion. I was bouncing on my tiptoes.

Four months into my new car payment, I was laid off. There’s me, hoping for a snorkel. A week later, we found out our son was going to be a big brother. Our pool had developed a tide.

We killed the cable and cut back on everything else and…managed. Money was tight, but we got by. I got a new job, but had we learned any lessons? Of course not. We got a satellite dish, started shopping the way we always had. Times were good, and could never be bad. We had such short memories.

Fast forward a couple of years. Baby #3 is on the way while baby #2 is still in diapers. Daycare was about to double. Daddy started to panic. I built a rudimentary budget and realized there was no way to make ends meet. There just wasn’t enough cash coming in to cover expenses. That’s when I made my first frugal decision: I quit smoking. That cut the expenses right to the level of our income. It was tight, but doable.

There was still one serious problem. Neither one of us could control our impulse shopping. For a time, I was getting packages delivered almost every day. It was never anything expensive, but it was always something. Little things add up quickly.

Last spring, I realized we couldn’t keep going like that. I started looking into bankruptcy. Somehow, we managed to toss ourselves into the deep end of the pool. We had near-perfect credit and no way to maintain it.

While researching bankruptcy, I found our life preserver. We put together a budget. We cut and…it hurt. It’s taken a year, but every bill we have is finally being tracked. We have an emergency fund and we are working towards our savings goals. It hasn’t been an easy year, but we are making progress. We’ve eliminated 15% of our debt and opened out budget to include some “blow money” and an occasional date night. We are always looking for ways to decrease our bottom line and increase the top line. Most important, we are actually working together to keep all of our expenses under control, with no hurt feelings when we remind ourselves to stay on track.

We are finally standing flat-footed, head and shoulders above the poo.

Update: This post has been included in the Carnival of Personal Finance.

3 Ways to Keep Your Finances Organized

I have 16 personal savings accounts, 3 personal checking accounts, 2 business checking accounts, and 2 business savings accounts. That’s 23 traditional bank accounts, spread across 3 banks. Just talking about that gives my wife a headache.

Every account has a reason. Three of the savings accounts exist just to make the matching checking accounts free. One of the checking accounts handles all of my regular spending that isn’t put on my rewards card. 14 of the savings accounts are CapitalOne 360 accounts that have specific goals attached. A couple of the accounts were opened to boost the sales numbers for a friend who is a banker. Really, it’s almost too much to keep track of. One credit card, 5 checking accounts, 18 savings account, all on 4 websites.

Sometimes, when you extend your bank accounts this far, it gets easy to let it all slip away and lose track of where your money is going. How do I keep track of it all?

1. Simplify

Whoa, you say? Simplify? I don’t simplify the number of accounts I have, I simplify the tracking, or specifically, the need to track.

Twice a month, I have an automated transfer that moves a chunk of money from my main checking account to C1360. I have a series of transfers set up there that move that money around to each of my savings goals. I move $100 to the vacation account, $75 to the braces account, and $10 to the college fund, among all of the other transfers. Doing that eliminates any need to keep track of the transfers, since it is all automated.

Using the same rules, I make every possible payment happen automatically, so I don’t have to worry about paying the gas bill or sending a check to the insurance company.

Simple.

2. Complicate

As you saw in the opening sentence of this post, I also complicate the hell out of my accounts. On the surface, it would seem like that would make it harder to keep track, but in reality, the opposite is true. I have 14 savings accounts at C1360, each for a specific savings goal, like paying my property taxes or going to the to Financial Blogger Conference in October. I can log in to my account and tell at a glance exactly how much money I have for each of my goals. In the account nickname, I include how much each goal is for, so I can easily see if I am on track.

3. Quicken

Everything I do gets set up in Quicken. This makes it easy to track how much actual money I have available. Since I’ve moved my daily expenses to a credit card, I only have about a dozen entries to worry about when I balance my checkbook at the end of the month. At that time, any excess funds get dropped into my debt snowball.

This may all leave me with a needlessly complicated system, but it’s a system that grew slowly to meet my needs and it is working well for me. I spend about 2 hours a month tracking my finances, and can–at any time–tell at a glance exactly how my finances look.

How do you keep your finance organized? Have you tried any unique savings strategies?

Make Extra Money Part 4: Keyword Research

In this installment of the Make Extra Money series, I’m going to show you how I do keyword research.

Properly done–unless you get lucky–this is the single most time-consuming part of making a niche site. If you aren’t targeting search terms that people use, you are wasting your time. If you are targeting terms that everybody else is targeting, it will take forever to get to the top of the search results.

Spend the extra time now to do proper keyword research. It will save you a ton of time and hassle later. This is time well-spent.

If you remember from the last installment, when we researched products to promote, we narrowed our choices down to a few products.

What I’ve done is create a spreadsheet to score the products. You can see the spreadsheet here. I’ll explain the columns as we populate them.

The first column contains the name of the product. Easy. We’ve got 10 products. I’m going to walk through scoring 1 product, then, through the magic of the internet, I’ll populate the rest, and you’ll get to see the results instantly. Wow.

The second column is the global search volume for the exact search term. I base my product niche sites primarily on the demand for a given product. Everything else is a secondary consideration.

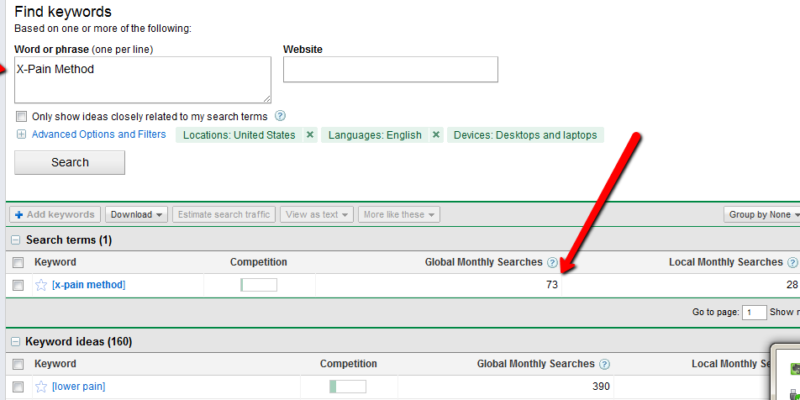

To find the demand for a product, go to the Google Adwords Keyword Tool. In the “word or phrase” box, enter your product name, exactly. In this case, it’s “X-Pain Method”. When the search results come up, change the match type to “Exact”. You should have something like this:

Enter the global search volume in column 2. In this case, it’s 73. Keep this window open, because we’ll be coming back to it.

Column 3 is the search competition. Go to google and enter your product name, in quotes. In this case, “X-Pain Method”. Put the total number of search results in column 3: 223000.

Column 4 is the search competition, but only what appears in a page’s title. Your search query is intitle:”X-Pain Method”, which yields 4400 results.

The next column is for the average PageRank of the first page of search results. For this, I use Traffic Travis. I use the 4th edition, which is paid software, but you can get the free version of version 3, instead. I’ll use version 3 for this example. Open the software and click on “SEO Analysis” on the bottom left of the screen. Put your search term (“X-Pain Method”) in the “phrase to analyze” and set the “Analyze Top” to 10, then hit “Analyze”. When it’s done running, just add up all of the PRs and divide by 10. Ignore Travis’s difficulty rating.

Now, for the rest of the columns, we’re going to look at the keyword tool again. We’re going to pick 3 alternate search terms. Here are the criteria:

- At least 1000 global monthly searches. We want terms that people are searching for.

- Competition bar at medium or less. This bar is just a rough guess on competition, so it’s really an arbitrary exclusion factor, but it helps narrow down the choices.

- A “buying” keyword is preferred, but not necessary. This is a term that indicates people are looking to spend money. “Back pain doctor” is a buying keyword, but it’s not an indicator that someone wants to buy a product, so we’ll skip it. A buying keyword isn’t absolutely necessary, because these will also be the terms we’ll use to generate content later.

- It has to be related to our product.

Once we pick the keywords, we’ll throw them into google to get the competition, just like we did to populate column 2.

“Exercises for back pain” has medium competition and 1900 monthly searches. It also has an estimated cost-per-click of $3.02, which means people are paying for this.

“Lower back pain exercises” has 6600 searches and medium competition. It’s actually on the lower end of medium, so it looks really promising.

“Lower back” has 4400 searches and low competition, with a CPC of $6.24. This should be a good one. Scratch that. It has 40 million search results, but only 4400 searches. That’s a lot of competition for a small market.

Instead, I’m going to search for “cure back pain” in the keyword tool and see what I get. “Upper back pain” is better. Low competition, 18000 searches each month, and only 2000000 competing search results. Now, I’ll score it.

You really want at least 500 searches per month for the product name. More than 2500 is better. I’m going to assign 1 point per 500 monthly searches.

You also want a lower number of search results. Less than 10,000 is ideal. Less than 100,000 is still decent. More than 250,000, I’d walk. So, under 10,000 gets 5 points. Under 50,001 gets 4. Under 100,001 gets 3. Under 200,001 gets 2. Under 250,001 gets 1. Any higher gets 0.

The ideal intitle search will have less than 2000 results. More than 100,000 is too time-consuming to deal with. 0-2000: 5 points; 2001-10,000: 4 points; 10001-25000: 3 points; 25001-50000: 2 points; 50001 to 100000: 1 point.

The perfect product will have the first page of search result all with a PageRank of 0. That’s a 5 point product. I’ll knock off half a point for every point of average PR.

The related terms are more relaxed. They are what’s known as “Latent Semantic Indexing” (LSI) terms. We will be creating articles to match those search terms, mostly to make our niche site look as natural and real as possible. Any actual traffic those pages drive is just gravy. Points for the related searches start at 10 and get 1 point knocked off for each 3 million results. We’ll be treating the 3 terms as one for this score.

That gives us a perfect score of about 25. There’s no actual upper limit, since the score for the search volume has no upper limit. X-Pain Method scored 18.22.

Now, excuse me a moment while I score the rest.

I’m back. Did you miss me?

I’ve finished scoring each of the products and sorted the results by score. The clear winner is the back pain product, but the lack of searches bothers me. The wedding guide looks much nicer, especially if I target the phrase “wedding planning guide” during the SEO phase of the project. That change alone brings the score almost to first place.

Frankly, I’d take either 2nd or 3rd place over the back pain product. The bare numbers don’t support it, but my judgement tells me they are better products to promote.

There is one final step before deciding on the product. I have to buy it. I can’t review the product without seeing it and I can’t promote it without approving of it.

That’s the secret to ethical niche marketing, you know. Only promote good products that you’ve personally read, watched, or used.

Negotiating 101

In the US, haggling is something that makes a lot of people twitch and wet their pants. It’s too hard/scary/intimidating, so most of us just take whatever price is offered, with a smile.

The truth is, you can negotiate in almost any situation. Sure, big-box retailers with low-price goods–like Walmart or a grocery store–aren’t going to go for it, but a lot of other businesses will. Did you know you can haggle at Best Buy? It’s true, but only on the bigger ticket items.

You can also easily negotiate at place like these:

- Credit card interest rates and annual fees

- Luxury utilities like cable

- Rent

- Hotel rates

- Airline tickets

- Gym memberships

“Great”, you say. “Anyone can do it?”, you say. “But how, jerk?”

No need to call names, I’m getting to that part.

I am about to share the First Secret Lesson of Negotiating. This secret has been passed down from father to son among the celibate Shaolin monks for generations. Breaking the code of secrecy may be putting my life in danger, but I’m willing to do that for you, no matter the risk.

I rock like that.

Are you ready to be initiated into the secrets of the Ancient Masters? When our first abbot, Buddhabhadra, first wandered into the Northern Wei Dynasty branch of Best Buy in 477 A.D., he discovered the phrase most likely to break price barriers.

Are you ready, Grasshopper? This is the “Wax on, wax off” of effective negotiation.

When you are given a price, no matter what it is, say “Is that the best you can do?”

“This T.V. costs $7495.” “Is that the best you can do?”

“That comes to $56.95.” “Is that the best you can do?”

“$149,499 for the Ferrari.” “Is that the best you can do?”

“$12,000 for the kidney.” “Is that the best you can do?”

“Only $8.50 for this set of 10 tupperware lids that have been warped in the dishwasher.” “Is that the best you can do?”

“$50 an hour, honey.” “Is that the best you can do?”

“The salary for this position is $50,000 per year.” “Is that the best you can do?”

It is magical, it’s easy to remember, and it’s low stress. This is a non-combative question. The worst possible scenario involves the other side saying, “Yes, that is the best I can do.” No sweat.

Negotiating Lesson 101.2:

After saying “Is that the best you can do?”, shut up. The other party gets to be the next person to say something.

Go out and practice this over the weekend. Master the First Secret Lesson of Negotiating. I’ll be fighting off Shaolin ninjas for sharing the ancient secrets.

Avoiding the Downside of Saving

Like all good silver linings, saving often comes with a storm cloud. Too often, people fall into the trap of forgetting to live while they are digging out of debt. Once you get into the habit of spending every spare cent to pay down debt, retirement, or a college fund, it gets easy to ignore the present in favor of the future. The downside–or potential downside–to saving, debt repayment, and frugality is a deferred life. Whether it’s deferred fun, deferred education, or deferred personal development, it can be detrimental to you and your relationships.

My wife and I have had this conversation. We’re in the groove on our debt repayment. We are making excellent progress right now. Since we’ve got it all automated, it leaves us time to plan, dream and consider our options. We’ve been looking at converting a hobby into a business venture. Doing so will involve a $1-2000 investment. If we can make it work, my wife will be able to quit her tolerable, comfortable, soul-sucking job within a couple of years. If we can’t, she will still have moved her hobby into an advanced–and more fun–level. That’s a win either way, but our initial reaction is to postpone. We already know we’ll have to postpone the purchases until we’ve saved for it, because we refuse debt in all forms. Our initial reaction has been to postpone saving, effectively deferring development with long-term potential to improve our lives until our debt is completely gone.

We’ve been discussing this, off and on, for months. We have finally decided to start saving, but only when we have money that is purely extra and we’ve tucked money into all of our other savings goals. It’s not a perfect solution, but it seems to be an acceptable compromise given our situation and values.

Regardless of your situation, it is important to remember not to defer your life while you tackle your debt or savings goals.

Update: This post has been included in the Carnival of Personal Finance.