This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

The no-pants guide to spending, saving, and thriving in the real world.

This is a conversation between me and my future self, if my financial path wouldn’t have positively forked 2 years ago. The transcript is available here.

What would your future self have to say to you?

We had a garage sale last week, as a wrap-up to the April 30 Day Project. We got rained out halfway through the first day of our 3-day sale, but we still managed to clear $1500. We held the sale in our neighbor’s garage because it had more space and better visibility.

Wednesday night, while carrying boxes over, I missed the step to their property from our driveway and crashed while carrying three boxes. That’s a twisted ankle and a bleeding knee. Naturally, while I’m hopping and swearing, everyone is concerned that I’m okay. The worry-warts. Anyway, it hurt, so we stopped setting up while we still had a few boxes left in the basement.

[ad name=”inlineleft”]Thursday morning, I decided to show them all. At 5:30AM, before anybody else is strongly considering the possibility of maybe thinking about getting ready to hit the snooze button, I decided to get the rest of the boxes ready. They’d all wake up, worried about how I’m feeling, asking if I’m to stiff to carry boxes. The best way to show them they don’t need to worry would be to have all of the boxes dealt with before they woke up. So I started. Up and down the stairs, with a stiff, twisted ankle, gloating to myself about how tough I was…BOOM, down the stairs. I was on my back, sliding down the stairs. I caught a stair-tread in the small of my back and another on the point of my tailbone. Mommy?

After I stopped twitching on the floor at the base of the stairs, I managed to get the last of the boxes ready. Instead of sympathy, I spent the rest of the weekend getting asked if I needed an inflatable doughnut to sit on. There are places I’d prefer not to have bruised.

Unpacking the boxes made me glad that everything was priced. We spent 6 weeks going through our entire house–every room, every dresser, every drawer–to eliminate the clutter. As something went into a box, it got priced, so we didn’t have to do it all at the last minute. That is the most important time-saving step for a garage sale. Price it as you pack it. You don’t want to waste hours pricing stuff while tripping over potential customers.

Another preparation tip to do early: Find tables! Ask around. You’d be surprised at who has a dozen folding tables collecting dust in his basement. It’s better to borrow that to rent. The best price I found was $17.50 to rent an 8′ X 30″ table for a week. We didn’t have to do that, but we thought we would have to. I borrowed a few, found a few, and built a few out of sawhorses.

The week before the sale, we placed an ad in the paper. When I placed the ad, the paper called to suggest we change it from running the weekend before to running just the days of the sale. I agreed, to a point, but their Sunday circulation is miles ahead of the weekday circulation, so why pay to run an ad nobody will see on Thursday? I ran it Sunday through Tuesday, because I wanted the Sunday ad and we got 3 consecutive days in the price. Did I actually know better than the paper’s sales-weasel? Who knows? I think I made the right decision.

The Sunday before the sale, I posted an ad on Craigslist. Interesting fact: little old ladies use Craiglist to plan their garage-sale adventures.

Two days before the sale, we made signs. Bright pink signs with brighter yellow starbursts. They were all simple. “Mega Sale! 8-5” followed by an arrow and our address. Simple, easy-to-read, and bright. The morning of the sale, after the ibuprofen kicked in, I put the signs up. When you make signs out of paper, always include a crossbar. It rained a lot the first day of the sale, so the signs wilted. The second morning, I went out with some duct tape and crossbars and fixed them all.

The day before the sale, we got cash and change. We had $50 in 1s and 5s and $25 in silver change. No pennies. Nothing was priced to make us need them.

The morning of the sale, we set up two canopy tents in the driveway and pulled the prepared-and-filled table out under them. We finished stacking as much as we could on the tables and called it “open”. There were a few boxes we couldn’t put out due to the rain. We simply ran our of room. At noon, $65 into the sale, we decided enough was enough and shut down–cold, wet, and miserable. Lunch and a nap made the day better.

Later, I’ll discuss the other parts of our successful sale.

Note: The entire series is contained in the Garage Sale Manual on the sidebar.

Update: This post has been included in the Money Hacks Carnival.

I work daily to raise my kids to be more financially responsible than I have been. One of the most difficult pieces has been to explain the benefits of delayed gratification to my children. It’s hard enough, as an adult, to take delayed gratification to heart. For a child? It seems to be almost impossible.

My son wants an XBox 360 Elite. Good for him. He wants to renegotiate the terms of his allowance to get it faster. Currently, every other time he gets an allowance paid out, it goes into his bank account, to be mostly untouched. The other times he can do as he pleases with his money. We are enforcing a 50% long term savings plan. Now, with a medium-term goal in mind, he wants to keep all of his money, and only put gift money into the bank account.

Should we let him tap his bank account for a shiny new bauble? It’s been building for a while, so it’s delayed, right? I don’t think that would accomplish much. Like any other 10-year-old, his interests change often.

Should we let him change the terms of our agreement, speeding a medium-term goal at the expense of his long-term savings? My wife and I haven’t had a chance to discuss this, but my initial reaction is not to allow it. His savings has the potential to turn into a decent car in a few years, if he wants. That would be a car he knows he earned.

Last week, when we were at the store, he asked if he could borrow some money to buy a game. I don’t expect him to carry his money around everywhere, so I would have allowed it, if he would have had the money at home. He didn’t. His plan was to pay me what he did have as soon as we got home, then work his butt off for a few days to earn enough extra to pay it back. I won’t be a credit agency for my kids, so I said no. He was disappointed, but, by the time he had earned the money, he no longer wanted the game. I consider that a win, but I don’t know that he learned any lesson other than “Dad’s a jerk.”

Someday, when his life launch is smooth due to a lack of debt-dependence, he’ll look back on these lessons and smile.

I hope.

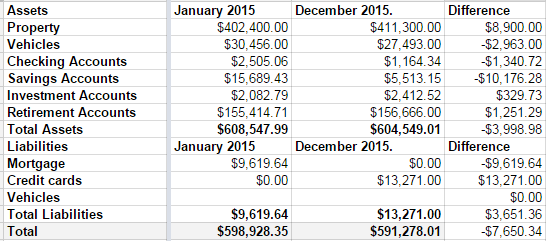

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

I’m not a huge fan of New Year’s resolutions. Generally speaking, if you don’t have the willpower to do something any other time of the year, you probably won’t grow that willpower just because the last number on the calendar changed.

Seriously, if you’ve got something worth changing, change it right away, don’t wait for a special day.

That said, this is the time of the year that many people choose to try to improve…something. Some people try to lose weight, other people quit shooting meth into their eyeballs, yet others(the ones I’m going to talk about) decide it’s time to get out of debt.

Now most people are going to throw out some huge and worthless goals like:

The problem with goals like that is the definitions. What is “some”, “more”, “better”, or “less”? How do you know when you’ve won.

It’s better to take on smaller goals that have real definitions.

Try these:

But Jason, I hear you saying, where am I going to find $1000 to save? Well, Dear Reader, I’m glad you asked. Next time though, could you ask in a way that others can hear so my wife doesn’t feel the need to call the nice men in the white coats again?

Let’s break that goal down even further.

Instead of saving $1200, let’s call it $100 per month. That’s a bite-sized goal. Some people don’t even have that to spare, so what can they do?

Let’s make that resolution something like “I’m going to have frozen pizza instead of my regular weekly delivery.” If your house is anything like mine, that brings a $60 pizza bill down to $15 for some good frozen pizza for a savings of $45. If you order pizza once a week, that’s $180 saved each month, double your goal. That’s a win with very little suffering.

Now, you can take that extra $80 that you hadn’t even planned for and throw it at your credit cards. That’s a free payment every month. Before you know it, you’ll have your cards paid off and a decent savings account.

Then you can thank me because I made it all possible.

Last week, my wife posted on Facebook that she was frustrated with her job hunt.

An hour later, she got a call from someone she hadn’t talked to in 10 years. He wanted to talk about a great business opportunity. He wouldn’t say what it was, but wanted to bring a friend over to discuss it.

Fast forward to last night.

The night my wife agreed to meet with the old friend.

The meeting we forgot about.

So we invited our friend and his friends into the house. We sat down at the dining room table to hear the pitch. Our friend is just getting started so his “friend” delivered the pitch.

While I was waiting for him to explain the business, he was showing us pictures of he and his wife traveling around the country.

Instead of explaining the product, he asked about our most expensive dreams.

Instead of telling us how the marketing worked, he mentioned something about utilizing the internet–and i-Commerce–and talked about changing our buying habits.

Instead of showing us a product, he talked about driving volume and building a team.

There was nothing concrete, but a lot was said to ride on the dreams of people who are frustrated with their income or are living paycheck-to-paycheck.

More than an hour into the presentation, it was revealed that the “product” is a buying portal to allow people to buy Amway products from your personal Amway store.

Freaking Amway.

How do they find your personal Amway store, you ask? I don’t know, because you are supposed to be your own best customer. You make money by buying the products you use anyway, but buy them from Amway. For example, there’s the $10 toothbrush, the $16 baby wipes, or the $38 toilet paper.

For six frickin’ rolls.

Seriously, this stuff is meant to touch my butt once. I don’t need it made from pressed gold.

As for the visual…you’re welcome!

So I sell a kidney to buy enough toilet paper to keep my nether bits clean for a month and I get one point for every $3 I spend. I figure that’s about 50 points per month, given the foot traffic our bathrooms see.

If I hit 100(I think, he didn’t leave the paperwork) points, I get 6%(again, I wasn’t taking notes) back at the end of the next month. For the sake of the math, I’m going to double the number of butts in my house. 100 points means I need to spend $300. That’s 47 rolls of toilet paper. In exchange for this $300–and on top of gold-embroidered silk I now get to flush down the toilet–I’ll earn $18.

I know exactly how much toilet paper I buy right now. Amazon sends me a 48 roll package every other month for $31.42, shipped.

To simplify, Amway is offering me the ability to spend $300 to get $18 plus $31.42 worth of toilet paper. I’m supposed to end my financial worries by turning $300 into $50 every month.

Yay!

[Note to self: Demolish Amway’s business model by starting a company that will let people turn $200 into $50, without the nasty overhead of stocking overpriced crap. A 33% increase in efficiency will make me rich!]

But wait, say the imaginary Amway proponents that I hope aren’t frequenting my site, you’re forgetting the most important part!

Oh really?

There’s also a thing called a “segmented marketing team”. To the rest of the multi-level marketing world, this is known as your downline. If you can con your family and friends into turning their $300 into $50 every month, then help them con their family and friends into turning $300 into $50 every month, you’ll get rich! Amway has apparently figured out a way to share a small fraction of their 600% markup with their victims to make them feel like it’s a business opportunity instead of a robbery.

If I get 9 people in my “business team” and each of them build out their team, I get the coveted title of “Platinum Master” or whatever. All I have to do is sell the souls of 72 people and I can make a ton of money! If each member of my downline turns $300 into $50, Amway will get $18,000. In exchange for delivering those souls, the “average” Platinum Ninja makes about $4500 per month. That’s about $12,000–free and clear–for Amway.

When your business model consists entirely of your sales force doing all of the buying and consuming, it’s not a business model, it’s cannibalism.