- RT @Dave_Champion Obama asks DOJ to look at whether AZ immigration law is constitutional. Odd that he never did that with #Healthcare #tcot #

- RT @wilw: You know, kids, when I was your age, the internet was 80 columns wide and built entirely out of text. #

- RT @BudgetsAreSexy: RT @FinanciallyPoor "The real measure of your wealth is how much you'd be worth if you lost all your money." ~ Unknown #

- Official review of the double-down: Unimpressive. Not enough bacon and soggy breading on the chicken. #

- @FARNOOSH Try Ubertwitter. I haven't found a reason to complain. in reply to FARNOOSH #

- Personal inbox zero! #

- Work email inbox zero! #

- StepUp3D: Lame dancing flick using VomitCam instead or choreography. #

- I approve of the Nightmare remake. #Krueger #

Perez Hilton: The Cost of Living in New York City

Ahhh, New York City. The Mecca of all that is glamorous, rich, luxurious and exciting. To some, the good life. So, you’re ready to pack your bags and head for the big city? Slow down there, big dreamer. The cost of

EVERYTHING in the city is higher than the national average, meaning your 70K per year needs to be 166K in New York City to keep your current lifestyle. Let’s talk about the basics here: lodging, food and entertainment:

Apartments in New York City are insanely high. Like, find a roommate and hang a curtain down the center of your one bedroom to make two bedrooms high. The average Manhattan apartment costs $3,973.00 per month, almost $2,800.00 more than rentals elsewhere in the country. Looking to buy? The average sale price of a home in Manhattan is $1.46 million, compared to under $230,000.00 elsewhere. I suppose the good news is that in New York City, you don’t have to own your home for an elite status, as is required in other areas. Considering a family of four making less than $68,700 per year qualifies for public housing in New York City – you better be making bank if you plan to check your mailbox next to any celebrities.

If rent has not broken you, you must also eat! I mean, you won’t be eating MUCH after paying rent, but you will need a nibble here and there. It will come as no surprise that the restaurants in New York City are pricey. Celebrity favorites such as the Four Seasons, Le Cirque and Nobu are over $50.00 PER PERSON. I just choked on my Diet Coke. Eateries such as McDonald’s and local Mexican restaurants are abundant, but they too are higher priced than elsewhere. Your best bet? Learn to cook. Eat leftovers. Use coupons. Pair those coupons with sale items. Find a generous and rich companion. Skip meals.

As far as entertainment goes, I’m afraid at this point, your only entertainment will be browsing the web for supplementary forms of income. Seriously, unless you are in the 1%, utilize the many forms of free entertainment that New York City has to offer. A jog through Central Park, window shopping or a walk through the city all offer ample opportunity for fun free of charge. Sadly, Broadway plays and designer shopping must be left to the rich and famous.

In conclusion, one can lead a good, but not extravagant, life in New York City on a normal income. Be prepared to work hard, save hard and live frugally. Unless you’re living on money that is coming from an investment or dividend, you shouldn’t expect anything more. Listen, New York City is exciting, good grief, it’s the “city that never sleeps,” but it isn’t cheap. Of course, the people I know who have lived there for a short stint of time had little money and have since moved on – with no regrets and countless memories from that season of life.

Related articles

I Smell a Scam

I hate scammers. Whether it’s the garage-sale shoplifter, telemarketing “charities” with 99% overhead, 3-card-monte

dealers, or the guy who begs Grandma for cash every week, they all need to be strung up. Since vigilante justice is generally illegal and occasionally immoral, it’s best to just avoid the problems from the start. Here are some scams to watch out for.

Pyramid Scams – All of the little parties people throw to earn free items at the expense of their friends are pyramid schemes. Most of those are legitimate money-sinks. A few, however, exist solely to get their “consultants” to bring in more consultants. The sales aren’t the actual way to make money. If you don’t have anyone “downstream” you won’t make any money. If the focus isn’t on selling an actual product or service, but is instead on bringing in people under you, you have entered the world of pyramid scams. Generally illegal and always immoral. Don’t sign up and, if you do, don’t ask me to participate.

Advance Fees and Expensive Prizes – If you win a contest and you are expected to send money to claim your prize, it is a scam. You don’t have to pay sales tax in advance. You don’t have to pay transfer fees. Real prizes are delivered free, accompanied by a 1099, because prizes are income. No prize requires pre-payment. No loan service requires “finder’s fees”. If it doesn’t sound right, don’t pay it and certainly don’t give your bank information to anyone you can’t verify.

Work at Home – The most common work-at-home job I’ve found is stuffing envelopes. You see the signs on telephone poles all over the city. “Make $10/hour stuffing envelopes from the comfort of your own home! Just send $50 to….” When you get the instructions, you are told to hand up signs telling people to send you $50 for instructions on how to make $10/hour stuffing envelopes. Everybody is feeding off of everybody else.

Charity – Never give money to a charity over the phone. Always take the time to verify where you are sending your money. Some freak may call to tug on your heartstrings with a sob story, but you don’t have to give them money. At least ask them to send it in writing so you can do some checking, first.

Phishing – Simply put, don’t click on any link in any email, unless you know where it is going. If it is a link to a financial institution, go enter the address into the address bar yourself. If you find yourself on a site you don’t recognize, don’t give them your personal information and don’t ever reuse your usernames and passwords. If you do, one bad site could get access to everything you do online.

[ad name=”inlineleft”]Foreign Lottery – To be clear, Spain did not just hold a international lottery and randomly draw your email address. No lottery in the world works that way. If you didn’t enter the lottery while you were in Spain, you aren’t going to win it. The scam is that you need to provide your bank information, including a number of release forms so the scammers can transfer money to you. In reality, you are signing over control of your account and will be wiped out.

Nigerian/419 Emails – Ex-Prince WhateverHisNameIs wants your help to get his fortune out of WhereverHeIsFrom. The New Widow Ima F. Raud has an inheritence that she won’t live long enough to spend. They’ve both been given your name as a trustworthy person to handle the transactions in exchange for a mere $10 million. What friends do you have that would make this seem legitimate? Once again, they will get your bank information and take your money. At a minimum, they will try to get you to pay a few thousand dollars for “Transfer fees”. Don’t do it.

Overpayment by Wire – I had this one attempted on my last week. You sell something online. A potential buyer agrees to purchase the item, sight-unseen. They’ll send a cashier’s check and, after it clears, one of their agents will pick it up. Unfortunately, the buyer’s secretary screwed up and added a zero to the check. Would you mind wiring the overpayment back, minus a small fee for the hassle? The check is bogus and there is no way to verify it. You’ll deposit the check and it will be assumed to be real. The bank will make the funds available well before it comes back as fraud. You’ll see the available funds and send the money by non-refundable Western Union and some thug in Nigeria gets a new iPhone.

Foreclosure Scams – Some scammers try to prey on the vulnerable because they are, well, vulnerable. If you are facing foreclosure, be very careful about where you turn for help. One scam is to get you to sign over your home “temporarily” to clear the title. That doesn’t work, but you won’t find that out until you are handed an eviction notice and told you still owe the money.

Stranded Friends – You get an email from a friend saying he’s in London/Moscow/Sydney/Wherever, and he’s been mugged. He’s got nothing and needs $2500 to get home. Can you help? Do you really have friends close enough to ask for a $2500 international bailout, but not so close they tell you about the vacation ahead of time? Would they really be too timid to call you collect instead of begging for change to use an internet cafe?

5 Ds of Identity Theft

Identity theft is, at its most basic level, the act of using someone else’s identity or credit without permission. From a stolen credit card to a forged phone bill in Moscow, it all involves your good money paying for the bad habits of another. Thankfully, there are ways to reduce the odds of having your identity stolen. LTC David Grossman reviews the “5 Ds of Survival” in his seminars and books. Today, I bring you the 5 Ds of Identity Theft.

In the words of the master, “Denial has no survival value.” Denying the possibility of identity theft will not keep it from happening. You have to take steps to keep yourself safe. “It could never happen to me” is not a valid defense mechanism in any situation, financial or otherwise.

Deterrence means keeping the information away from identity thieves. The harder it is for the criminals to get your information, the more likely it is that they will move on to an easier target. And yes, a kid stealing Grandma’s credit card is a criminal and needs to be treated as such.

- Some people use a shredder, but not me. I have a fire pit that catches all of my personal documents. I’d like to see an thief get my social security number from the ashes in the bottom of the pit.

- Don’t carry your social security card. If you lose your wallet, your driver’s license and social security card contain all of the information needed to steal your identity. Keep it locked up at home and don’t give the number out unless absolutely necessary.

- Don’t use stupid passwords. Anything listed on yourFacebook profile or otherwise available on Google in association with your name is a stupid password. Don’t make life easy for the people looking to screw you. Your birthdate, maiden name, and “password” all qualify as stupid passwords. Use KeePass to securely generate and store your passwords.

- Lock up your personal information. I throw two large parties every year. Purses and wallets get stored in a locked bedroom, so nobody can grab them. That was a lesson learned the hard way. If there’s someone in your home you don’t trust absolutely, lock up anything that can be used against you.

- Don’t release personal information to anyone, for any reason, unless you have initiated the contact. Don’t give a credit card number to a telemarketer. Don’t give a spammer your personal information. It’s your privacy, use it.

- Don’t click anything in an email. If it’s a company you have a relationship with, type the address in your browser by hand.

Detection is up to you. Some credit card companies will alert you to suspicious purchases, but you can’t rely on it. I was once called because I went to the gas station and Best Buy, which is apparently a common pattern for a stolen credit card.

- Examine your credit card statements. If there’s a purchase you don’t recognize, find out what it is.

- Watch for bills to arrive as expected. You do know when you pay the gas bill every month, right?

- Watch for unexpected bills to arrive. If you get a statement for a credit card you don’t have, it’s a problem.

- Check your credit report three times per year. AnnualCreditReport.com will let you see each of the three major credit reports each year. Space them out so you see your report every 4 months.

Defending your identity happens after you’ve detected a theft. This involves getting your credit and sometimes, your money, back.

- File a fraud report with the credit bureaus. This will force potential creditor to follow certain procedures before opening new credit accounts for your identity, including calling your cell phone, if you choose. Stop the identity theft in its tracks.

- Close the fraudulent accounts. Don’t leave them open for abuse.

- File a police report and report the fraud to the FTC at ftc.gov/idtheft . This may or may not help catch the criminal, but without it, there will never be a punishment. Make stealing your identity an expensive proposition. Hopefully, 1o years of his life will be wasted in jail in return for the theft.

Destroy. Unfortunately, fraud and identity theft are not yet capital crimes. Maybe someday.

Deter, detect, defend. These are the secrets to avoiding, and recovering from, identity theft.

My Investment Portfolio

I’m not a financial adviser. I haven’t taken any of the classes or certifications that allow me to give investment advice. Please don’t take this post as advice.

This is me, sharing what I have chosen to invest in. These investments are scattered across a few different IRAs and brokerage accounts. Copy me at your own risk.

BAC – Bank of America: I bought this low. When any major bank is low, it’s time to buy. I bought in stages starting at about $5 per share. What I’ve got now has given me a 57% return.

CVS – CVS Caremark: I bought this on the advice of a friend. It’s shown a 6% return over the past few months.

IAU & GLD – Gold ETFs: I wanted a way to get some precious metals into my IRA, so I bought a gold fund. It’s down 7%, but I’m confident it’s going to come back.

MSFT – Microsoft: This is one of the first stocks I bought with my 401k 10 years ago. It’s up about 5% since I rolled it into my current IRA.

PAYX -Paychex Inc: I hate payday loans, but a friend recommended this stock and it has given me a 10% return.

SIRI – Another recommendation from a different friend. I don’t think it will ever hit the moon, but you won’t see me complain about the 60% return, either.

SLV – Silver ETF: Another precious metals venture. It’s down 3% overall, but that’s varying day to day. A couple of weeks ago, it was around $19 per share, so it’s up nicely since then. I predict it will continue to rise.

SYK: Stryker Corp: Another friendly recommendation. This one is down 2%, but the recommender thinks it’s a good long-term bet, so I’ll hold it for a while.

VB – Vanguard Small-Cap ETF: I like Vanguard funds in general. This one has given me a 5% return.

VIG – Vanguard Dividend ETF: This one pays dividends, which is usually a sign of a strong stock. 1% return.

VWO -: Vanguard Emerging Market ETF: If our economy has problems, emerging markets tend to thrive in response, so I’m hedging my bets with this. It has lost 4% so far.

IDMOX – An ING family fund that has served me well. 13% return.

VFINX – Vanguard S&P index fund. 2% return.

RICK – Rick’s Cabaret: A few days ago, I read an article about Rick’s Cabaret losing a lawsuit that made all of it’s New York strippers into full employees entitled to minimum wage. The article mentioned that Rick’s is publicly traded, which amused me, so I bought a few shares.

Those are the positions I have with one brokerage, across three accounts. I didn’t share the balances, but overall, I have had a 10% return on these investments.

Now, I’ll share the contents of my wife’s inherited IRA. This money was entirely in a money market when she inherited it last year. She got nervous and would only let me play with half of it. That half has averaged a 20% return since June 2012, with part of it hitting 29%.

These are all Fidelity funds for a specific 401k program. I have no idea our accessible the funds are to the general public. We are working on an IRA-mandated withdrawal of this money, so it will be moving over the course of years.

PYR INX LFC 2010/2035/2040/2045/2050 – These are targeted date funds. Each of them has had at least a 20% return.

SM&MID Cap Equity – This fund currently has a 29% 1 year return.

That’s my investment portfolio. Some gambles, some amusement, some solid investments. I think I’m doing pretty well. What do you think?

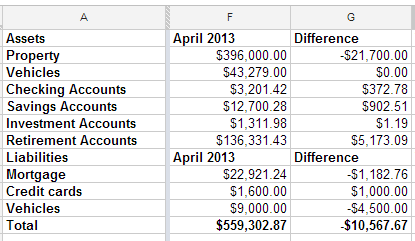

Net Worth Update

I looked back at the spreadsheet I use to track my net worth, and realized that I have been filling it out quarterly, though I can’t say that has been on purpose. Apparently, I get an itch to see my score about four times per year.

This quarter is the first time in a long time that my net worth has dropped. We got our property tax statements last week and found out that our houses have dropped a combined $21,700. Since we’re not planning to sell, that doesn’t matter much.

What’s interesting to me is that, even though our property values dropped $21,700, our total net worth only fell $10,567. We’ve been hustling trying to get the Tahoe paid off. It’s going a little bit slower than I had hoped, but it’s progressing nicely.

I do feel good that, even if I would have been focusing on my mortgage, I still would have lost the mortgage race. That means my misplaced priorities of acquiring more debt to snatch a fantastic deal didn’t cost me the race. Now, I’ll be forced to take a vacation in Texas, coincidentally in the same town as my wife’s long lost brother. I think we can make that work.

I rounded off the credit card and vehicle totals because one is used every day and paid off every month and the other has a steady stream of money getting thrown at it, so the numbers change often.

All in all, I don’t have any room to complain. I am looking forward to paying off the truck and focusing on the mortgage. We could swing quadruple payments, which would pay off the house shortly after the new year starts.