- RT @ScottATaylor: Get a Daily Summary of Your Friends’ Twitter Activity [FREE INVITES] http://bit.ly/4v9o7b #

- Woo! Class is over and the girls are making me cookies. Life is good. #

- RT @susantiner: RT @LenPenzo Tip of the Day: Never, under any circumstances, take a sleeping pill and a laxative on the same night. #

- RT @ScottATaylor: Some of the United States’ most surprising statistics http://ff.im/-cPzMD #

- RT @glassyeyes: 39DollarGlasses extends/EXPANDS disc. to $20/pair for the REST OF THE YEAR! http://is.gd/5lvmLThis is big news! Please RT! #

- @LenPenzo @SusanTiner I couldn’t help it. That kicked over the giggle box. in reply to LenPenzo #

- RT @copyblogger: You’ll never get there, because “there” keeps moving. Appreciate where you’re at, right now. #

- Why am I expected to answer the phone, strictly because it’s ringing? #

- RT: @WellHeeledBlog: Carnival of Personal Finance #235: Cinderella Edition http://bit.ly/7p4GNe #

- 10 Things to do on a Cheap Vacation. https://liverealnow.net/aOEW #

- RT this for chance to win $250 @WiseBread http://bit.ly/4t0sDu #

- [Read more…] about Twitter Weekly Updates for 2009-12-19

How You’re Finding Me

Every once in a while, I like to dig through Google Analytics and see how people are finding this site. Some of the search terms are interesting.

“father of three” mid life crisis

Here’s a free piece of advice. As a father of three, you don’t get to have a mid-life crisis. It’s not allowed. Rather, it’s allowed, but you aren’t allowed to act on it. At a minimum, until your children are out of the house, you need to man up and provide all of the support you possibly can. No sports cars you can’t afford and no 22 year old hardbodies. Be there for your kids.

“payday loans” which accepts guest posts

Payday loan marketing. Just go away. You aren’t running a guest post here.

“slow carb” hungry all the time

You’re doing it wrong. If you are hungry, eat more bacon. Or beans. Beans fill you up longer.

$1000000 business idea

Ideas are the easy part. Execution makes you a millionaire.

articles on why appearance shouldn’t matter?

Appearances do matter, and always will. Your appearance is what makes the initial impression when you meet someone new. You don’t have to be a model, but basic grooming and fashion sense is necessary. Take this with a grain of salt. I’ve got a week’s growth of a beard and I wear a different plaid, button-down shirt every day.

are push ups supposed to be hard

Only the first 50. After that, I kind of go on blissed-out autopilot. If you can do 100 pushups, you can probably do 200.

acceptable place to put tattoo

If you wear clothes there, you can put a tattoo there. Visible tattoos are called “job stoppers” for a reason. If you put a tattoo on your face, the only job you qualify for is “drug dealer’s girlfriend”. Or possibly prison janitor.

burning bridges with toxic people

If you must burn bridges, filling them with toxic people first isn’t a bad idea.

candied pork butt

Rule 34: If it exists, there is porn of it. Interesting side story: while double-checking the rule number, I stumbled across My Little Ponies doing things they never advertise on the box.

cut my wife’s hair

I did this once. Pro tip: In the back, at the bottom, cut small chunks and leave them longer than you think they should be. You can always cut more, but uncutting hair is really hard.

f***** on the roadside by your mechanic

He probably deserves a tip for that.

girls fart for money and girls live farts

See the bit about the pork butt, remove the funny, and…ewww.

how to be a successful debtor

I recommend starting by paying your bills. When the debts are gone, you win. Success!

i ate bacon on slow carb diet

So did everyone else, sweetie. It’s the biggest draw to the slow carb diet.

in memory of pets tattoos

When I get a pet, I get it with the understanding that I’m going to outlive it. The day I bring it home, some small part of me is preparing for the day when I have to dig a hole in my backyard. Tattooing that day? Not gonna happen.

thickening felt behind testicle

Why are you on google? Go to the doctor. Please?

Interesting. Between girls farting and my post about being well-trained, there is a significant amount of fetish traffic coming through here. Maybe I need to explore a new advertising strategy.

10 Tips to Help Parents Stay Out of Debt

, jigger, and a bar spoon.")

People say that when you have a baby, your world gets flipped upside down. That’s not true. Your world gets dropped in a martini shaker and left to the whims of a sadistic bartender with a shaking fetish. Everything changes. That sounds like an exaggeration and nobody believes it until it happens, but it’s true.

When you find out you are about to reproduce, you will experience a phenomenon called “nesting”. Nesting is the idea that, if you take your credit cards and beat them against the curb until they bleed and VISA calls you asking for mercy, you will be transformed into the best parent ever, regardless of what you may actually screw up. It’s the way parents calm their fears by spending money, often on things that aren’t needed.

Q. How do you avoid becoming a debt-ridden, worried mess of an over-protective, over-extended new parent?

A. What do you get when you cross an elephant and a rhinoceros?

I can’t help with the rest, but here’s 10 ways you can avoid the debt problems.

- Have a budget. I may have said this before. It’s possible this counts as a recurring theme here. If you don’t have a budget, you aren’t in control of your money. If you aren’t in control, then how do you know where it has gone or where it is supposed to go?

- Budget for baby crap. This will be a recurring expense for years, so get used to it. A friend of mine is on the cusp of having everyone out of diapers for the first time since 1993. Do you think they plan that expense? Diapers.com has $10 off and free shipping on orders over $49. Use code “ LiveReal” during checkout.

- Double the number you have in #2. Seriously. It will cost you more than you think, but it doesn’t have to cost you as much as you fear. It’s far better to have too much budgeted and find yourself with extra money than it is to budget too little and be forced to make up the difference at the feet of Master Card.

- Only take the advice of people you know and trust. Every random jerkface on the street has (usually) well-intentioned advice for new and expecting parents. Ignore them all. If they aren’t your doctor, your mother(assuming she did her job right), or friends with children, they are clueless and their advice should be immediately round-filed. Ditto for parenting magazines. The writers don’t know better than you do. Read the magazines for six months and watch for conflicting advice, not only in the same magazine, but often from the same writer! Don’t add the stress of bad advice from strangers to what is already a stressful time.

- Don’t get every gadget designed to cushion the baby. A wipe warmer is a waste of money. Do you want your baby to be scared of a little chill forever? Cold wipes build character. If that isn’t good enough, hold the wipe in your hand for a few seconds before using it. There are a million other gadgets to keep your little one from ever feeling a moment of discomfort. Don’t waste your cash. It may only be 10 pounds, but it’s tougher than you think.

- Don’t get every gadget designed to cushion the parent. They make ergonomic bottles, braces to hold your arms in the right position to feed, fancy cloths to catch baby vomit. Tough it up. Support your baby yourself. Build some muscle and some character. Use cloth diapers to catch various treasures your little brat will spit up on you. Spending more doesn’t always make it better. The ergonomic bottles that make it easier to feed a baby, make it harder for the baby to hold the bottle. This is actually making your life more difficult.

- Focus on the necessities. Yes, the fancy formula with the pre-digested proteins has a nicer label. It doesn’t make a difference. The generic brand at the warehouse store usually has the exact same ingredients in the exact same ratios as the brand name at the baby store–for half the price. There is nothing special about the blankets in the baby section–except the price. The fancy bottle warmer doesn’t do anything that a cup of warm water on the counter won’t handle. You need: A crib, unless you are doing a family bed; a easy-to-clean mat to change diapers(on the floor works!); and a diaper bag(back-to-school backpacks are more ergonomic and easy to organize than anything in the baby store!). Everything else is a luxury.

- Time counts more than stuff. No matter what else you hear, no matter how old your child gets, time with you counts more than anything else you could do or buy. Be there for your kids and the rest is gravy.

- Brand-name and designer labels are not status symbols. The opinions of the other soccer mommies do not matter. The opinions of the random jerkfaces on the street do not matter. Designer labels do not make you a better parent and are not an indicator of a happy baby.

- Always remember: Babies bounce and have short memories. While I don’t recommend bouncing your baby on the floor, they are surprisingly resilient. They don’t hold grudges, either. There is room to make mistakes without screwing up your kid.

For a hundred thousand years, people raised babies with nothing more than a scrap of hide to alternately chew on or wipe with. You can probably get buy with just a bit more. Relax and enjoy the process of raising your kids. Money doesn’t matter nearly as much as your presence.

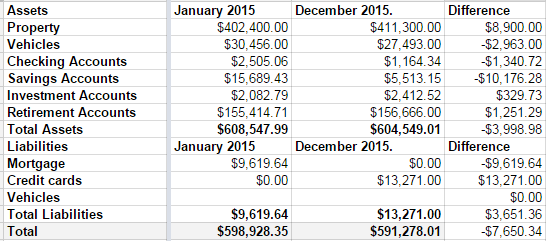

Net Worth and other stuff

This was not a good year for our net worth.

Over the summer, we remodeled both of our bathrooms. At the same time.

1 out of 10: Don’t recommend.

We love the bathrooms, but–as with any project–it went over budget. Sucks to be us.

Then, towards the end of the year, we decided to push hard and pay off our mortgage in 2015. Part of doing that meant paying the credit card off slower than we’d like. It wasn’t the best long-term decision, but we’re mortgage-free now.

Those decision, coupled with a small slump in our investment accounts means we are worth $7650 going into 2016 than we were at the start of 2015.

Disappointing.

I’m also disappointed that our credit card discipline slipped last year.

New plan: No debt before tax day. Every cent of Linda’s paycheck, every cent of my monthly bonus checks, and every cent of any extra money we make is going into the remaining credit card debt. My math says that last debt will die on April 1st.

Then we get to talk about what to do with out money when there’s no debt. But never fear, I have a plan. A boring, boring plan.

- We’re going to save for college at a rate we should have started 10 years ago.

- We’re going to max out both of our retirement plans.

- We’re going to take some nicer family vacations.

- We’re going to buy a pony.

So not that boring.

And when our kids all decide to become certified sign-spinners, we’ll have a huge nest-egg in the college fund savings account to spend on lottery tickets.

I Smell a Scam

I hate scammers. Whether it’s the garage-sale shoplifter, telemarketing “charities” with 99% overhead, 3-card-monte

dealers, or the guy who begs Grandma for cash every week, they all need to be strung up. Since vigilante justice is generally illegal and occasionally immoral, it’s best to just avoid the problems from the start. Here are some scams to watch out for.

Pyramid Scams – All of the little parties people throw to earn free items at the expense of their friends are pyramid schemes. Most of those are legitimate money-sinks. A few, however, exist solely to get their “consultants” to bring in more consultants. The sales aren’t the actual way to make money. If you don’t have anyone “downstream” you won’t make any money. If the focus isn’t on selling an actual product or service, but is instead on bringing in people under you, you have entered the world of pyramid scams. Generally illegal and always immoral. Don’t sign up and, if you do, don’t ask me to participate.

Advance Fees and Expensive Prizes – If you win a contest and you are expected to send money to claim your prize, it is a scam. You don’t have to pay sales tax in advance. You don’t have to pay transfer fees. Real prizes are delivered free, accompanied by a 1099, because prizes are income. No prize requires pre-payment. No loan service requires “finder’s fees”. If it doesn’t sound right, don’t pay it and certainly don’t give your bank information to anyone you can’t verify.

Work at Home – The most common work-at-home job I’ve found is stuffing envelopes. You see the signs on telephone poles all over the city. “Make $10/hour stuffing envelopes from the comfort of your own home! Just send $50 to….” When you get the instructions, you are told to hand up signs telling people to send you $50 for instructions on how to make $10/hour stuffing envelopes. Everybody is feeding off of everybody else.

Charity – Never give money to a charity over the phone. Always take the time to verify where you are sending your money. Some freak may call to tug on your heartstrings with a sob story, but you don’t have to give them money. At least ask them to send it in writing so you can do some checking, first.

Phishing – Simply put, don’t click on any link in any email, unless you know where it is going. If it is a link to a financial institution, go enter the address into the address bar yourself. If you find yourself on a site you don’t recognize, don’t give them your personal information and don’t ever reuse your usernames and passwords. If you do, one bad site could get access to everything you do online.

[ad name=”inlineleft”]Foreign Lottery – To be clear, Spain did not just hold a international lottery and randomly draw your email address. No lottery in the world works that way. If you didn’t enter the lottery while you were in Spain, you aren’t going to win it. The scam is that you need to provide your bank information, including a number of release forms so the scammers can transfer money to you. In reality, you are signing over control of your account and will be wiped out.

Nigerian/419 Emails – Ex-Prince WhateverHisNameIs wants your help to get his fortune out of WhereverHeIsFrom. The New Widow Ima F. Raud has an inheritence that she won’t live long enough to spend. They’ve both been given your name as a trustworthy person to handle the transactions in exchange for a mere $10 million. What friends do you have that would make this seem legitimate? Once again, they will get your bank information and take your money. At a minimum, they will try to get you to pay a few thousand dollars for “Transfer fees”. Don’t do it.

Overpayment by Wire – I had this one attempted on my last week. You sell something online. A potential buyer agrees to purchase the item, sight-unseen. They’ll send a cashier’s check and, after it clears, one of their agents will pick it up. Unfortunately, the buyer’s secretary screwed up and added a zero to the check. Would you mind wiring the overpayment back, minus a small fee for the hassle? The check is bogus and there is no way to verify it. You’ll deposit the check and it will be assumed to be real. The bank will make the funds available well before it comes back as fraud. You’ll see the available funds and send the money by non-refundable Western Union and some thug in Nigeria gets a new iPhone.

Foreclosure Scams – Some scammers try to prey on the vulnerable because they are, well, vulnerable. If you are facing foreclosure, be very careful about where you turn for help. One scam is to get you to sign over your home “temporarily” to clear the title. That doesn’t work, but you won’t find that out until you are handed an eviction notice and told you still owe the money.

Stranded Friends – You get an email from a friend saying he’s in London/Moscow/Sydney/Wherever, and he’s been mugged. He’s got nothing and needs $2500 to get home. Can you help? Do you really have friends close enough to ask for a $2500 international bailout, but not so close they tell you about the vacation ahead of time? Would they really be too timid to call you collect instead of begging for change to use an internet cafe?

ING Direct – 2 Day Sale

Today and tomorrow, ING Direct is having a “Financial Independence Days Sale”.

It’s a good sale. If you open a checking account or Sharebuilder account and you’ll get $76. Apply for a mortgage and you’ll get $776 off of the closing costs.

I have accounts at 4 different banks. Two of those were opened for specific debt-reduction purposes. Of the others, one is used for most of my cash flow and bill payments, and the other is ING. As of this moment, I have 15 accounts or sub-accounts with ING Direct.

Opening an account is painless and only takes a few minutes. They are currently offering up to 1.25% in an interest-bearing checking account, though I’ve never qualified for more than .25%. That account comes with overdraft protection, so you are charged interest instead of overdraft fees.

Once you have your first account set up, sub-accounts can be created in literally seconds. Why would you want a bunch of sub-accounts? I have a number of saving goals. Each of these goals has its own account at ING. I can tell at a glance how much we have saved for our vacation next month and far away we are from affording my son’s braces. My kids each have an account here because, currently, the interest rate is at 1.1%, which is miles ahead of most traditional banks. Combined with the convenience of total online control, there’s no contest.

Money transfers are smooth. I use one of my accounts as a transfer account to get money to and from two separate banks.

I also have a Sharebuilder account. For those who aren’t familiar with it, it is a stock brokerage with low fees and a low barrier to entry. If you set up an automatic investment, you get $4 stock trades with no minimum. I’m not aware of any place cheaper.

That all sounds like a lot of ad copy and the links are affiliate links, but the truth is, I am just that happy with ING. I’ve never had an accounting error, or any problems at all.

The downside? Paper checks are verboten. They will not accept paper checks, but you do have a check card to use. You can hit 35,000 ATMS for free withdrawals, but any deposits are held for a few days before you have access to the funds. It can also take 3-4 days to transfer money from ING to another bank. I keep enough in the accounts that I’m always spending or transferring older deposits while I wait for the new ones to clear.

Even if you don’t like the bank, get a checking account, use it a few times and get $76 for very little trouble. Open a Sharebuilder account, buy some stock and collect $76 for it. Without an automatic payment, it will cost you less than $20 to buy, then sell the stock, netting you $56.

Who doesn’t like free money?