- Getting ready to go build a rain gauge at home depot with the kids. #

- RT @hughdeburgh: "Having children makes you no more a parent than having a piano makes you a pianist." ~ Michael Levine #

- RT @wisebread: Wow! Major food recall that touches so many pantry items. Check your cupboards NOW! http://bit.ly/c5wJh6 #

- Baby just said "coffin" for the first time. #feelingaddams #

- @TheLeanTimes I have an awesome recipe for pizza dough…at home. We make it once per week. I'll share later. in reply to TheLeanTimes #

- RT @bargainr: 9 minute, well-reasoned video on why we should repeal marijuana prohibition by Judge Jim Gray http://bit.ly/cKNYkQ plz watch #

- RT @jdroth: Brilliant post from Trent at The Simple Dollar: http://bit.ly/c6BWMs — All about dreams and why we don't pursue them. #

- Pizza dough: add garlic powder and Ital. Seasoning http://tweetphoto.com/13861829 #

- @TheLeanTimes: Pizza dough: add lots of garlic powder and Ital. Seasoning to this: http://tweetphoto.com/13861829 #

- RT @flexo: "Genesis. Exorcist. Leviathan. Deu… The Right Thing…" #

- @TheLeanTimes Once, for at least 3 hours. Knead it hard and use more garlic powder tha you think you need. 🙂 in reply to TheLeanTimes #

- Google is now hosting Popular Science archives. http://su.pr/1bMs77 #

- RT @wisebread 6 Slick Tools to Save Money on Car Repairs http://bit.ly/cUbjZG #

- @BudgetsAreSexy I filed federal last week, haven't bothered filing state, yet. Guess which one is paying me and which one wants more money. in reply to BudgetsAreSexy #

- RT @ChristianPF is giving away a Lifetime Membership to Dave Ramsey’s Financial Peace University! RT to enter to win… http://su.pr/2lEXIT #

- RT @MoneyCrashers: 4 Reasons To Choose Community College Out Of High School. http://ow.ly/16MoNX #

- RT @hughdeburgh:"When it comes to a happy marriage,sex is cornerstone content.Its what separates spouses from friends." SimpleMarriage.net #

- RT @tferriss: So true. "Nearly all men can stand adversity, but if you want to test a man's character, give him power." – Abraham Lincoln #

- RT @hughdeburgh: "The most important thing that parents can teach their children is how to get along without them." ~ Frank A. Clark #

Should Pupils Focus on Personal Finance?

When I was younger, my dad was always trying to teach me the value of money but he never really succeeded and it took a series of monetary mishaps before I even started to learn any of the lessons that he had been trying to teach me!

Once I realized that I had been horribly mismanaging my finances, a painful lesson to learn, especially on the back of a redundancy, I began to do some research to find out exactly where I had gone wrong and what I could do to put things right.

It was at this point that it occurred to me that I knew absolutely nothing about personal finance and I couldn’t tell an ISA from a current account.

I also began to wonder if I had been taught these lessons at an early age then would I have made better financial decisions once I started earning?

For example, my outlook on personal finance was all about borrowing and not saving and I had no idea what my credit score was or how it was calculated.

Had I known that it could be affected by simply being close to the limits on my current lending streams or by applying for more credit then I may not have been so quick to spend on credit cards.

Although this was not a problem during the credit boom, when offers of guaranteed credit seemed to drop through my door on a daily basis, it has become something of an issue since the credit crunch.

Of course, just knowing the pitfalls of financial mismanagement is no guarantee that I would have done things any differently but it certainly would have made me think about the decisions I was making and the impact they would have in the long run.

All of which led me wonder whether should schools give students (or pupils if you’re in the UK) lessons in personal finance.

I think it would be a great idea as this would be something that everyone, no matter what their level of academic ability, could take with them into the real world.

And it could be the case that a school in the US is one step ahead of the rest as they already have money management lessons as part of the curriculum.

Burbank High School in Sacramento is offering students lessons in personal finance as part of National Financial Literacy Month in an effort to raise awareness of the importance of good practice in personal finance.

The lessons covered personal finance topics such as budgeting, saving and needs vs. wants and placed them into real life scenarios that would resonate with the students, such as estimating how much the senior prom will cost and ways to save and pay for it.

Students were also encouraged to put a portion of any weekly earnings or allowance into a savings account to teach them the importance of saving for the future from an early age.

I think that these were the values that my dad was trying to instill in me from an early age but I failed to take any notice.

I now have two sons that I have to try and keep from making the same mistakes that I made, so any help I can get will be greatly appreciated…here’s to future school pupils focusing on personal finance!

Article written by Moneysupermarket.com

Paying for Rat

I’m cheap. I don’t even consider myself to be frugal. I’m cheap. A few days ago, I spent my entire year’s Halloween budget–on November 1st–so I could store my new treasures

for an entire year before using them, just to save $145.

However, there are some things that just aren’t worth going cheap.

When I first moved out on my own, a good friend walked me through the mistake of buying cheap cheese. A slice of the generic oil-and-water that some stores pass off as cheese will not cure a sandwich made from Grade D bologna.

That advice got me through some less horrible meals when I was younger.

Now, I’ve expanded the crappy cheese rule to extend to any meal I pay someone else to prepare. While I do occasionally hit a fast food restaurant when I’m traveling, I almost never do so any other time. I enjoy sitting down for a nice meal in a nice atmosphere while friendly people cater to my every whim. Well, almost every whim.

I’m not saying I go to $100 per plate steak houses every week, but I’m certainly not afraid to drop $20-$30 per meal.

My reasoning is simple: anything I can buy at a fast food restaurant or a cheap restaurant, I can make better at home for less. Why would I pay good money to sit at a sticky table and eat food that won’t let me forget it for 3 days?

If I’m going to spend the money, I’m going to eat something I either can’t make at home, or can’t make as well. Chinese food is one example. I can make it at home, but I don’t stock the ingredients, and I don’t enjoy the preparation, so I go out for it. Cheap Chinese food tends to be worse than anything else I’ve eaten, so I spring for good food. Cheap rat isn’t good rat.

How about you? What are you willing to pay full price for?

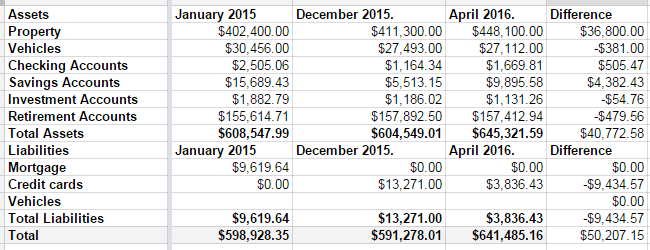

Net Worth, April 2016

Last year wasn’t a good year for my net worth. It came with a $7000 drop.

Q1 2016, however, was a great quarter.

In December, we had $13,271 in credit card debt. At the time I took this screenshot, it was down to $3836.43. As of this moment, it’s down to $2640.91. If things go as expected this week, I should wake up on Friday to a paid-off credit card. I had to raid some of our savings accounts to make it happen, but it’s happening. Some of it was a tax refund, some of it was the fact that my mortgage payment went away in December.

That’s seven years of hard work, almost to the day. Seven years ago, I was researching bankruptcy, and stumbled across Dave Ramsey. Seven years ago, we were drowning in debt.

Next week, we’re free. No more debt, hanging over our heads. We’re free to take vacations. We’re free to finally save for college, when my son is 16, and stand a chance of being able to pay for it for him. We’re free to do…whatever we want to do. Our monthly nut after the debt is paid–only in fall/winter/spring when my wife is working–is roughly 1/3 of our take-home pay.

That’s how hard we’ve cut to make sure we can pay our bills and make debt die. We do have some things that would be considered extravagant. We’re not savages. But my car is 10 years old. My wife’s is 7. My motorcycles are 35 and 30; one of them was purchased before we cared about our debt.

Back to the net worth….

The biggest change came from our property values, which sucks. That was $36,000 of the difference, which comes with the painful tax bump to go with it. A large chunk of the savings increase was the money we set aside every month to cover the property tax bill, and that will go away next month.

Still, $641,000 dollars is a long way from nothing. I’m pretty happy.

More Debt

Even though we just paid off our credit cards in August and have started competing to pay off our mortgage, we opened a new debt account on Monday.

We’ve been shopping for a new(to us) car for a while. Simply put, we’ve outgrown our current vehicles.

As I said last week, these are our needs:

- We have 5 people in our family. My 13-year-old son is bordering on 6 feet tall and shows no sign of not growing.

- Every weekend, we have at least 1 extra kid, sometimes 2.

- We still have a giant(24 foot) boat that we won’t be selling until spring.

- My wife wants to lease a couple of ponies next summer, which will mean a horse trailer to haul them in.

We were looking for a GMC Acadia, which would meet our needs, but after talking to my brother–an Acadia owner–and the dealer, we decided it wouldn’t be the best fit. It would be marginal for towing the horses and the back row of the older models isn’t as roomy as the new one I sat in.

Saturday, we went to test drive an Acadia, which is where we had the conversation with the dealership. We ended up test-driving a Chevy Tahoe instead of the Acadia. With the options and mileage, it bluebooks for $27531, but they were using it as an online price leader and had it priced at $25000. Maybe I missed something, but the thing ran well, handled great, and the engine sounded good. As a way to get people on the lot, it worked.

Our plan was to put $5000 down, and see about trading in our Dodge Caliber and Ford F150. We brought the Caliber with us. Its bluebook value is $9,969. They offered us $5500, so we went home.

Sunday, we decided to sell the car and truck ourselves. We texted the salesman and offered $24,500. He accepted, we got a new truck that will fit our family and our needs.

With taxes, fees, and our down payment, we now have a car loan for $21564. Our plan is to sell the Caliber for $9500 and the F150 for $6800. That will leave $5354. We have a beneficiary IRA that has to be cashed out relatively soon, so we’re planning to do that early in January to push the tax burden to next year, which will end the loan.

Effectively, we’re paying about $300 in interest to give us a chance to move our assets around to take advantage of an SUV meeting our needs for $3000 under blue book. Yes, we could have waited until the assets were ready, but this truck wouldn’t have been there, so we jumped on it.

John Kerry’s Wife Hospitalized: Can You Afford Health Insurance?

Even as a growing number of analysts are questioning the details of Obamacare, the sudden hospitalization of Teresa Heinz Kerry, the wife of former senator and current U.S. Secretary of State John Kerry, provides additional fodder to the ongoing healthcare debate.

Heinz, who is 74 years old, is the heir to the Heinz ketchup fortune. She is the widow of former Senator John Heinz, who was killed in 1991 in an aviation accident. Her marriage to Kerry in 1995 occurred when he was the senator from Massachusetts. Heinz was hospitalized on Sunday and is reported to be in critical condition after being flown to Massachusetts General Hospital in Boston.

Heinz was treated for breast cancer in December 2009 and went through two operations for lumpectomies. It is not known what specific health issues resulted in the current hospitalization. However, sources indicated that there was concern over the return of the cancer.

Regardless of the source of the current illness, it is taken for granted that Heinz will receive the very best of medical care, with cost being of no concern to treatments pursued. In the earlier process of treating her cancer, numerous doctors at the nation’s finest medical facilities were consulted. The issue of Heinz not having to worry about the costs of her care is the central theme of many who criticize our nation’s health care system.

For the millions of Americans who live daily without health insurance or any form of coverage, there is a constant concern over how they would deal with a medical emergency. These individuals know that they are one accident or serious illness away from devastating financial hardship. In fact, the single biggest reason for bankruptcy in the U.S. today is medical bills. According to the latest studies, the average hospital stay billed out at $15, 700, with an average daily cost of nearly $4,000.

These costs are onerous because so many people today find health insurance increasingly unaffordable. While the political debate over the current healthcare reform continues, there is one simple fact. That reality is that the annual cost of private health insurance, already out of the reach of many, has risen by as much as 50 percent in the last two years. Many plans for a family of four are now over $15,000 and it is predicted that a bronze plan under the implemented Obamacare will exceed $20,000 for that same family.

All of this brings us back to the hospitalization of Heinz. The reality we live in today means that many people diagnosed with cancer or other similar diseases have little hope of receiving the treatment or care that the wealthy can afford. Even with quality health care insurance, the co-pays and other costs create burdens that many cannot carry.

There are no simple or ready solutions to this situation. The morality of one patient dying because chemotherapy is too expensive while one with a large bank account survives is an issue that will see intensified debate in the coming months and years. Regardless of what caused the current hospitalization, Heinz is one of the lucky ones who will have superb medical care without financial considerations.