- Guide to finding cheap airfare: http://su.pr/2pyOIq #

- As part of my effort to improve every part of my life, I have decided to get back in shape. Twelve years ago, I wor… http://su.pr/6HO81g #

- While jogging with my wife a few days ago, we had a conversation that we haven’t had in years. We discussed ou… http://su.pr/2n9hjj #

- In April, my wife and I decided that debt was done. We have hopefully closed that chapter in our lives. I borrowed… http://su.pr/19j98f #

- Arrrgh! Double-posts irritate me. Especially separated by 6 hours. #

- My problem lies in reconciling my gross habits with my net income. ~Errol Flynn #

- RT: @ScottATaylor: 11 Ways to Protect Yourself from Identity Theft | Business Pundit http://j.mp/5F7UNq #

- They who are of the opinion that Money will do everything, may very well be suspected to do everything for Money. ~George Savile #

- It is an unfortunate human failing that a full pocketbook often groans more loudly than an empty stomach. ~Franklin Delano Roosevelt #

- The real measure of your wealth is how much you'd be worth if you lost all your money. ~Author Unknown #

- The only reason [many] American families don't own an elephant is that they have never been offered an elephant for [a dollar down]~Mad Mag. #

- I'd like to live as a poor man with lots of money. ~Pablo Picasso #

- Waste your money and you're only out of money, but waste your time and you've lost a part of your life. ~Michael Leboeuf #

- We can tell our values by looking at our checkbook stubs. ~Gloria Steinem #

- There are people who have money and people who are rich. ~Coco Chanel #

- It's good to have [things that money can buy], but…[make] sure that you haven't lost the things that money can't buy. ~George Lorimer #

- The only thing that can console one for being poor is extravagance. ~Oscar Wilde #

- Money will buy you a pretty good dog, but it won't buy the wag of his tail. ~Henry Wheeler Shaw #

- I wish I'd said it first, and I don't even know who did: The only problems that money can solve are money problems. ~Mignon McLaughlin #

- Mnemonic tricks. #

- The Wilbur and Orville Wright Papers http://su.pr/4GAc52 #

- Champagne primer: http://su.pr/1elMS9 #

- Bank of Mom and Dad starts in 15 minutes. The only thing worth watching on SoapNet. http://su.pr/29OX7y #

- @prosperousfool That's normal this time of year, all around the country. Tis the season for violence. Sad. in reply to prosperousfool #

- In the old days a man who saved money was a miser; nowadays he's a wonder. ~Author Unknown #

- Empty pockets never held anyone back. Only empty heads and empty hearts can do that. ~Norman Vincent Peale #

- RT @MattJabs: RT @fcn: What do the FTC disclosure rules mean for bloggers? And what constitutes an endorsement? – http://bit.ly/70DLkE #

- Ordinary riches can be stolen; real riches cannot. In your soul are infinitely precious things that cannot be taken from you. ~Oscar Wilde #

- Today's quotes courtesy of the Quote Garden http://su.pr/7LK8aW #

- RT: @ChristianPF: 5 Ways to Show Love to Your Kids Without Spending a Dollar http://bit.ly/6sNaPF #

- FTC tips for buying, giving, and using gift cards. http://su.pr/1Yqu0S #

- .gov insulation primer. Insulation is one of the easiest ways to save money in a house. http://su.pr/9ow4yX #

- @krystalatwork It's primarily just chat and collaborative writing. I'm waiting for someone more innovative than I to make some stellar. in reply to krystalatwork #

- What a worthless tweet that was. How to tie the perfect tie: http://su.pr/1GcTcB #

- @WellHeeledBlog is giving away 5 copies of Get Financially Naked here http://bit.ly/5kRu44 #

- RT: @BSimple: RT @arohan The 3 Most Neglected Aspects of Preparing for Retirement http://su.pr/2qj4dK #

- RT: @bargainr: Unemployment FELL… 10.2% -> 10% http://bit.ly/5iGUdf #

- RT: @moolanomy: How to Break Bad Money Habits http://bit.ly/7sNYvo (via @InvestorGuide) #

- @ChristianPF is giving away a Lifetime Membership to Dave Ramsey’s Financial Peace University! RT to enter to win… http://su.pr/2lEXIT #

- @The_Weakonomist At $1173, it's only lost 2 weeks. I'd call it popped when it drops back under $1k. in reply to The_Weakonomist #

- @mymoneyshrugged It's worse than it looks. Less than 10% of Obama's Cabinet has ever been in the private sector. http://su.pr/93hspJ in reply to mymoneyshrugged #

- RT: @ScottATaylor: 43 Things Actually Said in Job Interviews http://ff.im/-crKxp #

- @ScottATaylor I'm following you and not being followed back. 🙁 in reply to ScottATaylor #

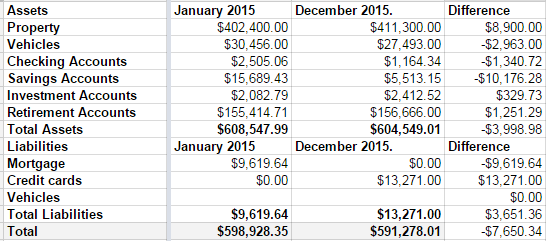

Net Worth and other stuff

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

- We’re going to save for college at a rate we should have started 10 years ago.

- We’re going to max out both of our retirement plans.

- We’re going to take some nicer family vacations.

- We’re going to buy a pony.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

My Financial Plan – How I Improve on Ramsey

In April, my wife and I decided that debt was done. We have hopefully closed that chapter in our lives. I borrowed, then purchased, The Total Money Makeover by Dave Ramsey.  budget” width=”300″ height=”213″ />We are almost following his baby steps. Our credit has always been spectacular, but we used it a lot. Our financial plan is Dave Ramsey’s The Total Money Makeover, with some adjustments.

budget” width=”300″ height=”213″ />We are almost following his baby steps. Our credit has always been spectacular, but we used it a lot. Our financial plan is Dave Ramsey’s The Total Money Makeover, with some adjustments.

Step 1. Budget:

The budget was painful, and for the first couple of months, impossible. We had no idea what bills were coming due. There were quarterly payments for the garbage bill and annual payments for the auto club. It was all a surprise. Surprises are setbacks in a budget.

When something came up, we’d start budgeting for it, but stuff kept coming up. We’re not on top of all of it, yet, but we are so much closer. We’ve got a virtual envelope system for groceries, auto maintenance, baby needs(we have two in diapers) and some discretionary money. We set aside money for everything that isn’t a monthly expense, and have a line item for everything that is. My wife is eligible for overtime and monthly bonuses. That money does not get budgeted. It’s all extra and goes straight on to debt, or to play catch-up with the bills we had previously missed. I figure it will take a full year to get all of the non-monthly expenses in the budget and caught up.

Step 2. The initial emergency fund:

Ramsey recommends $1000, adjusted for your situation. I decided $1000 wasn’t enough. That isn’t even a month’s worth of expenses. We settled on $1800, plus $25/month. It’s still not enough, but it’s better. Hopefully, we’ll be able to ignore it long enough that the $25/month accrues to something worthwhile.

Step 3. The Debt Snowball:

This is the controversial bad math. Pay off the lowest balance accounts first, then take those payments and apply them to the higher balance accounts. Emotionally, it’s been wonderful. We paid off the first credit card in a couple of weeks, followed 6 weeks later by my student loan. Since April, we’ve dropped nearly $10,000 and we haven’t made huge cuts to our standard of living. At least monthly, we re-examine our expenses to see what else can be cut.

Step 4. Three to six months of expenses in savings:

We aren’t on this step yet. In step 2, we are consistently depositing more, making us more secure every month.

Step 5. Invest 15% of household income into Roth IRAs and pre-tax retirement:

I have not stopped my auto-deposited contribution. It’s stupid to pass up an employer match. My wife’s company does not match, so she is currently not contributing.

Step 6. College funding for children:

We have started a $10 College fund.

Step 7. Pay off home early:

I don’t see the point in handling this one separately. Our mortgage is debt, and when the other debts are paid, we will be less than a year from owning our house, free and clear. This is rolled in with step three. All debt is going away, immediately.

Step 8. Build wealth and give!

We have cut off most of our charitable giving. Every other year, it has been a significant percent of our income, and in a few more years, will be so again. The only exception to this is children knocking on the door for fundraisers. I have no problems with saying no to a parent fundraising for their kid, but when the kids is doing the work, door-to-door, especially in the winter, I buy something. My son’s school, on the other hand, gets fundraisers ignored. When they come home, I send a check to the school, ignoring the program. I bypass the overhead and make a direct donation.

Working My Life Away

Since J. and Crystalare playing, and I don’t have a post scheduled for today, I thought I’d share my work history, too.

There are a couple of interesting things about my work history. Job #1 started when I was 6. Job #9 started when I was 21. I’m 33 now.

- Paper route. I delivered the local ad-rag. The route was split with my brothers. When I was 6, my share of the route was just the street we lived on. I think I had 8 papers to deliver. Later, that expanded to almost half of our tiny town.

- Odd farm jobs. I spent some time doing whatever needed to be done on a local hobby farm. That means everything from helping shore up a sagging wall in the barn to raking walnuts off of the yard.

- Dishwasher at my school. My freshman year, I gave up a study hall to wash dishes and serve lunch. My school was K-12, so I’d eat at the same time as the little kids, then wash their dishes and serve lunch to the rest of the students for $4.25/hour. I kept at it until my senior year, when I decided to relax a bit.

- Construction. Working with my Dad, until I fell off a ladder and severed a tendon in my finger when I landed. Easily the most difficult boss I’ve ever had, but it was excellent preparation for every other job I’ve ever had. His philosophy was that if he had to ask for it, I should have already known he needed it. Try carrying that training into another job and see if they complain.

- Dishwasher/Cook. I turned 16 and needed a job to afford a car that I needed to get a job. Nasty cycle. It took a couple of weeks of looking. Apparently, if a teenager puts on a nice shirt and shows up to the interview on time, he is way ahead of the curve. It took about 2 months to go from dishwasher to cook, and I kept the job until I was 18. I was working full-time all through high school.

- Palletizer. I spent 9 months standing at the end of a conveyor belt, picking up 50 pound bags of food powder mixes, taking 3 steps, and putting them on a pallet. We averaged 1500 bags per night. Fifteen years later, I still can’t comfortably button the cuffs of most shirts. When I flex, my forearms look like I have an unhealty “adult” internet addiction.

- Cook. While I was palletizing, I had a second job as a cook at a bar, working for a guy who was trying to avoid turning a profit by drinking his main product. This was 5 miles from the other job, and my car died right after I started, so I biked from job to job. In Minnesota. In the winter. I was a lean, mean popsicle.

- Machine Operator. I moved from the sticks to the Minneapolis area and was immediately hired to be run a CNC machine based on a friend’s recommendation to his boss. The pay was great for an 18 year old with no skills. I worked 5 twelve-hour graveyard shifts. The job mostly consisted of putting a little chunk of metal into a machine, closing the door, pushing a button, and sitting down for 15 minutes. This is the period of my life that trained me to shop for books based primarily on thickness.

- Bill Collector/System Administrator. After Brat #1 was born, 12 hour graves got to be a big pain. I’d work from 5 to 5, come home and make sure my wife got at least 4 hours of sleep, then I’d sleep for 4-5 hours and go back to work. Brat #1(who is now 13 and about 6 feet tall) needed to be fed every hour, so solid sleep didn’t happen for months. I took a pay cut to work normal, day-shift hours. I ended up working my way through college by collecting on defaulted student loans. Shortly after I graduated, I got promoted to be the system administrator of the collection system, responsible for hundreds of millions of dollars of debts flowing into and through our system correctly. I had a security clearance allowing me access to the Department of Treasury’s computer system. After a few years of this, the company decided that there were too many people with the same job description, so 5 overworked admins got laid off while the 6th got screwed with far too much work.

- Software Engineer. This is now. I write cataloging and ecommerce software, while managing a small team of programmers. I spend half of my day working on customer software estimates, training, and assisting on sales demos and half of my day writing code. I’m kind of a big deal.

That’s it, if I don’t count my side hustles. I’ve been earning a paycheck for 27 years, and have only had 10 jobs.

When did you start working? How many jobs have you had?

Save Your Family

I don’t attach much importance to dreams. They are just there to make sleepy-time less boring. Last night, I had a dream where I spent most of my time trying to prepare my wife to run our finances before telling my son that I wouldn’t be around to watch him grow up. That’s an unpleasant thought to wake up with. Lying there, trying to digest this dream, I started thinking about the transition from “I deal with the bills” to “I’m not there to deal with it”. We aren’t prepared for that transition. Last year, we started putting together our “In case of death” file, but that project fell short. The highest priorities are done. We have wills and health directives, but how would my wife pay the bills? Everything is electronic. Does she know how to log in to the bank’s billpay system? Which bills are only in my name, and will go away if I die? Is there a list of our life insurance policies?

I checked the incomplete file that contains this information. It hasn’t been updated since September. It’s time to get that finished. Procrastinating is inappropriate and denial is futile. Here’s a news flash: You are going to die. Hopefully, it won’t happen soon, but it will happen. Is your family prepared for that?

The questions are “What do I need?” and “What do I have?”

First and foremost, you need a will. If you have children and do not have a will, take a moment–right now– to slap yourself. A judge is not the best person to determine where your children should go if you die. The rest of it is minor, if you’re married. Let your next-of-kin, your spouse keep it. I don’t care. Just take care of your kids! Set up a trust to pay for the care of your children. Their new guardians will appreciate it. How hard is it to set up? I use Quicken Willmaker and have been very pleased. Of course, the true test is in probate court, and I won’t be there for it. If you are more comfortable getting an attorney, then do so. I’ve done it each way. You can cut some costs by using Willmaker, then taking it to an attorney for review.

It’s a sad fact that often, before you die, you spend some time dying. Do you have a health care directive? Does your family know, in writing, if and when you want the plug pulled? Who gets to make that decision? Have you set up a medical power of attorney, so someone can make medical decisions on your behalf if you aren’t able? Do you want, and if so, do you have a Do-Not-Resuscitate order? Willmaker will handle all of this, too.

What’s going to happen to your bank accounts? I’m personally a fan of keeping both of our names on all of our accounts. I share my life and my heart, I’d better be able to trust her with our money. If that’s not an option, for whatever reason, fill out the “Payable on Death” information for your accounts, establishing a beneficiary who can get access to your money if you die. Do you want your spouse to lose the house or the car if you die? Should your kids have to miss meals? Make sure necessary access to your money exists.

Does anybody know what you have for life insurance? Get a copy of the policy and make sure your spouse and someone else knows what company holds it and how much it is worth.

Now, it’s time to make some lists. You need to gather account numbers and contact information for everything.

- Bank accounts. List every bank and account you own. Checking, savings, CDs.

- Investment accounts. Again, every company, every account.

- Mortgage and car payment information.

- Life insurance. Get your policy numbers, contact information, beneficiaries, and amount of coverage all in one place.

- Credit card accounts. Every card, every company. If it’s just your name on the account, your spouse will need to send certified death certificates to stop collections. Otherwise, she’ll need to pay the bills.

- Utilities. Get the account number for the electric bill, the gas bill, water/sewer/garbage, cable and phones.

- Other bills. These include car/home insurance, Netflix, memberships and anything else you pay.

- I’ve included the account information for my web host, registrars and websites. Some of it is salable, some of it is income-generating.

- Car titles. Put the actual titles in the pile of lists.

- Property deeds. Keep these here, too.

Non-financial information to list:

- Online accounts. Any financial sites that would be useful, or any community sites you would like to have informed about your death. Your online presence is a part of who you are.

- Email accounts. Will your survivors need to interact with anybody potentially contacting you? They will need your username and password, or most big providers won’t let them in.

- Social media. How many networks do you participate in? Do you want to disappear, or should all of your Facebook friends know your dead?

- Blogs. Do you have a blog that needs an announcement? Does it generate income? Could it be sold?

- Contact list. Who else needs to be informed of your demise? Don’t make your loved ones hunt for the information.

Now, take all of this information and put it in a nice, fat envelope and lock it in the fireproof safe you have bolted to the floor. Make a copy and give it to someone you trust absolutely. Make sure someone knows the combination to the safe or where to find the key.

Your loved ones will appreciate it.

5 Personal Safety Apps that Could Save Your Life

No one likes to think about the possibility of dying too young. But knowing that potential exists, you take the smart step of protecting those you love by carrying term life insurance. But what about preventing the worst? Did you know your iPhone or Android device can call for help or record vital information if you ever find yourself in a life-threatening situation? Here are five personal safety apps that could save your life.

1) myGuardianAngel

Once this app allows you to reach all of your emergency contacts with the push of one button. You enter the contact information for anyone you would want to get in touch with if you were in any sort of emergency as soon as you download it. If you are in an emergency, the app will call your contacts, send them an e-mail with your GPS location and immediately begin recording audio and video from your phone.

2) StaySafe

This app is good for anyone who works or travels alone. You can schedule the app to automatically notify friends or family after a certain period of time when your phone is inactive. For example, you can estimate how long you expect to drive from one location to another on your own and then the phone will contact someone automatically if you are out of contact longer than expected. That way your friends will know to send help because something is wrong, even if you aren’t in a position to contact them yourself. StaySafe sends your contacts a detailed GPS location for you so that they can easily find you and bring help.

3) RESCUE

This full-service app can help you on the scene as well as notify your emergency contacts for you. If you are in trouble, you can trigger the app to sound a loud alarm that might frighten off anyone who might be planning to do you harm. The alarm can also help someone find you if you are lost or unable to move from your current location. When the alarm is triggered, the app will also send immediate notifications to your emergency contact list so that they can begin to send help right away. Emergency services such as the police and fire department can also be set for notification through the RESCUE app.

4) Night Recorder

This is a good app to have when you need to make a quick recording of your surroundings for any reason. The app can be set to begin recording at a touch. If you are stranded, you could create a recording by speaking about the landmarks you can see and explaining how you got to your current location. The recorder can then send an email of your recording to anyone on your contact list.

5) iWitness

With this app, you can instantly make video or audio recordings of your situation so that there is a permanent first-hand record of everything that happens. It is a handy tool for anyone who has been in a car accident or involved in a medical emergency because you can go back and look at the video to see exactly what happened if there is any question about it later. The app will also contact emergency services or your personal emergency contacts if you are in trouble. The built-in GPS locator will transmit your exact location so that people can find you quickly and easily.

Post by Term Life Insurance News